Image Source: Unsplash

Asian markets soared to new heights, surpassing their previous record close, as hopes of easing trade tensions brought renewed optimism. This positive sentiment followed a period of market turbulence fuelled by concerns over U.S. regional banks. MSCI's regional stock index climbed over 1.51%, with futures signalling gains in both U.S. and European markets. Japan led the charge, with its stock market surging over 3%, driven by expectations that pro-stimulus candidate Sanae Takaichi might become Japan's next prime minister. The yen also strengthened on these predictions. Meanwhile, Chinese equities advanced despite data showing the country’s economic growth had slowed to its weakest pace in a year. In the bond market, U.S. Treasury yields edged higher, with the 10-year yield rising by one basis point to trade above 4%. The Dollar index held steady, while oil prices dipped after three consecutive days of gains. Over in Europe, French bond futures took a hit after S&P Global Ratings downgraded France’s credit rating from AA- to A+, citing concerns over "elevated" budget uncertainty. This downgrade marks the second time in under a month that France has lost its double-A rating from a major credit agency, which could force some investors with strict portfolio requirements to offload French assets. On the geopolitical front, tensions flared in the Middle East as Israel launched strikes on Hamas targets in Gaza. The Israeli government also reportedly halted all humanitarian aid shipments on Sunday, accusing Hamas of orchestrating a deadly ambush that claimed the lives of two Israeli soldiers.

Eurozone inflation remained stable in September, with a slight upward revision to the core index largely due to base effects. Monthly headline inflation at 0.16% aligns closely with the ECB's 2.0% y/y target. Services inflation rose to 3.24% y/y after a 0.24% m/m increase, but the mild disinflation trend is expected to resume. Supercore inflation held steady at 2.51% y/y. Policymakers anticipate a modest CPI undershoot next year before prices stabilize at the target over the medium term. Doves remain concerned about undershooting risks, supported by recent production weakness, while hawks highlight trade uncertainties and potential tariff impacts. However, hawkish arguments seem weaker, even with growth projected to accelerate next year due to easing and fiscal spending. Policy rates are likely to stay stable unless growth deteriorates significantly.

October has earned the nickname "Uptober" among crypto enthusiasts, thanks to its reputation for fueling significant bitcoin rallies. However, this year seems to be breaking tradition, shaping up to be the worst October performance since 2015. As of now, Bitcoin has dropped 5% this month and is hovering around 111K during late Asian trading hours on Sunday, according to CoinGlass data. Historically, October has delivered an average gain of 19.8%, making it one of bitcoin’s stronger months—though it still falls short of November’s impressive average return of 42%.

As disruptions to the US calendar persist, the delayed release of the BLS’s September CPI report (Friday) takes centre stage. This report is crucial for indexing spending commitments. Expectations suggest the headline CPI will edge up to 3.1% year-on-year from 2.9%, while core CPI is projected to remain steady at 3.1% year-on-year. The UK’s economic updates are also grabbing attention. The week kicks off with September’s public finance figures (Tuesday). While some recent discrepancies, such as VAT errors, are expected to be corrected, the overall trajectory is likely to continue exceeding OBR forecasts. With sluggish growth, tax revenues may fall short of expectations, while overspending adds further strain to the fiscal balance. On Wednesday, the UK CPI data is anticipated to reveal a slight uptick in inflation, with persistent challenges in services inflation. Additionally, an update on producer prices, including the quarterly services measure suspended since January, is expected. The week wraps up with retail sales data (Friday), where the overall trend remains weak despite monthly fluctuations.

Meanwhile, preliminary October manufacturing PMIs for major economies will be unveiled on Friday, offering fresh insights into economic activity. The speaker calendar starts on a quieter note as many return from Washington meetings, though ECB President Christine Lagarde is scheduled to speak on Tuesday and Wednesday before the ECB enters its quiet period on Thursday. The Fed is similarly in its blackout phase. Lastly, the Swiss National Bank will release its September meeting minutes on Thursday.

Overnight Headlines

- Chinese Economic Slowdown Worsens With Growth Weakest In A Year

- Japan's LDP, Ishin Agree To Form Coalition Govt, Kyodo Says

- New Zealand Inflation Hits Top Of RBNZ’s 1%-3% Target Band

- S&P Downgrades France On Risks To Budgetary Consolidation

- Italy Wins DBRS Rating Upgrade In Boost For PM Meloni

- Apollo’s Rowan: Europe ‘At War With Itself’ On Financial Regulation

- UK Minister Hints At VAT Cut On Household Energy Bills

- Trump Says US Will ‘Be Fine’ With China As Trade Talks Near

- Rare Earths Stocks Jump As US–China Export War Escalates

- Israel Strikes Hamas, Suspends Aid As Ceasefire Unravels

- Trump Urged Zelenskyy To Accept Putin’s Terms Or Risk More Damage

- Kazakhstan Oil Output At Risk After Russian Gas Plant Hit

- Singapore Law Firm To Sue Switzerland Over Asia Losses On AT1s

- First Ford, Now Jeep; Carmakers Warn Of Global Parts Shortage

- Kering Sells Beauty Division To L’Oreal In $4.7B Deal

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.1600 (818M), 1.1625 (393M), 1.1640-50 (1.7BLN), 1.1655 (310M)

- 1.1690-1.1700 (1.5BLN), 1.1705-10 (664M), 1.1715-20 (1.3BLN)

- 1.1730-35 (550M)...

- USD/CHF: 0.7890-95 (630M), 0.7930-40 (464M)

- EUR/GBP: 0.8705-10 (390M). GBP/USD: 1.3390-1.3400 (732M)

- AUD/USD: 0.6500 (460M), 0.6545-50 (350M). AUD/NZD: 1.1325 (550M)

- USD/CAD: 1.4000 (15BLN)

- USD/JPY: 149.50 (1.1BLN), 150.00-05 (2.2BLN), 150.25-30 (1BLN)

- 150.50 (455M), 151.00 (1BLN), 151.70 (1.1BLN). EUR/JPY: 178.00 (655M)

CFTC Positions as of the Week Ending 9/10/25

-

October 1, 2025: During the shutdown of the federal government, Commitments of Traders Reports will not be published

Technical & Trade Views

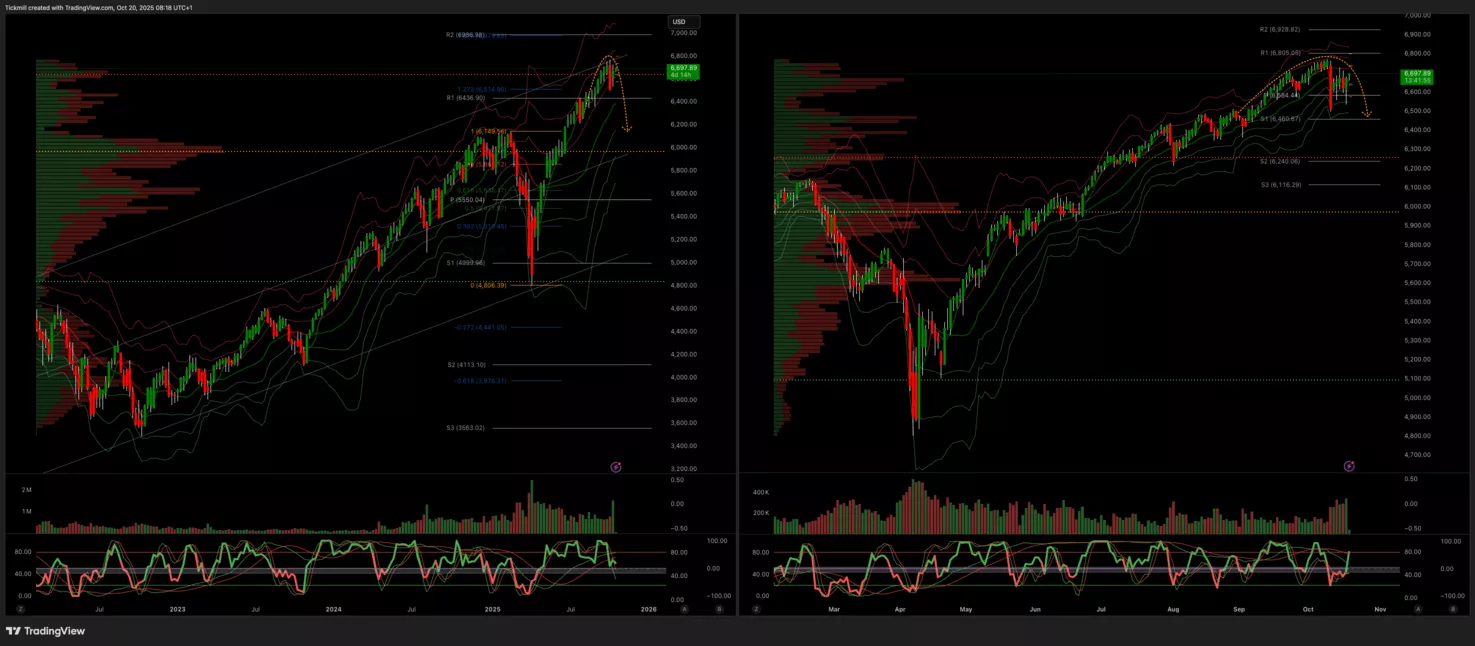

SP500

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 6650 Target 6800

- Below 6600 Target 6400

(Click on image to enlarge)

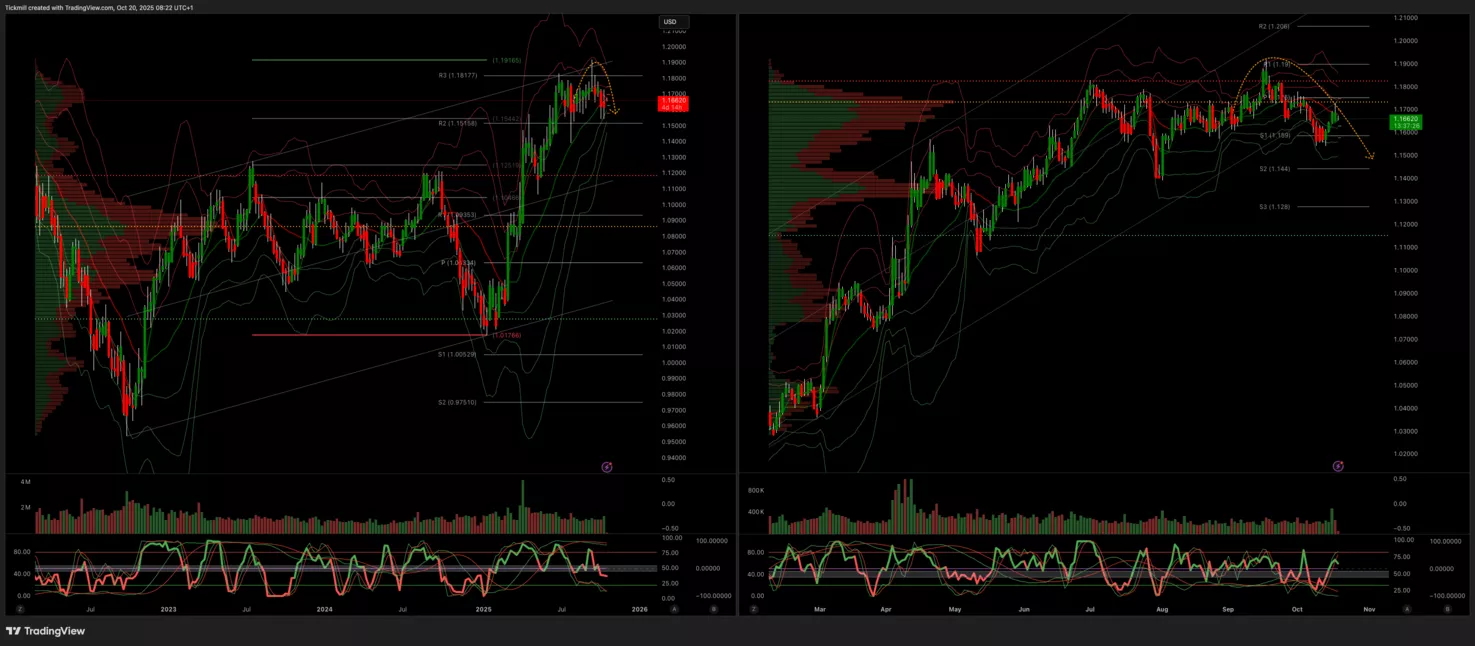

EURUSD

- Daily VWAP Bullish

- Weekly VWAP Bearish

- Below 1.16 Target 1.1450

- Above 1.1650 Target 1.1850

(Click on image to enlarge)

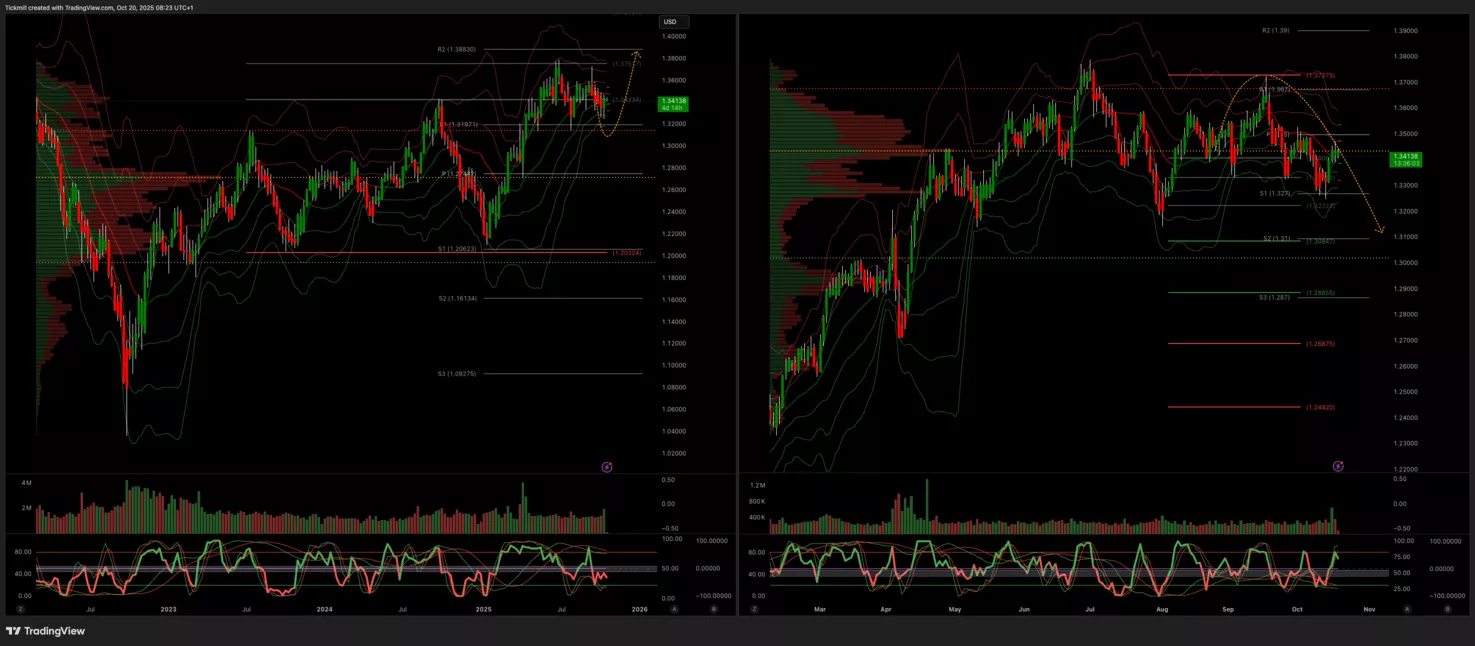

GBPUSD

- Daily VWAP Bullish

- Weekly VWAP Bearish

- Below 1.34 Target 1.31

- Above 1.3450 Target 1.3530

(Click on image to enlarge)

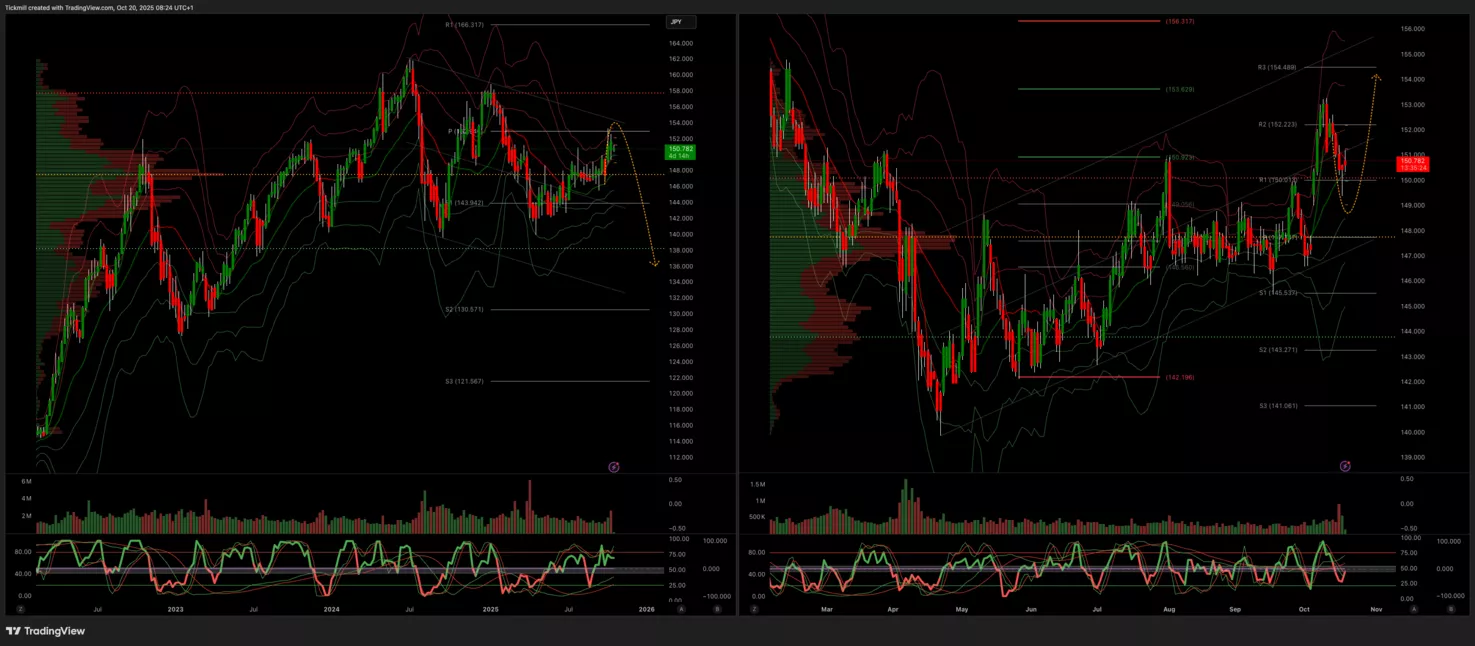

USDJPY

- Daily VWAP Bearish

- Weekly VWAP Bullish

- Below 150 Trgaet 148.5

- Above 151 Target 154

(Click on image to enlarge)

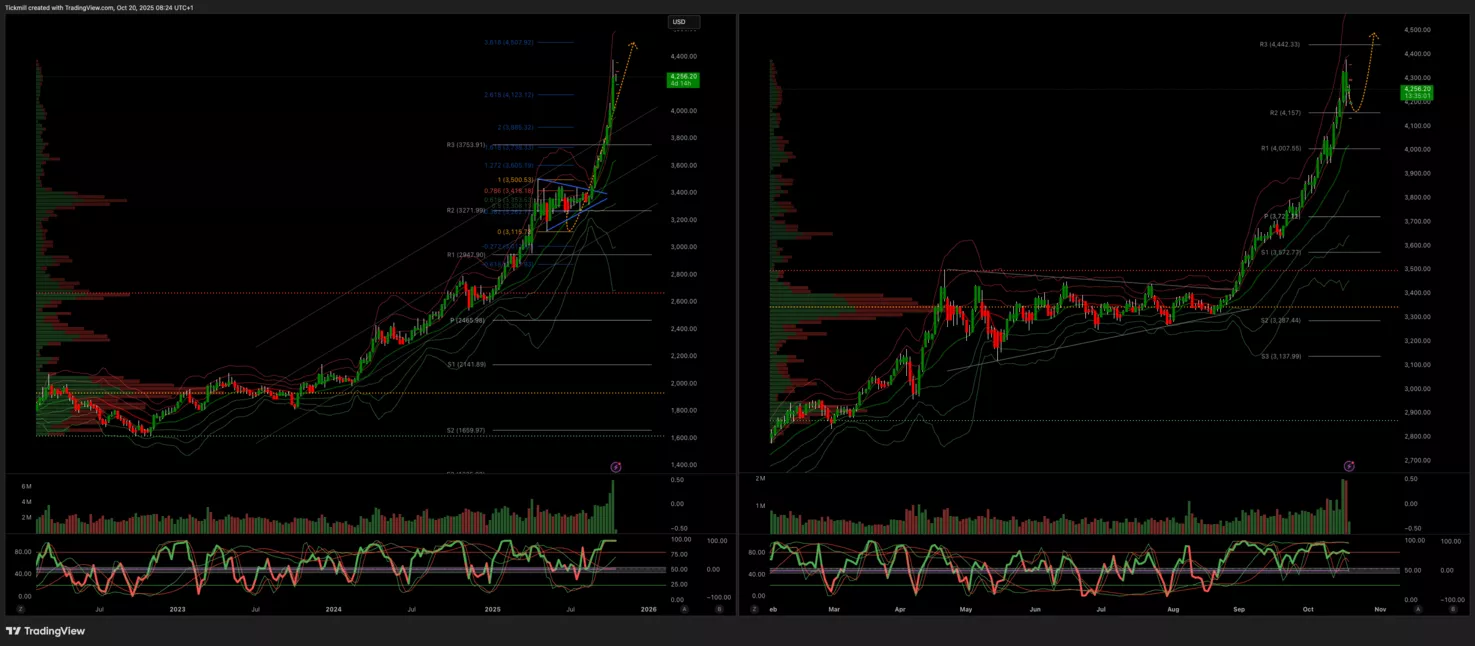

XAUUSD

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 4200 Target 4500

- Below 4050 Target 3950

(Click on image to enlarge)

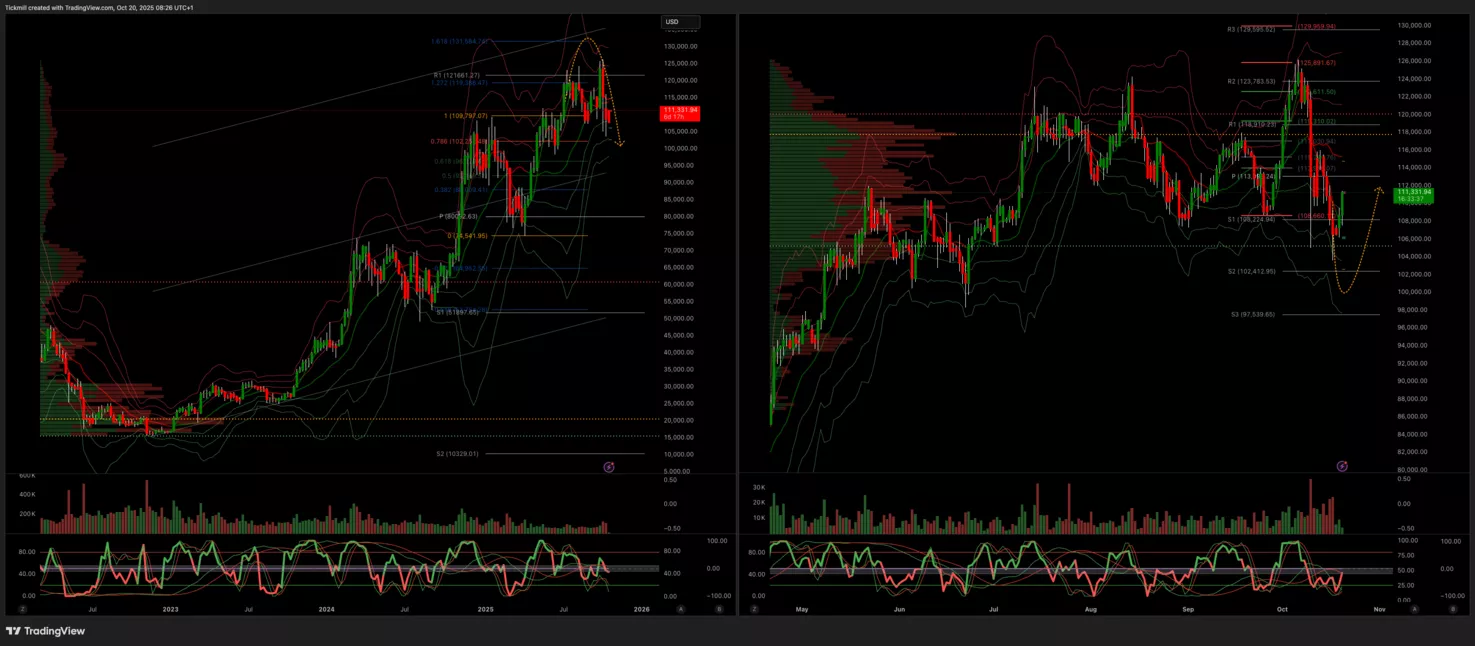

BTCUSD

- Daily VWAP Bullish

- Weekly VWAP Bearish

- Above 107k Target 113k

- Below 106k Target 100k

(Click on image to enlarge)

More By This Author:

Daily Market Outlook - Friday, Oct. 17

The FTSE Finish Line - Thursday, Oct. 16

Daily Market Outlook - Thursday, Oct. 16

Comments

Log in or sign up to join the conversation.