Image Source: Pixabay

Asia - Asian stock markets experienced a decline to their lowest levels in 11 months on Friday. This drop was driven by the continuous increase in long-term U.S. yields, which placed pressure on market valuations. Investor sentiment was marked by caution due to growing concerns that the conflict between Israel and Hamas might escalate into a broader conflict in the Middle East. These fears also led to an increase in oil prices. In Tokyo, the Nikkei index was down by 0.29%, although it managed to recover some ground from its earlier lows. Data from Japan revealed that core inflation in September fell below the 3% threshold for the first time in over a year. In China, blue-chip stocks fell by 0.59%, and Hong Kong's Hang Seng index dropped by 0.75%. Meanwhile, China kept its benchmark lending rates unchanged on Friday, signalling stability in its economy.

Europe - The latest retail sales data for the UK, released for the month of September, revealed a 0.9% monthly decline. This marks the second decrease in the past three months, indicating a potential faltering in consumer spending. This follows a period of stronger-than-expected growth in the first half of the year, raising concerns about the sustainability of the recovery. In addition to the retail sales figures, the October reading of the GfK consumer confidence measure also came out this morning, showing a significant drop to -30. This represents a nine-point decline from the September reading, further underscoring the uncertainties and anxieties among consumers.On the fiscal front, the UK's public finance data for September were also released. The data indicated monthly net borrowing of £13.5 billion, which is approximately £1.5 billion less than the same period in the previous year. Despite being up from the prior year after six months of the fiscal year, it remains below the projections outlined in the March budget. This discrepancy can be attributed to higher-than-expected tax receipts, which have more than offset the increased expenditure due to public sector pay agreements and rising interest payments. While there is uncertainty regarding whether this trend will persist, particularly in light of recent interest rate hikes, it has sparked speculation that next year's budget may include some tax cuts.

US - Stateside the economic data docket is scant, however, investors will focus on a series of speeches by several US Federal Reserve policymakers that will mark the final remarks before they enter a quiet period leading up to their next scheduled interest rate update on November 1st. Recent statements from various Fed officials, including those made by Chair Jerome Powell, have consistently indicated a cautious approach in response to the recent rapid increase in bond yields. These remarks imply that the Federal Reserve can afford to be patient when it comes to deciding on the necessity of further interest rate hikes. Given this cautious stance and the prevailing circumstances, it appears that a rate increase in November is highly unlikely. The central bank's policymakers seem inclined to closely monitor economic developments and the impact of recent events before making any significant monetary policy adjustments.

FX Positioning & Sentiment

There are several compelling reasons why the Swiss National Bank (SNB) might opt to permit the Swiss franc to appreciate. First, a stronger franc has proven effective in containing inflationary pressures, with the Consumer Price Index (CPI) currently at 1.7% year-on-year, closely approaching the SNB's 2% inflation target. Furthermore, the Swiss trade balance has witnessed a remarkable six-fold growth, even as the SNB has actively restrained the franc's ascent. Allowing the currency to gain strength can be instrumental in sustaining this positive trade balance. Moreover, permitting the Swiss franc to strengthen could serve the dual purpose of supporting the currency while facilitating the SNB's desire to further reduce its foreign exchange (FX) reserves. This reduction in reserves, as it continues, may exert downward pressure on major currencies such as the US dollar (USD), euro (EUR), Japanese yen (JPY), British pound (GBP), and Canadian dollar (CAD), influencing global currency markets. Despite a typical response of intervention when the EUR/CHF exchange rate drops, the SNB's current posture appears to be more accommodating of currency fluctuations. This shift in approach suggests the central bank's strategic intent to align the Swiss franc with its broader economic and monetary policy objectives.

CFTC Data As Of 4-10-23

- The US Dollar Index ($IDX) declined by 1.2% in this period.

- The Euro (EUR/$) appreciated by 1.36% during the same period, leading to a reduction of -3,411 contracts in speculative positions. The total net long positions now amount to +75,532.

- The Japanese Yen (JPY/$) saw a minor decrease of -0.22%, resulting in an increase of +14,512 contracts in speculative positions. The total net short positions now stand at -99,476, and the pair is close to the key 150 level.

- The British Pound (GBP/$) strengthened by 1.75%, but speculative positions reduced by -3,368 contracts, mainly due to a dovish Bank of England.

- The Australian Dollar (AUD/$) gained 2% in the same period, with speculative positions increasing by +5,410 contracts, totaling -76,577. The AUD has been lower since Tuesday.

- Bitcoin (BTC) saw a modest increase of 0.04%, and speculative positions grew by +95 contracts, reaching +1,151. The expectation of ETF approval supports BTC.

- It's worth noting that the USD has rallied on a more hawkish Federal Reserve outlook since the period ended, and SOFR red contracts suggest an expectation of higher rates for a longer duration. (Source Reuters)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0420-25 (648M), 1.0475-85 (1.65BLN)

- 1.0500-10 (643M), 1.0515-25 (773M), 1.0545-50 (1.8BLN)

- 1.0575-85 (1.06BLN), 1.0600 (2.306BLN)

- 1.0625-30 (2.85BLN), 1.0640-50 (1.72BLN), 1.0655 (469M)

- USD/JPY: 149.00-05 (1.0BLN), 149.50 (363M)

- 149.60-65 (520M), 150.00 (1.07BLN), 150.50 (820M)

- USD/CHF: 0.9000-10 (1.26BLN).

- EUR/NOK: 11.5895 (250M)

- EUR/CHF: 0.9465 (290M):

- EUR/GBP: 0.8700 (224M)

- GBP/USD: 1.2025 (425M), 1.2150 (452M)

- 1.2190-00 (633M), 1.2250 (354M), 1.2400 (356M)

- AUD/USD: 0.6210 (368M), 0.6250 (535M), 0.6285 (358M)

- 0.6300-30 (776M), 0.6400-05 (387M). AUD/NZD: 1.0730 (442M)

- USD/CAD: 1.3555 (955M), 1.3600 (1.82BLN), 1.3650-60 (356M)

- 1.3700 (481M)

Overnight Newswire Updates of Note

- Japan Inflation Hits 13-Month Low, Stays Above BoJ Target

- Vital Gaza Aid Delivery To Be Delayed, As Palestinians Face Worsening Conditions

- China Injects Most Short-Term Cash Into Banking System On Record

- Chinese Banks Keep Benchmark Rates Steady After PBoC Holds

- Fed’s Bostic Says Achieving 2% Inflation Is ‘Job One For Now’

- Fed's Logan Says Not Yet Convinced Inflation Is Trending To 2%

- Temporary US House Speaker Is Threatening To Quit

- UK's Ruling Conservatives Suffer Two Damaging By-Election Losses

- Russia Seeks Regular Security Talks With North Korea, China

- BoJ To Conduct 5-Year Funds Supplying Operations On Oct 24th

- US Seeks To Buy 6 Million Barrels For Oil Reserve By January

- China To Require Export Permits On Some Graphite Products From Dec 1

- Regional Banks Still Have A Profitability Problem

- Toyota To Adopt Tesla EV Charging Standard From 2025

- HP Enterprise Stock Drops Following Disappointing 2024 Earnings Forecast

- UAW And General Motors Inch Toward Tentative Deal, Union Negotiator Says

- Dish Network, T-Mobile Agree To Extend Deadline For Spectrum Deal

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

SP500 Bias: Bullish Above Bearish Below 4280

- Below 4230 opens 4170

- Primary resistance is 4450

- Primary objective is 4446

- 20 Day VWAP bullish, 5 Day VWAP bearish

(Click on image to enlarge)

EURUSD Bias: Bullish Above Bearish Below 1.06

- Below 1.0520 opens 1.0480

- Primary support is 1.05

- Primary objective is 1.0680

- 20 Day VWAP bearish, 5 Day VWAP bullish

(Click on image to enlarge)

GBPUSD Bias: Bullish Above Bearish Below 1.21

- Below 1.21 opens 1.1950

- Primary support is 1.21

- Primary objective 1.24

- 20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

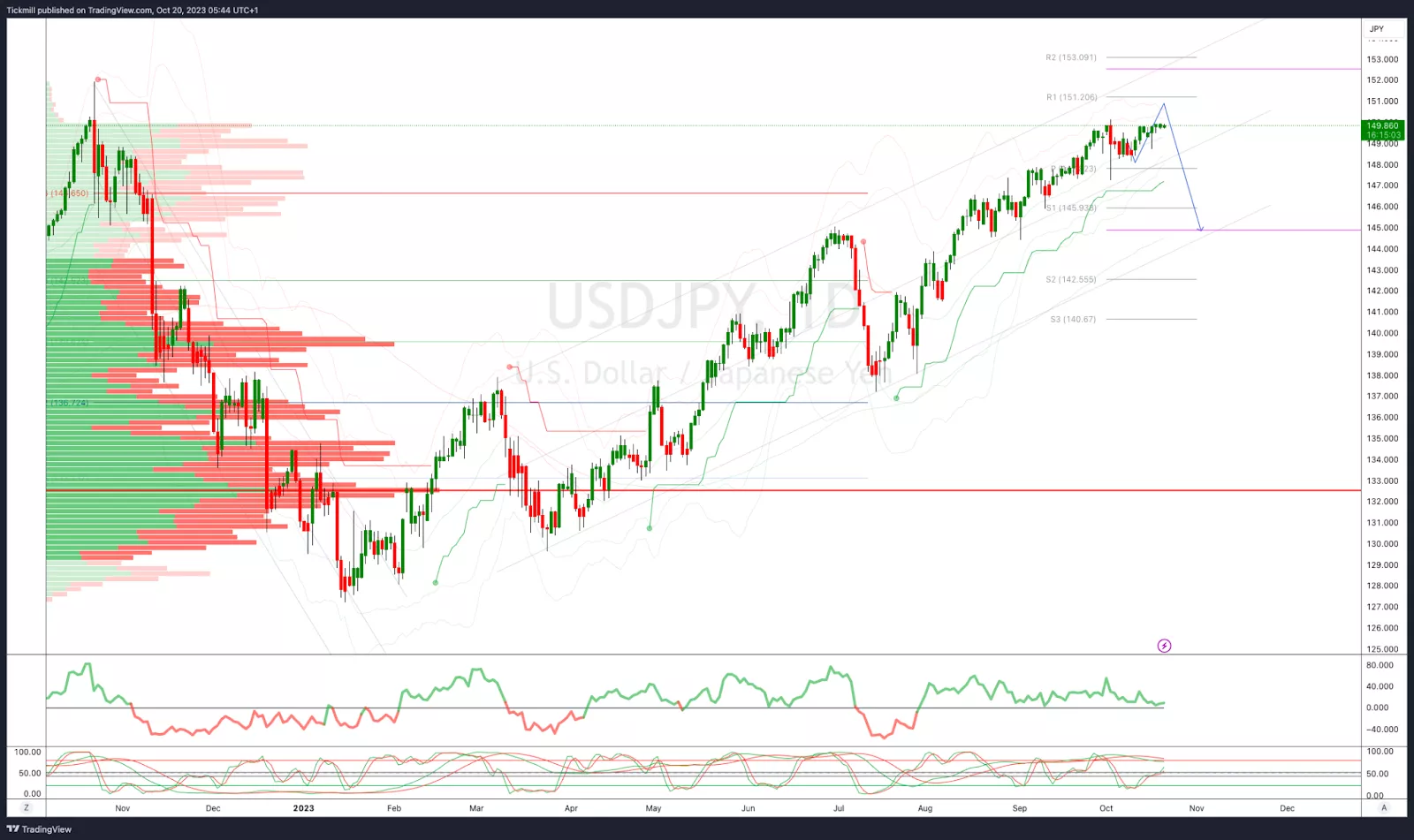

USDJPY Bias: Bullish Above Bearish Below 149.25

- Below 149 opens 148.50

- Primary support 144.50

- Primary objective is 150.20

- 20 Day VWAP bullish, 5 Day VWAP bullish

(Click on image to enlarge)

AUDUSD Bias: Bullish Above Bearish Below .6400

- Above .6475 opens .6525

- Primary resistance is .6620

- Primary objective is .6270

- 20 Day VWAP bearish, 5 Day VWAP bullish

(Click on image to enlarge)

BTCUSD Bias: Bullish Above Bearish below 27500

- Below 27100 opens 26500

- Primary support is 26500

- Primary objective is 31200

- 20 Day VWAP bullish, 5 Day VWAP bullish

(Click on image to enlarge)

More By This Author:

FTSE Slides On Rentokil PlungeTesla Targeting An Equality Test

Daily Market Outlook - Thursday, Oct. 19

Comments

Log in or sign up to join the conversation.