Image Source: Pixabay

Asian stocks exhibited mixed results, with major indices largely remaining range bound. The geopolitical landscape contributed to market sentiment, particularly following joint strikes by the US and UK on Houthi targets. Additionally, investors were digesting Chinese inflation and trade data, which likely influenced trading dynamics in the region. Nikkei 225 rallied over 6% this week, driven by strong earnings from Fast Retailing. Hang Seng and Shanghai Comp struggled for direction despite mixed Chinese trade data and deflationary Chinese inflation figures on a year-on-year basis.

The recently released UK GDP data for November indicated a monthly increase of 0.3%. There were positive developments in industrial production, which rose by 0.3%, and services output, which increased by 0.4%. However, construction activity declined by 0.2%. The October GDP decrease of 0.3% was partly attributed to exceptionally wet weather, so the November increase may be partially due to the reversal of this effect. Despite the monthly rise, the three-month GDP growth remained down by 0.2%, indicating ongoing weakness in underlying economic activity. The rest of today’s data slate is relatively scant. The recently released French December CPI data showed no change from the previously reported figures, with a slight increase in annual inflation to 4.1% from 3.9% in November, primarily driven by energy prices. This is expected to be temporary, with inflation forecasted to decrease further this year. The European Central Bank's Chief Economist Philip Lane is set to speak at a conference in Dublin on post-pandemic economic rebuilding, potentially addressing longer-term monetary policy trends.

Stateside, following the slightly stronger-than-expected December inflation reported in yesterday's CPI reading, the PPI data for the same month will provide new insights into pipeline price pressures. PPI inflation had previously declined mainly due to falling goods prices, but the December data is anticipated to show modest increases in annual changes in both overall and headline inflation. Federal Reserve policymaker Kashkari is also scheduled to speak, and it will be interesting to hear his perspective on the likelihood of interest rate cuts in the US, given his recent shift from being dovish on monetary policy to advocating for tighter policy.

US bank earnings kick off the earnings season in the US today, they are expected to report the fourth-highest year-over-year earnings decline among all 11 GICS sectors for Q4 2024. Investors should focus on the impact of the sharp decline in interest rates, credit quality deterioration, and updates to 2024 guidance. The decline in 10-year Treasury yield is positive for bank capital levels, but deposit pricing lags may pressure net interest margins. Weakness is expected in mortgage revenues and rising credit card delinquencies. Investment banking revenues are also expected to stay weak, with M&A more so than underwriting. Wealth management may benefit from a year-end rally, and cost-cutting measures are anticipated, particularly at larger banks. JPMorgan, Bank of America, Citigroup, and Wells Fargo will report their fourth-quarter and full-year results today.

Overnight Newswire Updates of Note

- US, UK Launch Airstrikes On Houthi Rebel Targets In Yemen

- China’s Consumer Prices In Longest Streak Of Declines Since 2009

- China's Exports Drop For First Time Since 2016 As Demand Cools

- BoJ Is Said To Consider Lowering Forecasts For Growth And Inflation

- U.S. And China Keep A Close Watch As Taiwan Heads To The Polls

- Fed Officials: December CPI Did Not Budge View On Inflation

- ECB's Lagarde: Think We Are Over Hardest & Worst Bit Regarding Infl

- Dollar Steady As Markets Assess Higher-Than-Expected US CPI

- Deutsche Bank Sees Strong Dollar Even As Fed Cuts Interest Rates

- Treasuries Edge Lower, Japan 30YR Auction Sees Weak Demand

- Oil Jumps As US Airstrikes Against Houthis Fan Mideast Tensions

- Citi Lowers Brent Price Outlook For 2024 And 2025 On Oversupply Fears

- Stocks In Asia Rise, Supported By A Continuing Rally In Japan Shares

- Tesla Cuts Prices Of Both Locally-Made Models In China

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0920-25 (1.2BLN), 1.0940-50 (1.5BLN), 1.0960 (601M)

- 1.0975-80 (1.3BLN),1.0990-1.1000 (2.1BLN), 1.1025 (623M), 1.1050-55 (2BLN)

- USD/CHF: 0.8540-50 (1.2BLN), 0.8575 (809M)

- GBP/USD: 1.2600 (655M), 1.2730 (508M), 1.2800 (319M)

- AUD/USD: 0.6660 (525M), 0.6675-80 (1.1BLN), 0.6690-0.6700 (800M)

- 0.6750-60 (835M), 0.6800 (767M)

- NZD/USD: 0.6200 (605M), 0.6245-50 (1.1BLN)

- USD/CAD: 1.3300 (681M), 1.3330 (480M), 1.3375 (400M), 1.3425 (584M)

- 1.3445-50 (1.2BLN)

- USD/JPY: 144.75-80 (553M), 145.00 (1.6BLN), 145.50 (355M)

- 146.00-15 (1.9BLN)

- FX option prices dropped after the release of U.S. CPI. The decrease in CPI volatility risk led to lower implied volatility. The 1-month expiry benchmark reached new lows for 2024 after the holiday gains. Lower implied volatility suggests less expected realized volatility, but some 1-month options are considered valuable based on this. The implied volatility for 1-month GBPUSD, EURUSD, and USDCHF is now lower than the realized volatility. Long implied volatility would be profitable if the FX performance repeats past months, with EUR/USD 1-month trade having the biggest implied discount at 1.3.

CFTC Data As Of 05/01/24

- USD bearish increasing-1,674

- CAD bearish decreasing +1,045

- EUR bullish neutral +138

- GBP bullish neutral +78

- AUD bearish decreasing +601

- NZD neutral neutral +198

- CHF bearish increasing -262

- JPY bearish neutral -157

Technical & Trade Views

SP500 Bullish Above Bearish Below 4730

- Daily VWAP bullish

- Weekly VWAP bullish

- Below 4730 opens 4700

- Primary support 4670

- Primary objective is 4830

(Click on image to enlarge)

_638406459887504105.webp)

EURUSD Bullish Above Bearish Below 1.1000

- Daily VWAP bullish

- Weekly VWAP bullish

- Above 1.1030 opens 1.1070

- Primary resistance 1.1130

- Primary objective is 1.0850

(Click on image to enlarge)

_638406459554227248.webp)

GBPUSD Bullish Above Bearish Below 1.28

- Daily VWAP bullish

- Weekly VWAP bullish

- Above 1.28 opens 1.2870

- Primary resistance is 1.2820

- Primary objective 1.2580

(Click on image to enlarge)

_638406459353288945.webp)

USDJPY Bullish Above Bearish Below 143.50

- Daily VWAP bullish

- Weekly VWAP bullish

- Below 143 opens 142.50

- Primary support 142.50

- Primary objective is 147

(Click on image to enlarge)

_638406459046411705.webp)

AUDUSD Bullish Above Bearish Below .6750

- Daily VWAP bearish

- Weekly VWAP bearish

- Below .6660 opens .6550

- Primary support .6525

- Primary objective is .6933

(Click on image to enlarge)

_638406458831567505.webp)

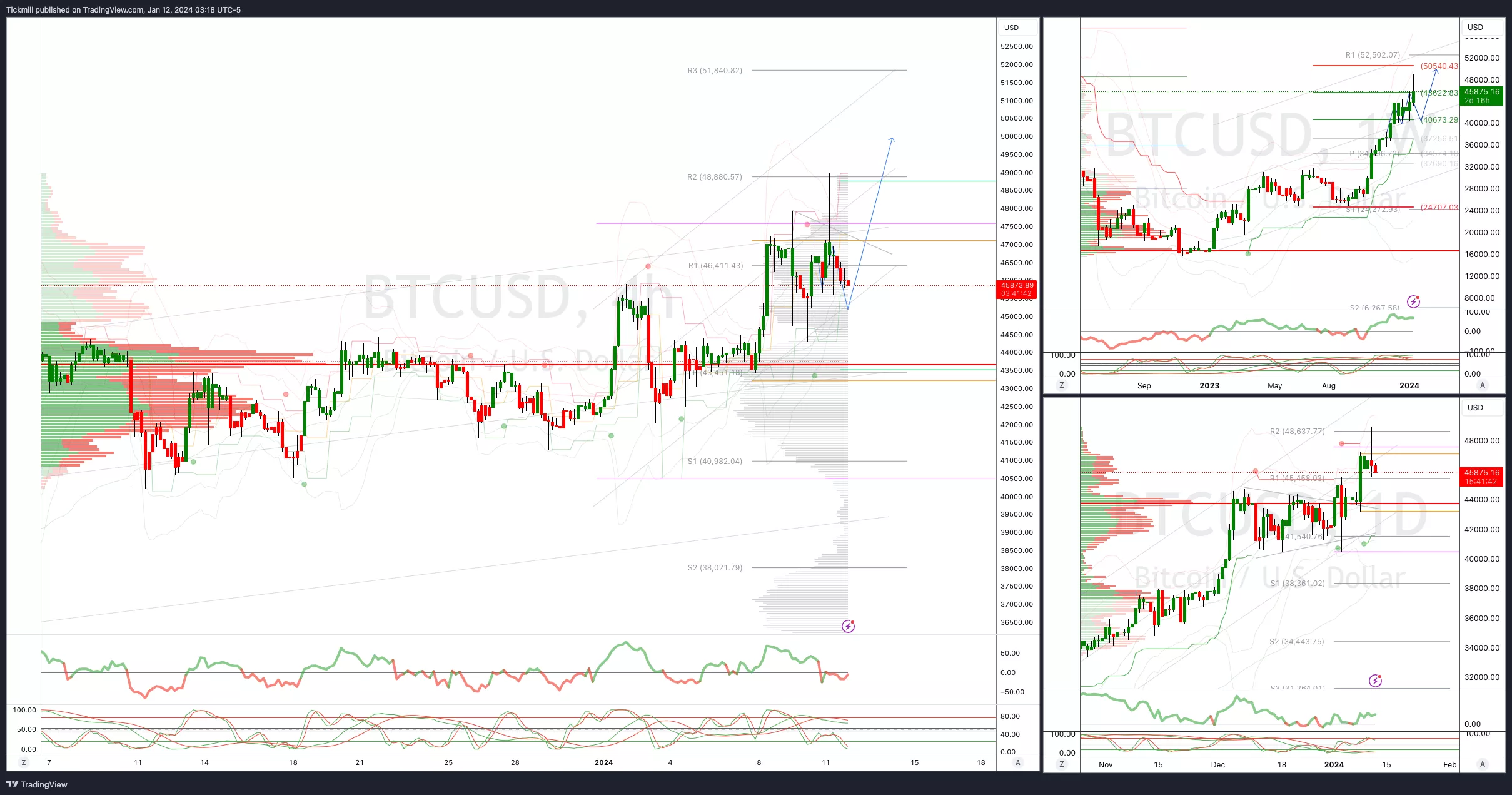

BTCUSD Bullish Above Bearish below 45200

- Daily VWAP bearish

- Weekly VWAP bullish

- Below 45000 opens 44600

- Primary support is 40000

- Primary objective is 50000

(Click on image to enlarge)

More By This Author:

FTSE A Brief Flash Of Green Before Reversing Into The Red AgainDaily Market Outlook - Thursday, Jan. 11

FTSE Floundering In The Red Again, As Sainsbury's Fails To Impress

Comments

Log in or sign up to join the conversation.