Image Source: Pixabay

Investors on Wall Street took an optimistic view on the effects of Donald Trump's trade conflict on American companies, leading to a surge in stock prices. They speculated that the Federal Reserve might lower interest rates sooner than expected to stave off a recession. The S&P 500 increased by 2%, reaching its highest point since Trump announced his tariff strategy. Despite Beijing's denial, the president claimed that the U.S. is negotiating with China on trade. Alphabet's stock soared in late trading after reporting strong earnings, while Intel offered a negative outlook. Bond yields fell amid speculation that Fed Chair Jerome Powell could be pressured to ease policy if the labour market weakens.

The MSCI Asia-Pacific Index continued to rise after a Bloomberg News report suggested that China is considering suspending its 125% tariff on certain U.S. imports. South Korean stocks rose by 1% following Treasury Secretary Scott Bessent's mention of a potential trade "agreement of understanding" by next week. The Nikkei-225 surged up to 2% due to positive developments in U.S.-Japan trade talks. The dollar index increased, while Treasuries held their gains from the previous day. Sources indicate that China is contemplating lifting tariffs on some U.S. imports as the ongoing trade conflict significantly affects certain industries. Officials are considering removing additional levies on medical equipment and some industrial chemicals, including ethane, according to anonymous sources due to the sensitivity of the discussions. On Thursday, President Trump stated that his administration was in talks with China regarding trade, while Beijing denied any negotiations and insisted that the U.S. remove all unilateral tariffs. Several countries have sought relief from increased tariffs, which have been postponed for 90 days to allow time for discussions.

UK retail sales defied expectations with a third consecutive monthly increase in March, rising 0.5% compared to the predicted -0.4%. Excluding autos and fuels, sales also rose 0.5% against a forecasted -0.5%. Despite a slight downward revision for February, the year-on-year growth accelerated to 2.6% and 3.3%. Favourable weather boosted demand for clothing and outdoor goods, though supermarket sales weakened. Softer prices supported spending, with the core retail deflator slowing to 0.8% year-on-year. Strong wage growth, a resilient labor market, and solid household balance sheets continue to underpin spending, although overall sales volumes remain below historical trends, indicating a recovery phase.

Political events continue to drive intra-day market volatility; however, markets remain with one eye firmly on the macro landscape. Next week offers a wealth of significant U.S. data to examine. Leading the agenda on Wednesday is the Advance Q1 GDP report. Trade distortions are expected to weigh heavily, as indicated by the Atlanta Fed Nowcast, with a median forecast of a 0.4% quarterly annualised gain, down from 2.4% in Q4. The performance of private consumption and investment will be equally critical, given recent shifts in consumer confidence. Following the GDP figures, the monthly PCE report is anticipated. In line with CPI improvements, the market expects a flat month-over-month headline reading, potentially reducing the year-over-year rate from 2.5% to 2.2%. Core PCE is expected to improve similarly, with a 0.1% month-over-month estimate suggesting a year-over-year rate of 2.6%, down from 2.8%. Ironically, the U.S. inflation profile aligns closely with the Fed's easing targets, if not for the ongoing tariff-related risks. The week concludes with the non-farm payrolls report, with a median forecast of 123,000 jobs. Survey data indicates a softer job market, though it might be too soon for this to fully manifest, particularly as the BLS has yet to account for DOGE-related job cuts. Nonetheless, the pace is likely to slow from March's stronger figures.

Overnight Newswire Updates of Note

- BlackRock CEO Larry Fink: We’re Investing In ‘Undervalued’ Britain

- UK Chancellor Rejects Parts Of Trump’s ECN Agenda Before Talks

- Trump’s Pressure On China Casts Shadow Over Australia Election

- China Weighs Exempting Some US Goods From Tariffs As Costs Rise

- PBoC’s Pan Reiterates Monetary Policy To Remain Moderately Loose

- Chinese Banks’ Wealth Products See Fund Inflow In April

- China Listed Firms’ Annual Report Delay Worries Investors

- Apple Aims To Source All US iPhone From India In China Pivot

- BYD’s Earnings May Fuel Further Gains In Shares Versus Tesla

- RBA: Interest Rates Don’t Hit Households As Hard As You’d Think

- The Fed Withdraws Its Guidance On Bank Crypto-Related Activities

- Alphabet Shares Rise On Stronger-than-expected Revenue Growth

- Yahoo Is Ready to Buy Chrome Browser If Google Is Forced to Sell

- Intel CEO Lip-Bu Tan Hints At Foundry Collaboration With TSMC

- US To Press Putin To Drop Demilitarisation Demand Part Of Peace Deal

(Sourced from reliable financial news outlets)

FX Options Expiries For 10 am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.1295-1.1300 (322M), 1.1320-30 (400M), 1.1350-65 (584M)

- 1.1390-1.1400 (1.5BLN), 1.1440-50 (1BLN), 1.1500-15 (937M)

- EUR/CHF: 0.9500 (570M), 0.9525 (708M)

- GBP/USD: 13130 (200M). EUR/GBP: 0.8525 (571M), 0.8575 (391M)

- AUD/USD: 0.6350 (390M), 0.6375 (358M), 0.6400 (290M), 0.6425 (725M)

- USD/CAD: 1.3800 (2.1BLN), 1.4000 (2.2BLN)

- USD/JPY: 142.50 (484M), 142.75 (350M), 143.00 (390M), 143.65-75 (460M)

- 144.00 (250M), 144.45 (406M), 144.70 (300M), 145.00 (1.7BLN)

- EUR/JPY: 164.60 (463M), 165.00 (375M)

Barclays is the first to unveil its preliminary model forecasts for month-end FX flow. The model anticipates a robust demand for USD across all leading currencies. This comes in the wake of the 2nd April liberation day, which caused a global risk-off sentiment and a decline in stock markets. Conventional safe havens, such as US Treasuries and the USD, experienced significant declines as well. This situation resulted in an unexpected expansion of U.S. swap spreads and a spike in credit spreads. The trade-weighted USD dropped by 4.6% in April, prompting a rebalancing that drove USD demand

CFTC Data As Of 18/4/25

- The Euro's net long position is at 69,280 contracts, while Bitcoin holds a net long position of 586 contracts. The Japanese yen shows a strong net long position of 171,855 contracts, in contrast to the Swiss franc's net short position of 28,584 contracts. The British pound has a net long position of 6,509 contracts.

- Equity fund speculators have decreased their S&P 500 CME net short position by 47,956 contracts, lowering it to 239,649. In contrast, equity fund managers have increased their S&P 500 CME net long position by 1,812 contracts, bringing it to 805,062.

- Speculators have expanded the net short position in CBOT US 5-Year Treasury futures by 40,000 contracts to 2,061,575, while reducing the CBOT US 10-Year Treasury futures net short position by 140,715 contracts to 937,755. Additionally, the net short position for CBOT US 2-Year Treasury futures has risen by 56,664 contracts to 1,254,773. Speculators have also increased the net short position for CBOT US Ultrabond Treasury futures by 19,747 contracts to 220,057, and for CBOT US Treasury bonds futures by 82,631 contracts to 100,785.

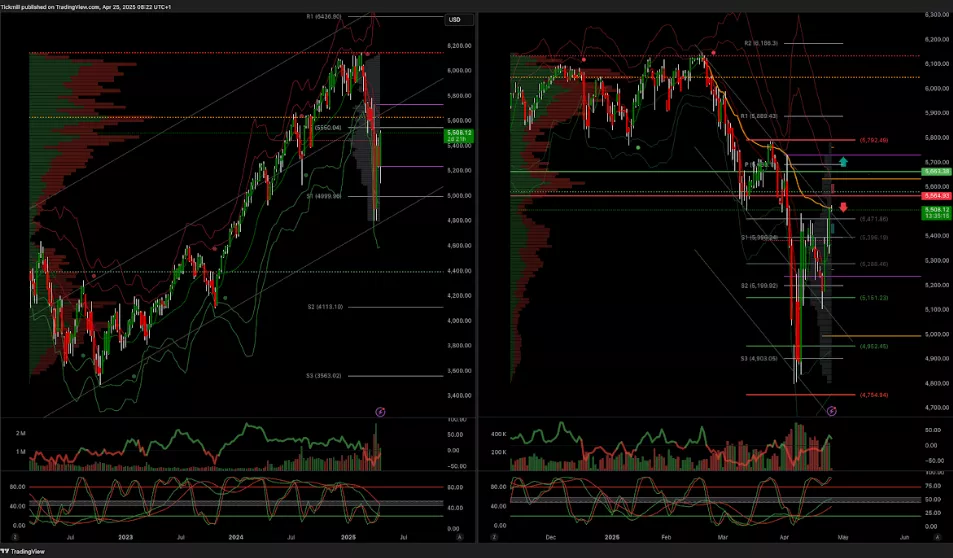

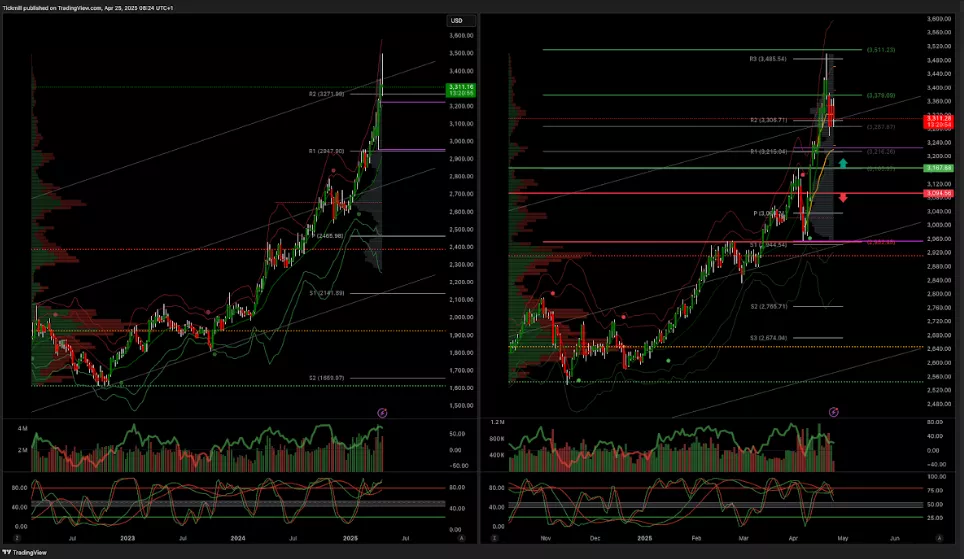

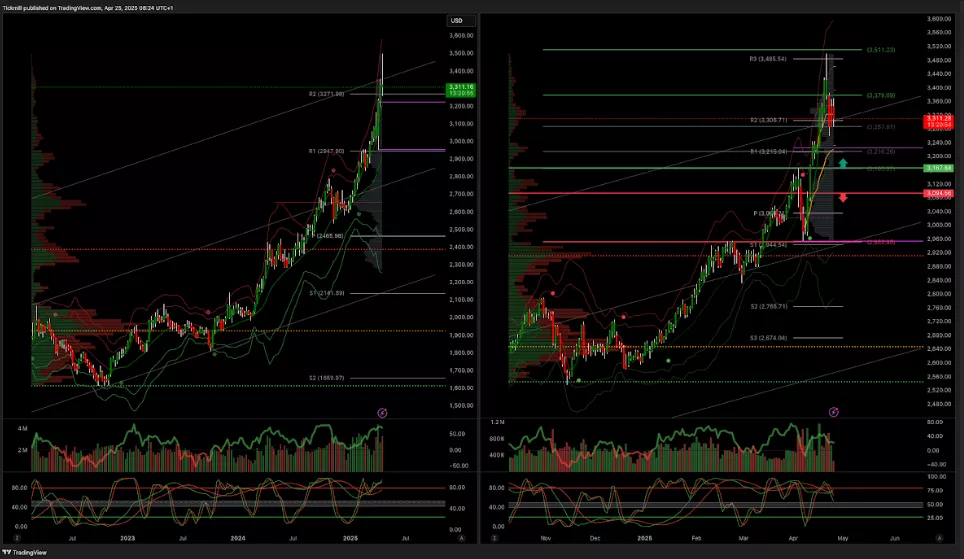

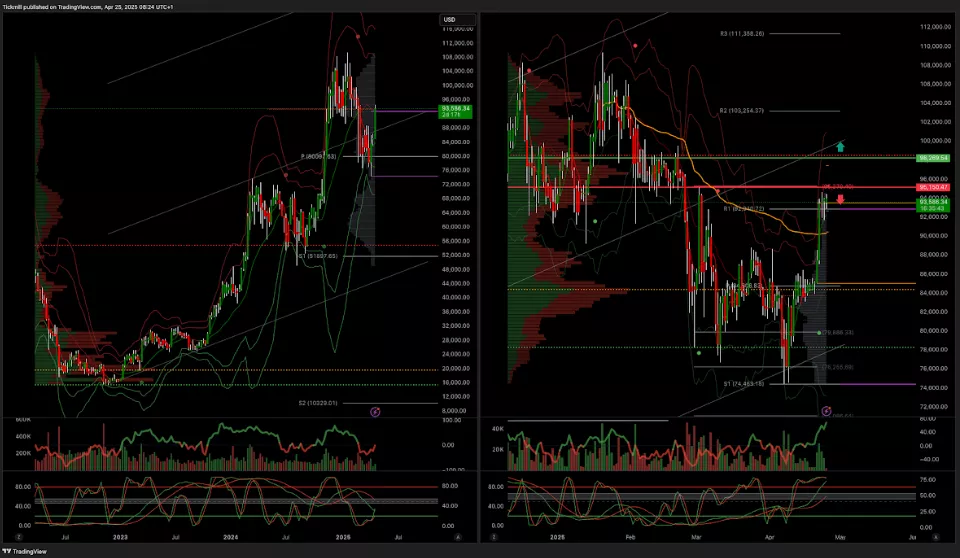

Technical & Trade Views

SP500 Pivot 5610

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 5665 target 5792

- Below 5000 target 4755

(Click on image to enlarge)

EURUSD Pivot 1.11

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bearishness into the end of April

- Above 1.12 target 1.19

- Below 1.1070 target 1.0945

(Click on image to enlarge)

GBPUSD Pivot 1.28

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 1.34 target 1.38

- Below 1.29 target 1.27

(Click on image to enlarge)

USDJPY Pivot 147.70

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bearishness into early May

- Above 1.52 target 153.80

- Below 146.53 target 139

(Click on image to enlarge)

XAUUSD Pivot 3100

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bearishness into mid/late April

- Above 3200 target 3640

- Below 3000 target 2950

(Click on image to enlarge)

BTCUSD Pivot 90k

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bullishness into mid/late April

- Above 97k target 105k

- Below 95k target 65k

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Thursday, April 24

Daily Market Outlook - Thursday, April 23

The FTSE Finish Line - Wednesday, April 23

Comments

Log in or sign up to join the conversation.