Image source: Pixabay

Central Bank Watch Overview:

- Fed policymakers have been speaking in more hawkish tones, downplaying the idea that the rate hike cycle is finished and rate cuts are coming in 2023.

- More importantly, the FOMC, collectively, appears comfortable with allowing US financial assets to fall and the US unemployment rate to rise if that means US inflation rates can be tamed.

- Rates markets see a 100% chance of a 75-bps rate hike in September.

Rate Hikes Are Still Coming

In this edition of Central Bank Watch, we’ll review comments and speeches made by various Federal Reserve policymakers since the Jackson Hole Economic Policy Symposium last month. Fed policymakers have been speaking in more hawkish tones, downplaying the idea that the rate hike cycle is finished and rate cuts are coming in 2023. More importantly, the FOMC, collectively, appears comfortable with allowing US financial assets to fall and the US unemployment rate to rise if that means US inflation rates can be tamed.

75-Bps Or 100-Bps This Week?

The tone deployed by Fed policymakers at the Jackson Hole Economic Policy Symposium and the September Fed meeting suggests that a 75-bps rate hike is very likely, even after Fed Chair Jerome Powell suggested, at the July Fed meeting, that rate hikes to such a degree were less likely moving forward. Having abandoned forward guidance to embrace a data-dependent stance, the hotter-than-expected August US inflation report (CPI) and the strong August US nonfarm payrolls report have bolstered the case for an aggressive tightening effort.

August 29 – Kashkari (Minneapolis president) said that weakness in US equity markets showed that investors understood how serious the FOMC is about bringing down US inflation rates.

August 30 – Bostic (Atlanta president), in an essay posted to the Atlanta Fed’s website, commented that “incoming data – if they clearly show that inflation has begun slowing – might give us reason to dial back from the hikes of 75 basis points that the Committee implemented in recent meetings. We will have to see how those data come in.”

Williams (New York president) suggested that further aggressive rate hikes remain necessary, given that “we need to have a somewhat restrictive policy to slow demand and we’re not there yet.”

August 31 – Mester (Cleveland president) downplayed suggestions that the Fed would cut interest rates in early 2023.

September 1 – Bostic noted that the Fed still has “some work to do” in order to bring down inflation, and that “we have got to slow the economy down.”

September 7 – Barkin (Richmond president) bluntly stated that the Fed must raise rates to a level where they restrict economic activity. “You do have to move to a level where inflation expectations come down in order to have enough restriction on the economy to bring inflation down.” Furthermore, he added, “the destination is real rates in positive territory and my intent would be to maintain them there until such time as we really are convinced that we put inflation to bed.”

Mester issued caution over “declaring victory over the inflation beast too soon,” and that “we do have to raise rates from where they are now.”

Brainard suggested that interest rates will stay elevated for a long time, as “we are in this for as long as it takes to get inflation down.” Additionally, “monetary policy will need to be restrictive for some time to provide confidence that inflation is moving down to target.”

Daly (San Francisco president) noted that the Fed is trying to orchestrate a “slowdown,” and by raising interest rates, the Fed is “bringing price stability back, slowing the job market, slowing the housing market, slowing the growth of the economy but doing so in a way that still allows us to move forward.”

September 8 – Powell (Fed Chair) committed to further aggressive action in the near term, noting “we need to act now, forthrightly, strongly as we have been doing.”

Bullard (St. Louis president), in an essay posted to the St. Louis Fed’s website, said that “bringing today inflation rate back down to that 2% target is the top priority for the FOMC.”

Evans (Chicago president) argued that “I think that we’ve got a good plan in place. We could very well do [75-bps] in September,” but “my mind is not made up. I do know that we need to be increasing interest rates up to a substantially higher level than where they are now.”

Bullard commented that, in the wake of the August US jobs report, was leaning towards a 75-bps rate hike at the September Fed meeting.

Waller (Fed Governor) said “the case for continuing to remove policy accommodation remains clear-cut.”

Markets Discounting Varying Degrees Of Hawkishness

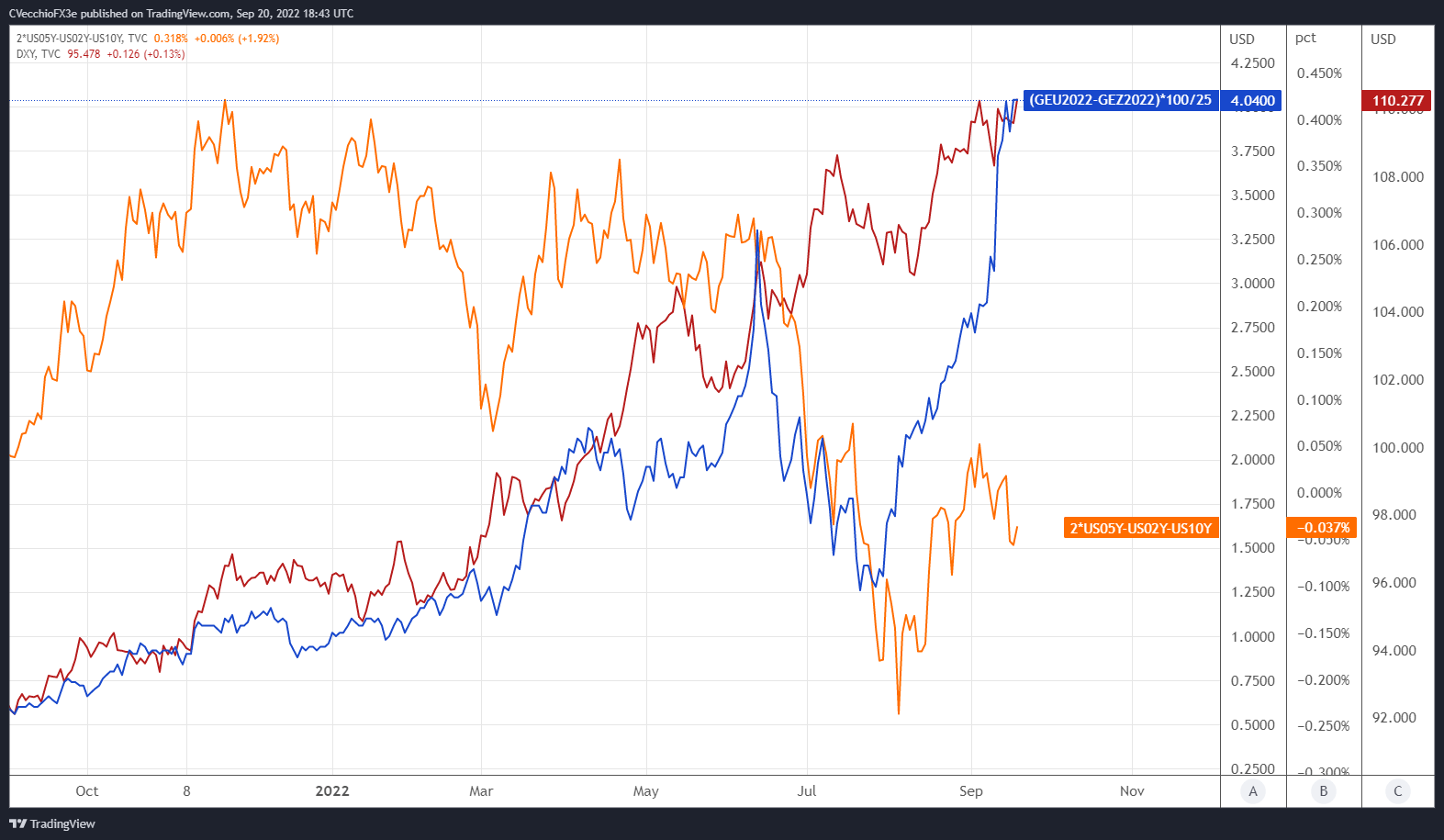

We can measure whether a Fed rate hike is being priced in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the front month/September 2022 and December 2022 contracts, in order to gauge where interest rates are headed by the end of this year.

Eurodollar Futures Contract Spread (September 2022-December 2022) [blue], US 2S5S10S Butterfly [orange], DXY Index [red]: Daily Timeframe (September 2021 To September 2022) (Chart 1)

(Click on image to enlarge)

September thus far has been defined by rapidly rising Fed rate hike odds. On August 1, there was one 25-bps rate hike priced in through the end of 2022, with a 34% chance of a second 25-bps rate hike (50 bps in total by the end of the year). Now, 100 bps worth of rate hikes is fully discounted, with a 4% chance of a fifth 25-bps rate hike.

To an extent, the market is suggesting that the last few Fed rate hikes may materialize in the coming months – with the bulk of the tightening efforts arriving this week, where a 75-bps rate hike is the base case scenario. Given the outside chance of a 100-bps rate hike, should the Fed deliver 75-bps and not offer hawkish forward guidance, the September Fed meeting could shape up to be a ‘buy the rumor, sell the news’ event for the US Dollar.

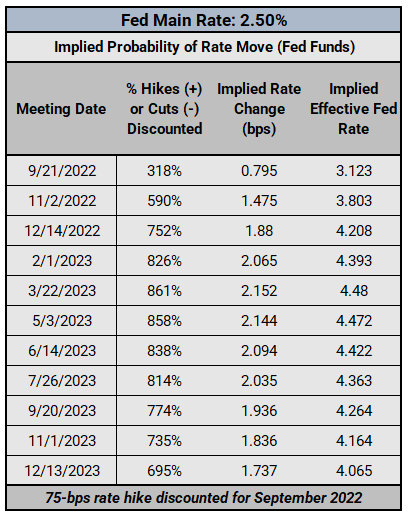

Federal Reserve Interest Rate Expectations: Fed Funds Futures (September 20, 2022) (Table 1)

As has been the case for several weeks, Fed fund futures remain more aggressive than Eurodollar contract spreads in the near term. Rates markets see a 118% chance of a 75-bps rate hike in September (a 100% chance of a 75-bps rate hike and an 18% chance of a 100-bps rate hike), with additional 50-bps rate hikes fully discounted in November and December. Ahead of the Jackson Hole Economic Policy Symposium, the main rate was expected to rise to 3.552% by the end of 2022; it is now discounted to end the year at 4.208% (currently 2.50%).

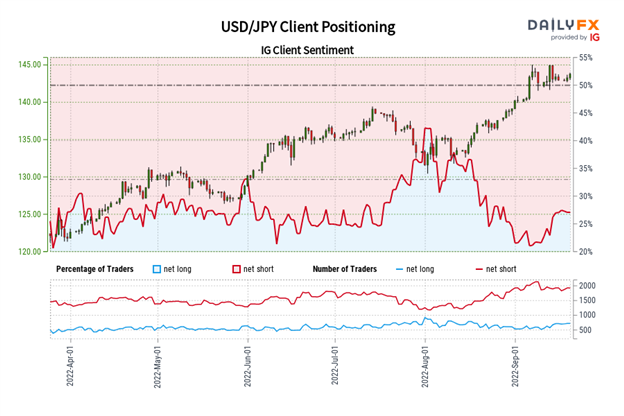

IG Client Sentiment Index: USD/JPY Rate Forecast (September 20, 2022) (Chart 2)

USD/JPY: Retail trader data shows 29.49% of traders are net-long with the ratio of traders short to long at 2.39 to 1. The number of traders net-long is 6.82% higher than yesterday and 42.68% higher than last week, while the number of traders net-short is 0.16% lower than yesterday and 4.37% higher than last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Yet traders are less net-short than yesterday and compared with last week. Recent changes in sentiment warn that the current USD/JPY price trend may soon reverse lower despite the fact traders remain net-short.

More By This Author:

FX Week Ahead - Top 5 Events: Canada Inflation Rate; Fed Rate Decision; BOJ Rate Decision; SNB Rate Decision; BOE Rate Decision

Euro Forecast: EUR/USD Struggling, But EUR/GBP & EUR/JPY Retain Bullish Potential

Canadian Dollar Technical Analysis: CAD/JPY, USD/CAD Rates Outlook

Comments

Log in or sign up to join the conversation.