Dick's Sporting Goods: A Value Story

Recommendation Summary

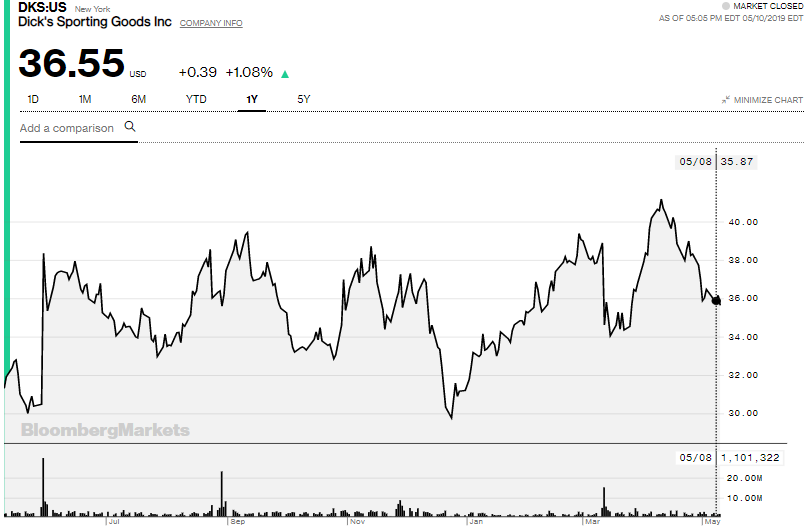

*Source: Bloomberg

In my opinion, Dicks Sporting Goods (DKS) is a company going through big changes, and the volatile stock price reflects that. So with all the changes going on, is the company worth the ~$36 per share price today?

Last year Dick’s removed guns from 10 stores and this year the company expanded its strategy, halting gun-sales and ammunition at 125 stores, targeting mainly locations with struggling firearms sales. The company also announced it would replace Reebok merchandise on its shelves with their own in-house private label apparel brand. As a result of these changes, analysts have put an overall hold recommendation on the stock with a price target of $37 per share.

I believe that by dropping Reebok and replacing it with an in-house brand the company can actually increase operating margins in the long-run. With these shifts in company strategy, I would expect a drop in the stock price this year, before the company stabilized and starts to profit. I think most of the expected changes are positive, but it will take time before the company rebounds.

Investment Thesis

*Source: Company Presentation

As of today, Dick’s e-commerce business remained strong throughout the year and increased 17% over last year. As a percent of total net sales, online business increased to 23% compared to 19% in the same period last year. I expect the increase in online sales to help the company’s margins, but ultimately I think the main revenue driver in the years ahead will be DKS’s in-store experience. This past February, the company rolled out nearly 150 in-store HitTrax batting cages across the country, giving baseball and softball players the ability to test bats for free before making a purchase. This, coupled with the strengthening of the company’s private-label assortment, could have a positive future outcome for Dick’s. With expanding its in-house Calia athletic wear brand to 80 stores and launching a new outdoor apparel brand, the company positions itself well for the coming change.

Below you can find several company metrics (based on my calculations) and see where the company stands right now. The numbers I have used for calculating these metrics are as follows, share price of $36.6 dollars per share, Enterprise Value of $3,557 million and an EBIT of $328 million (EBIT has been calculated by including an adjustment for operating leases of $-117 million dollars):

-

P/E Ratio – 11.29x – US industry average: 25.19x.

-

EV/Revenue – 0.4x – US industry average: 0.95x

-

EV/EBIT – 10x - US industry average: 14.6x

Keep in mind that the numbers I have used for global and U.S. industry averages were taken from professor Damodaran’s website.

Per the numbers presented above, the company trades at below the global industry averages for the sector. These numbers may not incorporate the true underlying value of the company, but offer a quick overview of where it sits in a market of its peers.

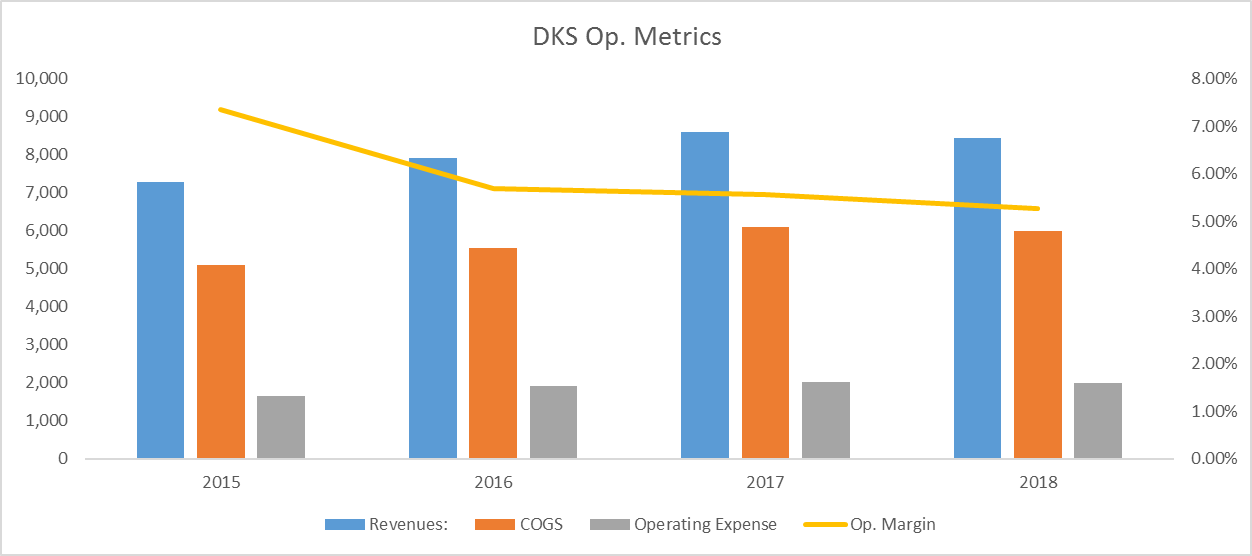

In the graph below, you can see how the company’s operating metrics have performed through the last few years. We can also clearly see margins falling in 2016 and experiencing only a slight downward trend from 2016 through 2018, this was mainly due to the low-margin hunt and electronics business:

*Source: Company filings and author’s own estimates

Recent Results

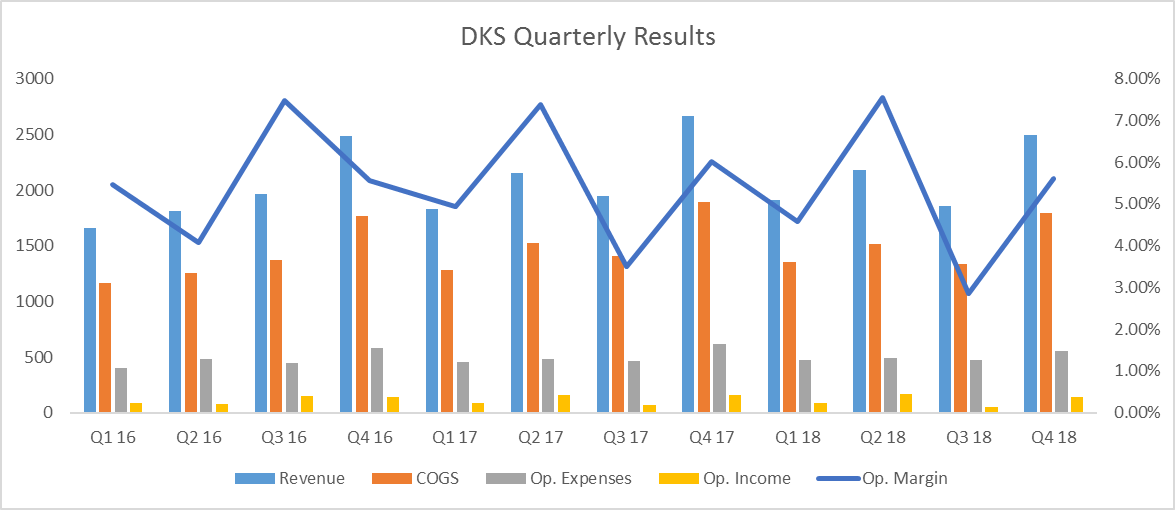

Dick’s recorded a Q4 18 revenue of $2,492 million, representing a yearly decrease of 6.46% for the quarter, this reflects the impact of the calendar shift, which negatively impacted sales by $39 million and the impact of the extra week sales from last year which generated $105 million. Gross profit in the fourth quarter was $694.6 million or 27.87% of net sales, a 168 basis points decline versus last year. The decline in gross margin was driven by higher shipping, fulfillment and freight costs as a result of our strong e-commerce growth and by occupancy deleverage.

In the graph below you can see that the lowest point of operating margins were in Q3 18, this is mainly due to a lower sales number and a higher operating expense as a percent of revenue. The lower revenue number was because of the impact of the calendar shift which negatively affected sales by $41 million or $0.10 a share in the quarter.

Source: Company filings and author’s own estimates

New Facilities

*Source: Pressconnects

I think the key to driving Dick’s revenue growth could be a new, highly automated order fulfillment center in Conklin. Such a center would help the company with faster deliveries, thus improving customer experience.

Dick's President Lauren Hobart said:

"We believe a big opportunity to continue improving our online experiences to faster and more reliable delivery, … to achieve this, we're investing significantly in our fulfillment capabilities (in New York and California). These new facilities will open during the third quarter and will enable us to deliver the majority of our online orders within two business days in the near future."

Further expansion of the Conklin center from 630,000-square-feet to 930,000 square feet over the next year, will transform it into the largest of the company's five across the nation.

The company is also investing in robotics to drive automation and optimize Dick’s cost per shipment in the New York fulfillment center. This will help Dick’s to lower COGS and improve margins in the future. Such a strategy, coupled with the development of new in-house brands, could actually help the company grow in future years.

New In-Store Experience

*Source: Company presentation

As mentioned above, the company rolled out 150 in-store HitTrax batting cages across the country this February. Anna Whieldon, Community Marketing Manager, Dick’s Sporting Goods said:

“The Cage gives athletes the ability to analyze HitTrax swing metrics in order to find the right fit for their game. It also has a fun, interactive element to store for our customers here at Walden Galleria.”

The new batting cage at Dick’s gives athletes the ability to analyze swing metrics, by being able to capture real-time stats immediately following impact so players can review and understand how certain bats perform for them. Swing metrics include exit velocity, launch angle, distance, point of contact, play outcome and more.

Software Development

This year Dick’s is expected to finish the transition to in-house software for all its e-commerce platforms, after developing new inventory tracking software. The in-house software plans include an overhaul of the website, how products are showcased online, the website’s search, checkout functions and shipping estimates. The team that developed the inventory software has a self-imposed goal to earn at least 10 times the cost of the team in annual revenue. Thanks to its tech overhaul, Dick’s is now able to list sports products online within 30 minutes of a major event, such as a championship win or a player trade.

Industry Peers

In the analysis below, I have included Dick’s direct competitor. Footlocker offers a product range closest to Dick's pricing and quality, and could disrupt Dick’s market share in the future. I believe that Footlocker is the most appropriate peer to compare Dick’s Sporting Goods to.

Footlocker

*Source: Bloomberg

Footlocker (FL) is an American sportswear and footwear retailer, with headquarters in Midtown Manhattan, New York City, and with additional stores operating in 28 countries worldwide.

In the past year, Foot Locker’s stock price has increased by 35% and operating profit margin has decreased from 10% to 9%. The decrease in profit in the last year is mainly driven by higher SG&A costs reflecting the investments the company made in digital capabilities and logistics, and higher incentive compensation.

As of today, Foot Locker has made investments in several different ventures, thus expanding its reach over the market. The retailer recently invested in consumer startups, including a $100 million investment in sneaker resale platform GOAT, $12.5 million in children’s apparel company Rockets of Awesome, a $3 million investment in children’s footwear brand SuperHeroic, and a $2 million investment in Pensole Footwear Design Academy. Foot Locker also invested $15 million last year in women’s active wear company Carbon38 and announced recently that it is investing an additional $10 million into the company in January.

Recently the company made a $100 million investment in GOAT Group, one of the most well-known players in the fast-growing $6 billion global sneaker reselling market. GOAT is considered to be the world's largest marketplace for authentic sneakers operating GOAT and Flight Club brands. The investment brings GOAT’s total raised investment to $197.6 million since its launch in 2015. This is the largest investment to date by a retailer into the secondary sneaker market, as well as Foot Locker’s biggest investment ever. Such a move will put FL on the map in e-commerce.

The investment in Rockets of Awesome a kids clothing brand, puts FL in a position to further tap into the children’s apparel market. Foot Locker CEO Dick Johnson said that the company is looking for ways

“To tap into the capabilities and talent of innovative and unique brands through partnerships or investments” as it aims to serve “the evolving youth culture.”

Foot Locker’s investment in Rockets of Awesome is part of the online retailer’s $19.5 million Series C funding round. Rockets of Awesome, which barely has any brick-and-mortar presence other than several pop-up shops — will now be working with Foot Locker and opening stores within Kids Foot Locker locations. This could further solidify Foot Locker’s position in the kids market, thus bringing in more revenue for the company in future years.

On January 3rd Foot Locker announced that it made a strategic investment in Super Heroic, Inc. The company is taking a minority stake in the innovative, high-performance, tactical play and entertainment company whose mission is to inspire children to be more active through play. The $3 million Series Seed II investment brings the total raised by Super Heroic to $10 million since it was founded. Super Heroic was founded by Jason Mayden a former Jordan Brand designer and is a lifestyle brand that designs, manufactures and markets innovative footwear, clothing and accessories. Super Heroic could bring a new revenue stream to Foot Locker, as they are not only going to tap into the children's market, but also introduce new, innovative designs into their already broad product inventory.

In January of this year, Foot Locker announced another investment, $2 million in the Pensole Footwear Design Academy. Foot Locker and its vendor partners will collaborate with Pensole on new educational programs and the design and manufacturing of exclusive products for Foot Locker. Pensole offers a unique blend of education geared specifically to help designers enter the footwear industry and now has 400 graduates working in the sneaker industry. This could offer Foot Locker a powerful advantage. By having access to new talent, Foot Locker would be able to provide customers with unique designs, thus extending the company’s brand and giving them an edge over the competition.

On January 22nd Foot Locker announced that it made a strategic investment in Carbon38, taking a minority stake in the world's destination for women's luxury active wear. The $15 million Series A funding round brings the total raised by Carbon38 to $26 million since 2013. Carbon38 is the world's leading women's luxury active apparel company.

Below you can find several company metrics (based on numbers from GuruFocus) and see where the company stands right now:

-

EV/EBIT Multiple – 7.88x

-

P/E Multiple – 12.37x

-

EV/Revenue – 0.72x

Considering all this, it seems Foot Locker is very well priced based on multiples. With the underlying value the company provides, I can see why FL could be a good investment opportunity.

Source: Company filings and author’s own estimates

Income Statement Breakdown

Revenue

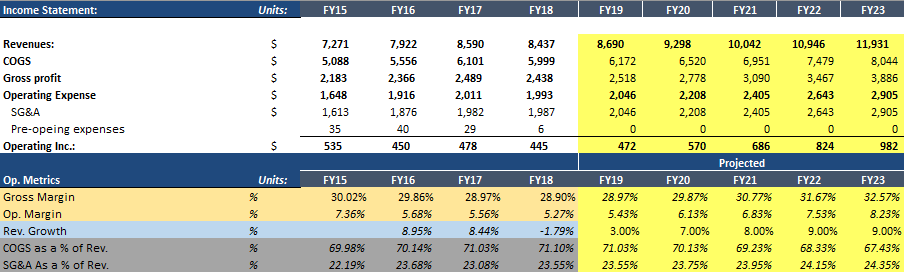

As we can see from Dick's income statement below, revenue has fallen in the last year by roughly 2%. The fall in revenue was mainly driven by a decrease of same-store sales and an impact of the calendar shift explained above in the “Recent-Results” section.

For the years ahead I expect the company to grow at an average of 7.2% per year supported by driving new in-store experiences, strong digital innovation and highly automated fulfillment centers.

Source: Company filings and author’s own estimates

Gross Margins

We can see gross margins constantly decreasing in the last three years, driven by a constant increase in COGS.

For the 5 years ahead I forecast an increase in gross margins mainly supported by the increase in digital sales driven by anticipated double-digit sales growth in e-commerce which has lower gross margin rate and the investments the company is making to improve fulfillment capabilities.

SG&A

In the years ahead I expect SG&A costs to increase slightly. SG&A is expected to deleverage as a result of the company’s strategic investments, driven by increasing hourly wages and higher freight costs.

Catalysts

Catalysts in the next 12-24 months for the price to increase include:

In-House Software Development

In-house software I think could help the company increase its margins in the long-run and provide more value for customers. Strategic Resource Group, a consumer industry consulting firm, expects Dick’s to increase its market share to 50% of its retail category, up from about 20%, within the next five years, due in part to investments in technology.

New Private Brand

With Dick’s and Reebok going their own way I would expect the company to experience a short-term decline in sales. Despite that, in the long-term I would expect the company to recover and even improve its operating margins.

Private brands grew double-digits in 2018, increasing as a percent of sales to 14% from 12%. For 2019 Ed Stack, Dick’s CEO said:

“We expect a continued strength as our private brands will play an important role in our space allocation and assortment strategies”.

Calia, the women’s fitness line backed by Carrie Underwood, will expand its footprint in approximately 80 Dick’s stores. A new athletic apparel brand is also set to launch in time for back-to-school that will replace its licensed Reebok line.

Valuation

DCF Analysis

The analysis I have done here is a base case scenario built on Dick’s current and expected future performance in the market. This scenario takes into consideration Dick’s new in-store improvement and new facilities.

For the DCF analysis I have used the assumptions listed below, which got me to an equity value of $2,406.3 million and a share price of $24.36 per share with diluted shares outstanding of 99.781:

-

A 6.4% average discount rate.

-

Revenue growth for the next 5 years at an average of 7.2% per year and then slowly declining when reaching year 10 to the terminal growth rate of 3%.

-

Operating Margin at an average of 6.8% in the first 5 years and then increasing to an average of 7% from year 6 to year 10, in order to be in-line with the global industry averages pre-tax operating margins. For a terminal operating margin I have used 7%

-

A tax rate of 25%

-

A ROIC at 4% at year 1 and slowly increasing throughout the years until reaching 5.4% at year 10 and getting closer to industry averages. For a terminal ROIC rate I have used 10%, the global industry average number.

Please take into consideration that the scenario I have used in the above section in the analysis is pretty easily achievable with the underlying value the company has, combined with the management’s views for the foreseeable future.

Risks

Some of the macro-factors, such as a slowdown in consumer spending and a possible increase in labor costs, are already included in my analysis on Nordstrom (JWN). In order to not repeat myself I will not include them here:

Eliminating Firearms

Recently the company said it’s going to strip firearms and other hunting products from 125 of its stores and replace the merchandise with batting cages, ski apparel and other sports gear. If everything goes as planned, the company says this shift will be expanded to other stores.

Mr. Edward Stack, Dick’s CEO said:

“People in the gun business are not terribly happy with us... They said we were toxic, which is fine with us; we’re not going to change the way we’re going.”

First quarter comps are still expected to be impacted by the company’s decision to halt sales of assault-style weapons in their stores, along with the sale of guns and ammunition to customers under age 21.

Struggles With Under Armour

Dick’s Sporting Goods fourth-quarter results were hurt not only by stripping arms and other hunting products from some of its stores, but also by some of the moves Under Armour (UA) made. CFO Lee Belitsky said in an interview:

“Under Armour continues to be difficult, but we mentioned now for the second quarter in a row that our apparel business is a positive, so we’ve been able to replace the lost Under Armour apparel business with other brands in the stores at this point.”

The struggles the company is experiencing with Under Armour may prove to be damaging to both sides in the long-run.

Key Takeaways

In considering all catalysts and risks, I think there is a high possibility that Dick’s stock price will experience a significant drop. Despite DKS’s transformation, according to my calculations the company is trading above its fair value for now. I would expect a difficult year for the retailer as the company adjusts and stabilizes in the coming years.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Good read.

Thanks

Adding batting cages to Dick's store was a brillaint idea! I really appreciate that kind of innovation and out of the box thinking for a company.

On the one hand, yes, adding batting cages is a brilliant idea. I can see that definitely driving higher sales of bats. But what percentage of total sales are bats? Compare that to the incredibly dispropriation amount of space required to house those batting cages. And the added insurance costs to protect people from injury. I wonder if the added value is worth it.

I do get it yeah, on a sales per square foot they will lose some money at the start, but to be honest it would make me want to go there more. Bringing more people into stores could offset the loss on the sales per square foot.

Yes, I agree 100%. It's like how Starbucks spent a lot of money to change the atmosphere of going for a cup of coffee. Sure cushy chairs and sofas took up a lot of space, but business exploded. Same concept.

It's just a gimmick to get people in the door. Sure they'll have some people going just for fun, or to try out a single new bat. But once in the store, they may buy all their sports equipment there. Overall, I thing it's a good idea to drive more business to #Dicks. The better question is, what's to stop #FootLocker from doing the same thing.

They will have to add some more in-store experience for sure, but it is a good start. Digital sales is growing.

Excellent article and very thorough analysis on $DKS and $FL.

Thank you for the positive feedback!

I will be looking at $GHG next hope it brings some value your way.

Will be looking forward to that. Haven't been able to find any reliable coverage on that company.

Thanks, looking forward to to the $GHG article.

Good read. Though I find it ironic the #Dicks likely spent millions of dollars on a state of the art facility to achieve parity with Amazon's ability to offer 2-day shipping. Then right after it opens, Amazon ups the ante to 1-day shipping.

Thanks for taking the time to comment.

They really did and although Amazon does have the moeny to beat them they ain't the whole market.

I think there is still value to be had in $DKS.

@[Angry Old Lady](user:7657), Ouch! Lol, that has to hurt!