CONCERNS ABOUT US HOUSING MARKET, OVERHEATING ECONOMY

There’s a lot of chatter among market participants about the state of the US housing market, which has seen its strongest run of price growth since 2006 – right before the last US housing bubble burst, which helped lead to the Global Financial Crisis. Concerns were heightened this week after US Treasury Secretary Janet Yellen said that “it may be that interest rates will have to rise somewhat to make sure that our economy doesn’t overheat” when discussing the potential impact of US President Joe Biden’s latest stimulus bill.

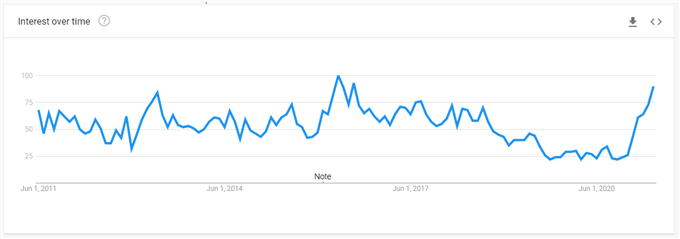

GOOGLE TRENDS “HOUSING BUBBLE” (MAY 2011 TO MAY 2021) (CHART 1)

This isn’t just a concern from policymakers. Everyday Americans are taking notice of the state of the US housing market too. In fact, Google searches for the term “housing bubble” are approaching their highest level over the past ten years. The big questions for traders and investors alike are thus: will the Fed’s regime of low rates continue to entice homebuyers as mortgage rates remain historically low? Or will rising costs sideline buyers – and finally take air out of the recent US housing price bubble?

RAW MATERIALS PUSHING PRICES

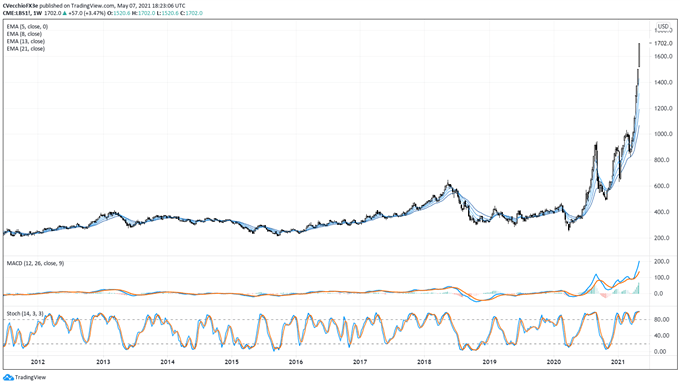

“Growth” was expected to be the story of 2021, thematically speaking. The rise in commodity prices reinforces the idea that this expectation has become reality. But lumber prices are blowing away other major commodities in terms of their price-performance year-to-date, up by nearly +95%: corn is up over +51%; copper has gained over +34%, and wheat prices are up a paltry +19% by comparison.

LUMBER FUTURES PRICE CHART: WEEKLY TIMEFRAME (MAY 2011 TO MAY 2021) (CHART 2)

The US housing inventory is at its lowest level in four decades, while supply chain issues (e.g. closed sawmills) have helped lift lumber prices to all-time highs, leading to over a $35K increase in new home prices in the US since the start of 2021. Until supply chain issues are resolved, input costs for new homes will remain high, effectively squeezing a certain segment of first-time homebuyers out of the market.

HOUSING AFFORDABILITY METRICS STABLE

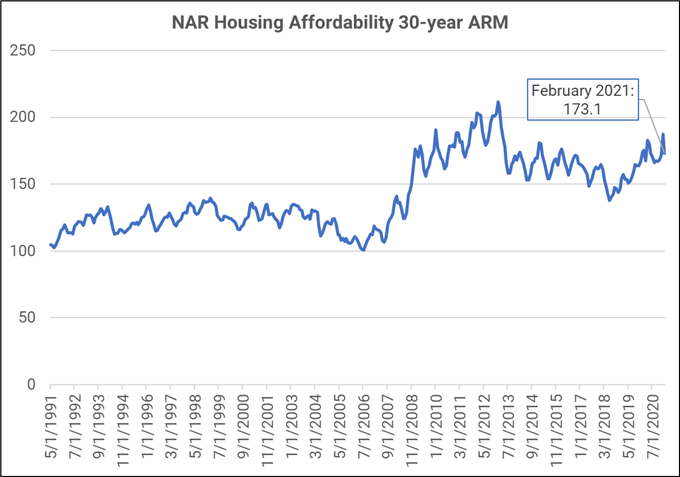

Even though housing input costs have run higher alongside other commodity prices, measures of housing affordability have only just started to fall. The US-based National Association of Realtors produces various measures of housing affordability, including one measure that is tethered to the average 30-year mortgage rate derived from the Freddie Mac Primary Mortgage Market Survey:

NAB HOUSING AFFORDABILITY INDEX: MONTHLY TIMEFRAME (MAY 1991 TO MAY 2021) (CHART 3)

At the start of 2021, housing affordability was at its best level going back to early-2013, according to the NAR Housing Affordability Index. Curiously, the last time this measure of US housing affordability (prior to the recent decline) was this high was right before the 2013 Taper Tantrum; we may have just experienced a ‘taperless tantrum’ in recent weeks.

MORTGAGE RATES LOW, BUT…

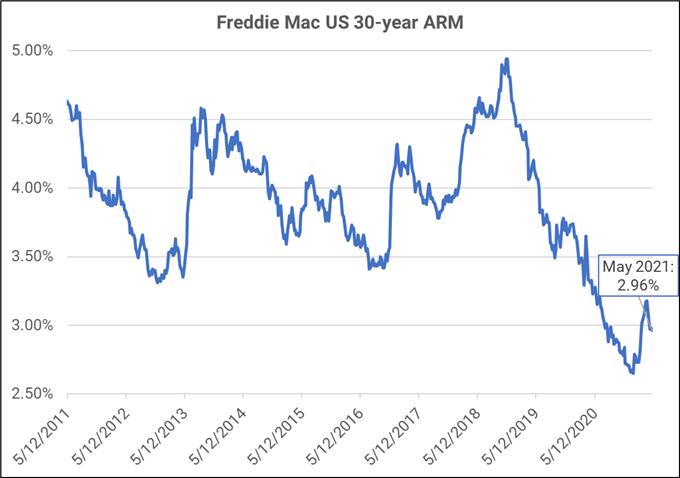

Low mortgages have kept measures of housing affordability within reason, but US Treasury Secretary Janet Yellen’s warning this week about higher interest rates are a stark warning. Recent changes have been quick and therefore unpleasant, deprived of the historical context of the US housing market beyond the scope of the pandemic.

FREDDIE MAC US 30-YEAR MORTGAGE RATE: WEEKLY TIMEFRAME (MAY 2011 TO MAY 2021) (CHART 4)

For now, the US Treasury yield curve has remained tame, which in turn has relieved upside pressure on mortgage rates (which are tethered to the long-end of the US yield curve). Some quick scratch math shows that, on a $500,000 mortgage, for example, if rates were to rise by another 50-bps, American homeowners would send around another $1600 out the door each year.

IS THERE A US HOUSING BUBBLE? WILL IT BURST?

The US housing market has been on a tear in recent months, no doubt. But going so far as to call it a bubble may be a bridge too far, given that US mortgage rates remain historically low and that measures of housing affordability remain historically rich. House price growth will likely moderate henceforth, but a dramatic turn lower seems unlikely in the very near term.

Comments

Log in or sign up to join the conversation.