Image Source: Pexels

Market Analysis

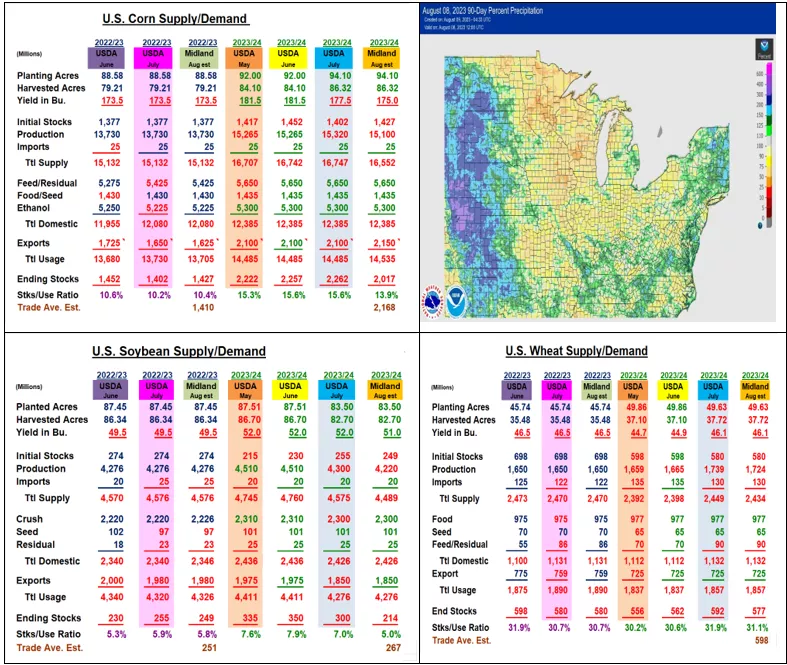

As we approach the August 11 crop report, the trade has turned mixed about 2023’s US corn & soybean crops. US satellite firms have become more positive about the vegetative look after our dry Central US spring, particularly in the ECB where hefty July rains have occurred. N Plains, PNW & SW dryness remains possible problem areas. 2023’s warm to hot Midwest temperatures advanced plantings & crop development, but the N Plains experienced another cool & wet spring before conditions opened in mid-May. Conversely, heat built into the Midwest & Mid-South from the SW in May & June. With limited Central US subsoil moisture, the US G/E crop ratings drop by 19% to 50% in corn & 12% to 50% in beans during June. July’s ECB rains did prompt 7% & 4% recoveries. Our C. IL crop tour revealed many strong corn & bean fields. However, 2 early planted corn fields had sizable tip-back & reduced ear counts cutting their yields sharply. However, one field’s yield was the highest since 2016. July’s rains have been positive for soybean pods count vs 2022, but August will determine if they make the harvest. Overall. our 2023’s C. IL corn yield was up 0.6 bu from 2022 prompting a 206 bu August estimate, solid, but no bin buster for us.

The USDA’s August crop estimates are based on a producer survey & enhanced satellite crop views since 2020. No enumerator field counts until September. Utilizing our tour data & Midwest rainfall maps, our August US yield is 175 bu for a 15.1 billion crop. Slow exports could slice 25-50 million from 22/23 demand. However, a smaller crop and a pop in exports could dip corn’s 2024 stocks by 245 million to 2.017 billion.

Our IL crop tour revealed many heavily podded fields. However, the US G/E rating being 9% below the 5-yr US average suggests a possible 1 bu lower US yield to 51 for a 4.22 billion bu crop. Strong US bean oil demand suggests a 6 million rise in 2022/23’s crush, but the size of 2023/24 US crop will determine if the US stocks decline 80 million this month or not.

Dry N Plains & PNW weather and lower harvest reports suggest a 15 million bu smaller US wheat crop tightening stocks to 577 million. The collapse of the Black Sea deal opens up the possible expansion of US wheat exports going forward.

What’s Ahead:

Despite smaller US corn & soybeans yield ideas for USDA’s August report, World weather & the Black Sea conflict will likely be August’s price factors. Late July price strength finalized old-crop corn at $5.50-60 & beans at $15.50-80. Nov bean sales were upped to 50% in the $14.30- 50 range while KC wheat push to $8.90 increased 22 & 23 sales to 45%. Hold balances for now.

More By This Author:

US 2023/24 Stocks Change Modestly, But Weather Stays ImportantDespite Lower US Soybean Acreage, Trade Watching Nearby Weather

Dramatic Corn And Soybean Seeding Changes

Comments

Log in or sign up to join the conversation.