Uranium Is In A Legit Bull Market

Image Source: Pixabay

Uranium stocks are having another big day. So in honor of their extremely positive impact on our portfolio, here are two backgrounders, the first on uranium’s recent history and likely future from commodities analyst Marin Katusa, and the second from uranium consultant Per Jander on how the business works:

The Black Swan Event about to Spike Uranium—Again

By Marin Katusa

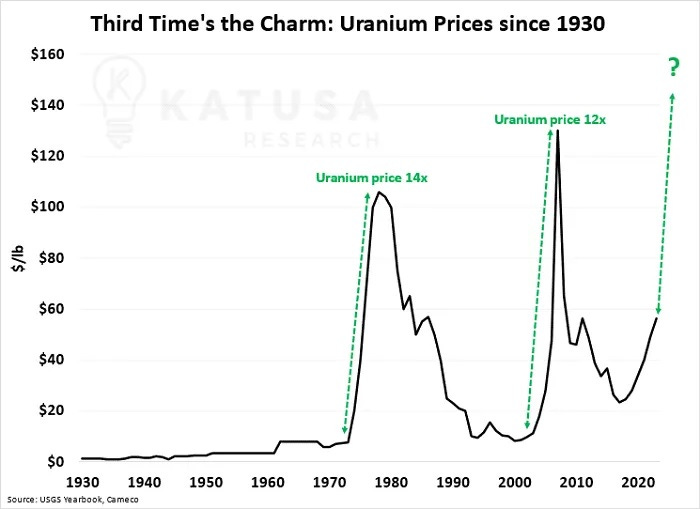

Twice in the past fifty years, the price of uranium has shot up 600%.

Both were due to a “black swan” event—one that cannot be predicted, but completely alters the landscape of an industry.

Another such event is taking place right now.

And it’s likely to have a similar effect on the price of uranium.

To understand it, you need to know what caused the first two “black swans.”

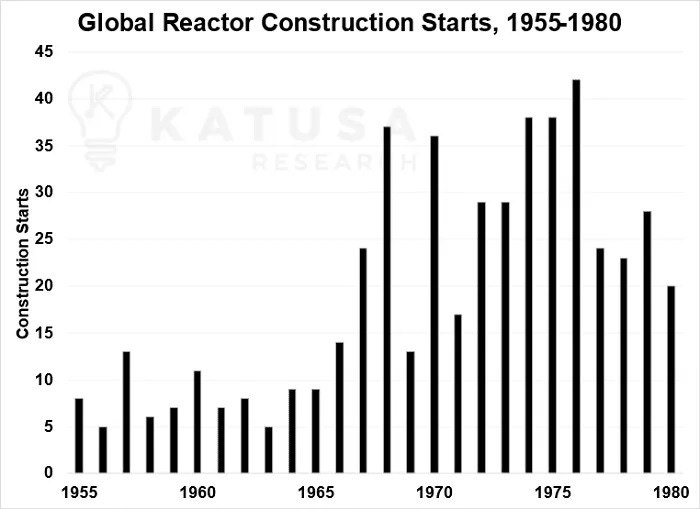

The first occurred in the mid ‘70s, when the global nuclear reactor buildout began to gain momentum and go global.

Nuclear reactors require a lot of uranium to start up and operate, and it can take more than a decade to get a new uranium mine online.

Utilities became extremely concerned that they wouldn’t be able to actually run their expensive new reactors when they were finished.

And it didn’t look like the world would slow down building new nuclear reactors any time soon.

In just four years, a run on uranium took it from $6/pound to $42/pound—or over $200/pound in 2023 dollars.

Of course, every boom has a bust, which is exactly what the Three Mile Island accident did to the uranium market. Sentiment toward nuclear changed, new construction dried up, and the price of uranium fell… and fell… and fell some more.

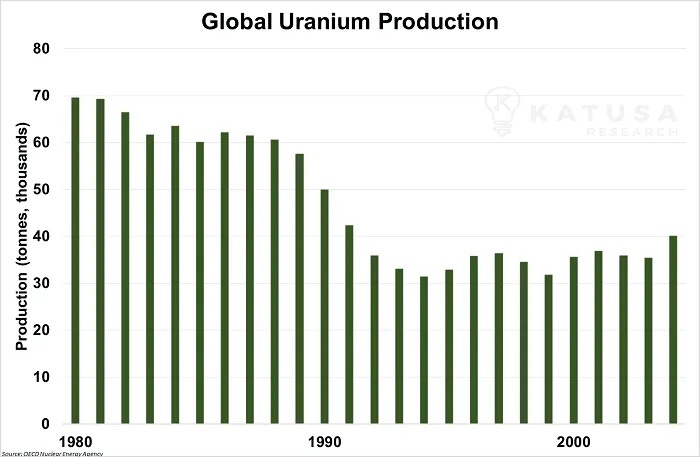

By 1990, it was sitting right back at $7/lb., and utilities were sitting on huge stockpiles of uranium.

And uranium producers were sitting on huge losses from mining.

So they devised a slick solution: cut production. A lot.

For fifteen years, mine after mine was taken offline to create an artificial uranium shortage.

From 1980–1995, uranium production was cut by more than 50%.

Years of overproduction seemingly took forever to use up. By 2001, uranium was back at… still $7/lb.

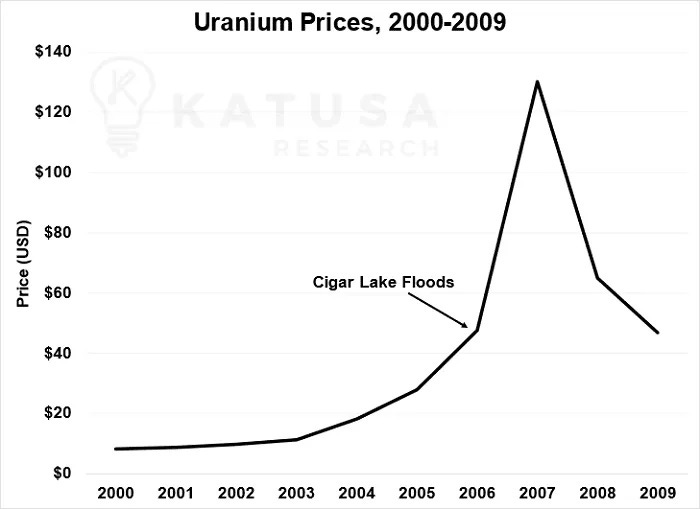

But in early 2006, the price finally broke free.

Black Swan #2 took the form of a single busted pipe at an unfinished uranium mine in central Canada called Cigar Lake.The Wrench Twist Heard ‘Round the World

Cigar Lake held the largest reserve of high-grade uranium, at 100x the average grade, anywhere in the world.

When it was complete, Cigar Lake was intended to produce more than 10% of the world’s supply.

But when a small standpipe sprang a leak, two workers trying to fix it accidentally broke a valve completely off.

The resulting gush of water couldn’t be stopped, and the mine flooded—several times. Mine development couldn’t resume for four years.

Pay attention to what happened next… because it’s happening again.

The existing mines that were built, like Cigar Lake, are not meeting production guidance because of equipment reliability issues, supply chain delays, and lack of trained personnel. Which all contributed to lower uranium production than expected.

Supply issues are happening across all mines globally.

The mere possibility of a tighter supply,

Combined with planned nuclear construction around the world, sent shockwaves through the entire uranium market.

Producers, wanting to get more money for their metal, held onto their uranium as the price rose.

Utilities, the primary buyers of uranium, grabbed as much as they could—again afraid of not being able to buy enough inventory to keep reactors running.

Spot prices spiked from $20/lb. to $140/lb. in early 2007— a second 600% gain.

But ultra-high uranium prices led to historically high exploration and production, and the price began to drift back to normal.

Then Fukushima happened in 2011, and it was Three Mile Island déjà vu.

As major developed countries like Japan and Germany pulled away from nuclear altogether, producers just kept producing uranium.

As a result, the price of uranium fell to one of the lowest inflation-adjusted levels in history. And it stayed there.

The low price forced hundreds of mining companies into bankruptcy and others to completely exit the uranium sector to stay alive.

The number of uranium miners listed on the ASX and TSX cratered—from 585 to about 50.

More than 70% of the market value of major listed producers was erased.The OPEC of Heavy Metal Throws Its Weight Around

So uranium companies returned to their old strategy: “production discipline.”

In short, that means keeping uranium in the ground until it becomes valuable again.

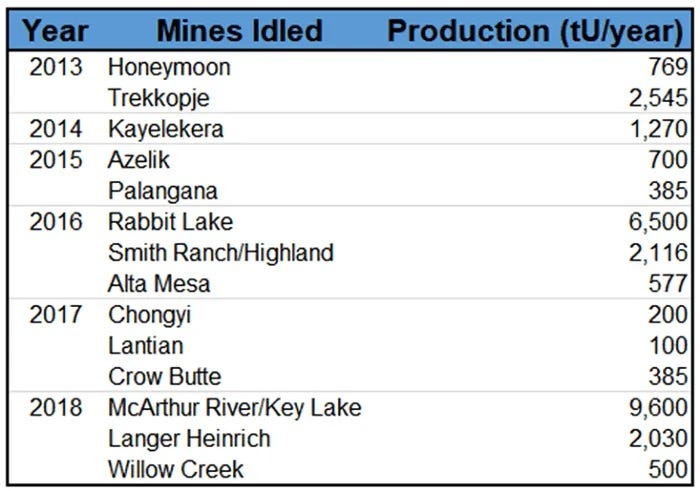

In 2013, the largest producers of uranium began to take mine after mine offline.

Then the unthinkable happened.

You see, about 40% of the world’s uranium is mined in Kazakhstan, a former Soviet state.

That makes Kazakhstan effectively a single-member OPEC; their decisions around uranium can singlehandedly dictate its price.

And in January 2017, Kazakhstan cut production by 10%.The rest of the world got the signal...

A few months later, the McArthur River mine in Canada shut down—and 15% of global uranium production went offline. Cameco announced that the suspension was “for an indeterminate period” due to low uranium prices.

By 2018, more than 50% of global uranium demand had been cut from production.

And a single company had removed more than twice the annual global demand:

“Since 2016, we have removed more than 190 million pounds of uranium from the market.”

– Cameco president and CEO Tim GitzelThen came another twist: COVID.

In March 2020, production at Cigar Lake (the formerly flooded mine) was suspended. The next month, Kazakhstan reduced operations at all of its uranium mines.

To be clear, the shutdowns had little to do with COVID. Otherwise, mines would have come back online the next year.

Instead, global uranium production in 2022 was only 3% higher than in 2020.

The shutdowns were all about further shrinking supply so uranium miners could eventually capitalize on skyrocketing uranium prices.

In fact, of the top seven uranium-producing countries in the world, five of them cut production between 2021 and 2022.

In 2022, Cameco stated: “We are continuing with indefinite supply discipline.”

The uranium market is rapidly shooting from oversupplied to severely undersupplied . . . and no new supply is coming online soon.

“For some time now we have said that the uranium market is as vulnerable to a supply shock as it has ever been, due to persistently low prices.”

– Cameco president and CEO Tim GitzelUtilities are just beginning to notice that there’s very little uranium to go around.

Even the COO of Kazatamprom, Kazakhstan’s nationalized uranium producer, has gone on record saying that there simply isn’t enough uranium for the next contracting cycle.

If you think you’ve seen all of this before, it’s because you have.

The first spike was caused by a run on uranium by utilities. The second was an accidental removal of uranium production from the market.

This time, it’s both.

Because mine operators have already deliberately taken massive production offline—and utilities are just beginning to make a run on uranium.

History doesn’t repeat itself—but it certainly does rhyme. So you know what comes next.

We’re one busted pipe away from $150/lb uranium.

But there’s a THIRD EVENT unfolding that no one could have predicted or anticipated—and it’s one that will irrevocably alter the course of global uranium demand.

How the uranium market works

Uranium consultant Per Jander via Commodity Culture’s YouTube channel:

Video Length: 00:31:20

More By This Author:

Finally, The Housing CrashPeter Zeihan: China Is Collapsing -- Now

Gold Is Doing Great -- In Other Currencies