Image by Carlos Lincoln from Pixabay

Central banks endlessly fascinate me. The more I research them the more contradictions I find, particularly since their missions and impacts changed over time. Take the Federal Reserve (Fed), for example. It was originally created to countercyclically balance volatile market forces in times of stress. However, the evolution of financial concepts—most notably money and inflation—has turned the Fed upside down. It no longer acts as a stabilizer. Rather, the Fed’s actions are now procyclical. Today, its monetary policy is fanning the flames of shortage-induced inflation.

From cronies to currency to macro

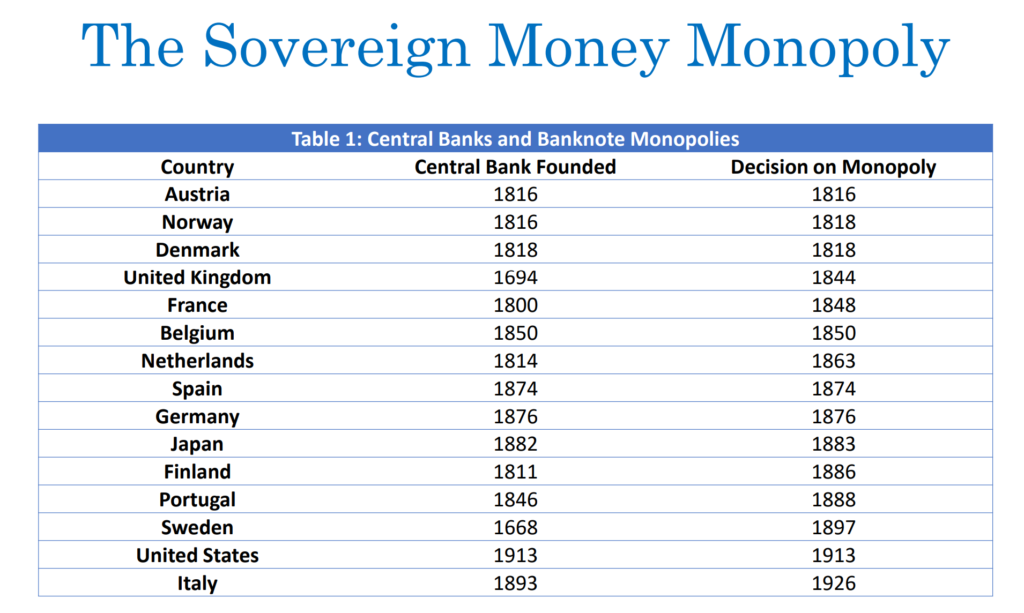

Central banks are a relatively new phenomenon in the modern world. Like many things, they’ve evolved. The first ones were private organizations that were granted special, privileged status by governments in return for purchasing their debts. Specifically, these early central banks were granted monopolies over the issuance of banknotes (which served as national currencies) in exchange for lending governments much-needed funds. These include the Swedish Riksbank (1668), the Bank of England (1694), and the Banque de France (1800).

Central banks have long histories of banknote monopolies. Source: Gary Gorton, The Future of Money

Central banking evolved (in part) with the founding of the Fed. The Fed was specifically created to help stabilize the volatile commercial banking sectors after the Panic of 1907. It was supposed to provide an elastic currency at times when interbank lending left the private sector short on liquidity and susceptible to bank runs.

However, the Fed’s role officially changed in 1977. Congress amended the Federal Reserve Act tasking

the Fed with its now infamous Dual Mandate. The Fed’s purpose shifted from managing the “money supply” to promoting “maximum employment, stable prices, and moderate long-term interest rates.” These vague and unspecified tasks forever changed the role of central banks in our economies and markets.

Today, the Fed targets inflation

Today, the Fed’s Dual Mandate is interpreted as an inflation target. The Fed—and other central bankers—seek to keep inflation at 2%. Inflation is defined as the general change in the price of some basket of goods and services. Which goods, which services, and in what quantities are constantly debated. Each market participant and economist has his/her preferred metric, be it the Consumer Price Index (CPI), Personal Consumption Expenditures Price Index (PCE), CPI excluding food and energy, core PCE, the price of gold, etc. Importantly, inflation no longer stands for monetary debasement (as there are no monetary standards to debase in fiat currency regimes; more on that here).

Thus, inflation is subjective. Its presence, amount, and scope are constantly disputed. What’s not contested, though, is how the Fed achieves its target. It’s widely held that adjusting the Federal Funds Rate (FFR) does the trick.

The orthodoxy guiding policy in the post-WWII era was Keynesian stabilization policy, motivated in large part by the painful memory of the unprecedented high unemployment in the United States and around the world during the 1930s. The focal point of these policies was the management of aggregate spending (demand) by way of the spending and taxation policies of the fiscal authority and the monetary policies of the central bank. The idea that monetary policy can and should be used to manage aggregate spending and stabilize economic activity is still a generally accepted tenet that guides the policies of the Federal Reserve and other central banks today.

Michael Bryan, The Great Inflation

According to this Keynesian stance, which most academics support, the Fed impacts demand by adjusting the FFR. Raising it can “cool down” an overheated economy while lowering the FFR can stimulate an under-utilized one. Without getting into the details, the theory rests on the Taylor Rule which links interest rates to levels of aggregate demand. As described below:

… the theory …is based on the view that the economy can move above or below a full market-clearing equilibrium in the short run—called a “demand gap.” A positive demand gap means the economy is overheated; a negative demand gap means it is operating below capacity. Other than random shocks, the main disturbance preventing general equilibrium is a deviation of the real interest rate from the natural interest rate. The policy solution is to adjust the nominal fed funds rate to move the real rate to the natural rate. … Instead of using money supply as a policy tool, the Fed follows a Taylor rule in setting the fed funds rate target. To the extent that it can align inflation expectations with its own ultimate inflation target, the Fed is able to get actual inflation in its target range (typically close to a measured 2 percent rate).

Dimitri B. Papadimitriou and L. Randall Wray, Still Flying Blind After All These Years: The Federal Reserve’s Continuing Experiments with Unobservables

This theory drives the Fed. It primarily conducts monetary policy by adjusting the FFR with the explicit goal of achieving a 2% inflation rate. The Fed believes that changing the FFR impacts the overall level of demand for goods and services in the United States. According to the law of supply and demand, lower demand should lead to lower prices—on average—and vice versa. It’s a neat little theory.

Well, so, as I mentioned, you can see places where the demand is substantially in excess of supply. And what you’re seeing as a result of that is prices going up and at unsustainable levels, levels that are not consistent with 2 percent inflation. And so what our tools do is that as we raise interest rates, demand moderates: it moves down. Interest rates, you know—businesses will invest a little bit less, consumers will spend a little bit less. That’s how it works. But, ultimately, getting those, getting supply and demand back, you know, back in balance, is what gives us 2 percent inflation, which is what gives the economy a footing where people can lead successful economic lives and not worry about inflation.

Jerome Powell, FOMC Press Conference, May 4, 2022

Bad in practice

While orthodoxy today, some economists note that the “empirical evidence for this [theory linking interest rates to demand] is surprisingly weak … .” Interest rates simply don’t impact commercial investment and consumer spending as theorized. Thus, the interest rates-inflation link seems more myth than science. Yet this theory drives monetary policy, globally.

The theory is that as interest rates rise, borrowers decide to borrow and spend less. The empirical evidence for this is surprisingly weak, for the most part. Empirical estimates of the elasticity of spending with respect to the interest rate generally show it does not matter much—with the exception of purchases of residential real estate. Low rates probably boost asset markets (including housing), but that does not feed directly into inflation.

Dimitri B. Papadimitriou and L. Randall Wray, Still Flying Blind After All These Years: The Federal Reserve’s Continuing Experiments with Unobservables

As an investor closely following individual companies for nearly 20 years, I’ve always found this popular theory bizarre. Prices are not a plaything for academics or central planners. They play a specific and vital role in commerce. By utilizing the language of money, prices mark the value at which items are trade. As a result, they facilitate the movement of value from producer to consumer.

It should be obvious that prices are not set from the top down. Rather, each business (and individual) engaged in trade meticulously derives them one by one. The goal, however, is not to maximize prices. Businesses seek to maximize profits. Prices are just a means to a business’s end.

Profit maximization is not an abstract concept or “something nice to have.” It is a matter of survival. Each business consumes resources in order to create higher-value ones. Every input, from energy, labor, unfinished goods, websites, real estate, and financing must first be acquired and organized before they can be transformed into output sold to others. Profit measures the value produced in this process. A loss represents a net consumption of resources. Thus, a money-losing entity cannot survive on its own. It consumes more than it produces and ultimately must perish (unless injected with fresh, outside capital).

“I have to raise prices when I raise wages. That’s just how it works,” said Herridge, who doesn’t have enough staff to get all of his Burger King locations back to 24-hour operations. “That’s going to be the primary driver of inflation still over the next year or so.”

Burger King and Qdoba franchisee Matt Herridge, Bloomberg

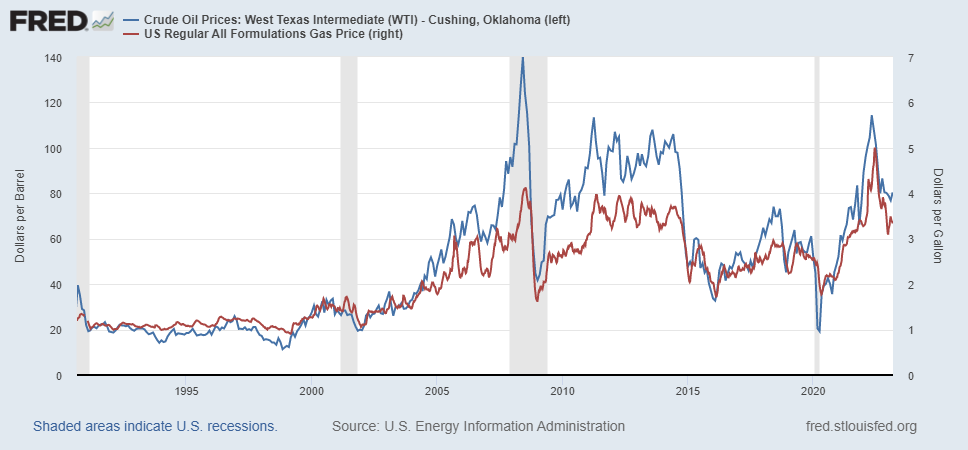

Unsurprisingly, businesses respond to rising input costs by raising prices. Their revenues must keep up. Failure results in hardship and, potentially, catastrophic failure. Look no further than your local gas station. When the price of (crude) oil increases so too does the price of gasoline at the pump. The gas station does not concern itself with a drop in demand (at least initially). It’s focused on survival. The same holds for every item.

Gasoline prices are tightly correlated with the price of crude oil from which it’s derived.

Contrary to theory, the Fed is forcing businesses to raise prices by hiking the FFR, both directly and indirectly. Higher interest rates lead to higher financing costs which must be paid for with revenue. While not all companies employ debt, all consume capital. Thus, raising the cost of capital impacts all commercial ventures, to varying degrees.

Money is more than financing

The cost of capital is an important corporate finance concept. It describes how much a company would pay for external financing at a given time. Thus, businesses consider it when funding new initiatives or evaluating M&A. Investors use it to value companies.

Interest rates are one factor in a company’s cost of capital. The other is the return on equity that shareholders would demand. Thus, the Fed can broadly impact companies’ cost of capital by adjusting the FFR (though, just in part). This thinking motivates the conventional demand view which assumes that higher financing costs lead to less investment and thus, lower spending. Though, this theory not is not well supported for the reasons already mentioned.

Careful study by Steven Fazzari [in his study] has shown that for most types of firms, the interest rate is not an important determinant of investment spending, which is considered to be the classical transmission mechanism of monetary policy. In theory, raising rates should reduce investment and thus aggregate demand through the investment spending multiplier—in theory, but not in practice, for the simple reason that what matters is expected profits. When optimism is high, a few percentage points higher borrowing costs do not change the net returns much.

Dimitri B. Papadimitriou and L. Randall Wray, Still Flying Blind After All These Years: The Federal Reserve’s Continuing Experiments with Unobservables

This common perspective’s flaws can come to light through a better definition of money. Properly understood, money is an abstraction that quantifies all real-world things. Everything can be translated into money terms and categorized as an asset or liability. Financial statements precisely serve this purpose. Thus, interest rates represent more than the cost to borrow funds today. They represent the cost of everything currently used in production. After all, we borrow capital to exchange them for things we want, not to horde it. Higher capital costs are higher costs, period.

Thus, raising the FFR makes all cost inputs more expensive. Businesses must respond to these higher input costs by raising prices in order to cover their expenses, protect their profits, and survive. Contrary to popular belief, rising interest rates create inflation! The Fed’s got it precisely backward.

Higher interest rates stoke, not dampen, inflation

Central banks have played evolving roles in economies and markets. While first employed as government funding schemes, they now play macroeconomic policy roles. Most famously, central banks seek to control inflation with monetary policy.

The Fed targets a 2% inflation rate by adjusting the FFR. According to theory, raising it should lower inflation via its impact on demand (and vice versa). However, facts don’t support this orthodoxy. Businesses raise prices in response to rising input costs. Higher interest rates create higher financing costs which must be paid for with higher revenues and prices.

However, money is more than investment capital. It’s an abstraction for every existing component of a business. Thus, raising capital costs raises the cost of all inputs, not just financing. As a result, businesses must respond to higher interest rates with price increases or run the risk of ruin.

The Fed’s got monetary backward. Higher interest rates fuel inflation due to their supply-side impacts, not dampening it via demand. This confusion has transformed the Fed from a countercyclical liquidity provider to a procyclical inflation stoker.

More By This Author:

Inflation No Longer Has Monetary ApplicationsWhy I’m Waiting For The Fed To Pivot

Why Commodity Currencies Are Better Than Fiat And Crypto

Comments

Log in or sign up to join the conversation.