Seven Reasons Why We Should Not Depend On Imported Goods From China

It seems to me that the situation in China is far different from what most people think it is. Even if we would like to depend on China, we really cannot.

Reason 1. When we depend on goods from China, an amazingly large share of the world’s industrial activity gets concentrated in China.

The five largest users of energy in the world are China, the United States, India, Russia, and Japan. The International Energy Agency shows total energy consumption as follows for the year 2016:

(Click on image to enlarge)

Figure 1. IEA’s estimate of energy consumption (total fuel consumed, or TFC) by sector in 2016 for the top five energy-consuming nations. Mtoe is a million tons of oil equivalent. Source: IEA. Non-energy use is the use of fossil fuels as a material to create end products that are not burned. Examples include medicines, plastics, fertilizers, asphalt, and fabrics.

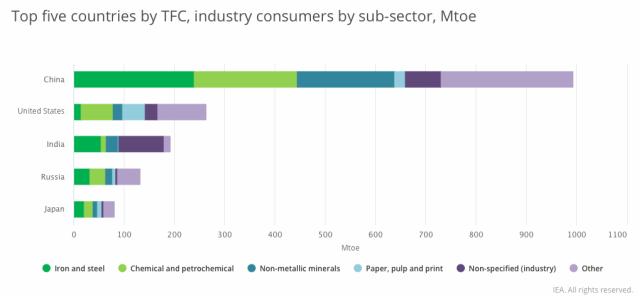

When these countries are compared, restricting our analysis to the portion of energy used by industry, we find the rather disconcerting result shown in Figure 2:

(Click on image to enlarge)

Figure 2. Chart by the International Energy Agency showing total fuel consumed (TFC) by industry, for the top five fuel consuming nations of the world.

China consumes more fuel for industrial production than the next four countries listed (United States, India, Russia, and Japan) combined. Of course, we don’t know exactly the corresponding amounts for other countries of the world, but we can observe that if a country is concerned about its CO2 emissions, the easiest way to reduce these emissions is to send heavy industry elsewhere, such as to China or India. There are likely many countries that are primarily service economies, thanks to the option of outsourcing most industry to other countries.

Much of the discussion I have read regarding sending industry elsewhere has been in the direction of, “As advanced as our economy is, we don’t need heavy industry; service jobs will substitute. The industry can be developed at lower cost elsewhere. Everyone will be better off with this arrangement. The invisible hand will provide jobs and goods and services for everyone.” In addition, corporations saw the possibility of adding customers from around the world. Not too many thought about the real-world problems that might result.

Clearly, there is a problem with the jobs being lost to China and other Emerging Markets. When new service jobs are added, they often do not pay as well the industrial jobs they replaced. In fact, there might not be enough jobs in total, if automation plays an important role as well.

Another issue is that the level of industrial concentration can be a problem. We are now depending on China and perhaps a few other countries to provide for a large share of the “stuff” we use. Even if China is not the only provider, it is often an important part of the supply chain. If something should go wrong (for example, widespread riots in China), we don’t have a Plan B.

Reason 2. China needs energy products to make the goods it uses for itself and for the goods it exports. China’s own energy supply is faltering. Because of China’s huge size, it is becoming increasingly difficult to keep China’s energy consumption rising sufficiently rapidly using imported energy.

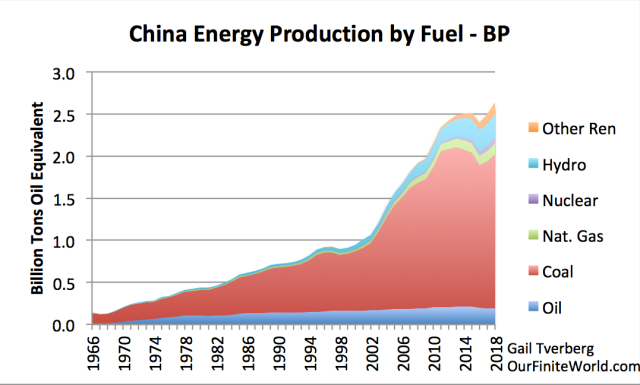

China’s own energy production is shown in Figure 3. (Note: Hot off the press! New BP report released this week.)

(Click on image to enlarge)

Figure 3. China energy production by fuel, based on 2019 BP Statistical Review of World Energy data. “Other Ren” stands for “Renewables other than hydroelectric.” This category includes wind, solar, and other miscellaneous types, such as sawdust burned for electricity.

It is easy to see that China’s coal production hit its highest point in 2013 and has stayed at a lower level since that date. Also, China’s highest oil production occurred in 2015, with lower production since that date. China’s total energy production has been rising recently, but only with great effort. Total energy production is only 8.9% higher in 2018 than it was in 2012, implying an increase of less than 1.5% per year, relative to 2012 amounts.

A standard workaround for inadequate energy production growth is imported energy products. Even with these imports, it has been impossible to keep total energy consumption rising as rapidly as it rose in the 2002 to 2007 period. The cost with imports is greater, also.

(Click on image to enlarge)

Figure 4. China energy production by fuel, plus line showing its total energy consumption (including imports), based on BP 2019 Statistical Review of World Energy data.

In 2018, China imported 71% of its petroleum (either as crude or as products), and 43% of its natural gas. It was the largest importer in the world with respect to both of these fuels.

In 2018, China’s coal imports shrank as its own coal production surged. This was almost certainly a change planned by China. China would much prefer producing its own coal (and keeping the jobs within the country) to importing coal from elsewhere. China imported 4% of its coal from elsewhere in 2018.

Reason 3. The commodity demand from China is so huge that, to a significant extent, it determines world commodity price levels. Where regional energy prices exist, China’s choice regarding whether or not to import from a country can influence local price levels.

Chile is the largest copper producer in the world. A recent article regarding problems associated with lower copper prices notes that Chile’s copper demand has been driven “almost entirely by the expanding Chinese economy over the last three decades.” For many commodities, China consumes over half of the world’s commodity supply. If China’s industrial demand is growing, prices will tend to rise, allowing more of the mineral to be extracted. Higher commodity prices tend to be needed over time because the ores of highest concentration (and otherwise easiest to extract ores) tend to be extracted first. Ores extracted later tend to be more expensive to extract, so higher prices are required for extraction to be profitable.

This situation of China playing an extremely large role in commodity prices holds for a very large number of commodities. If China is building widgets or any other product, using a particular commodity, China’s need to buy this commodity in the world market will tend to hold up world prices for the commodity. This situation holds even for fossil fuel prices.

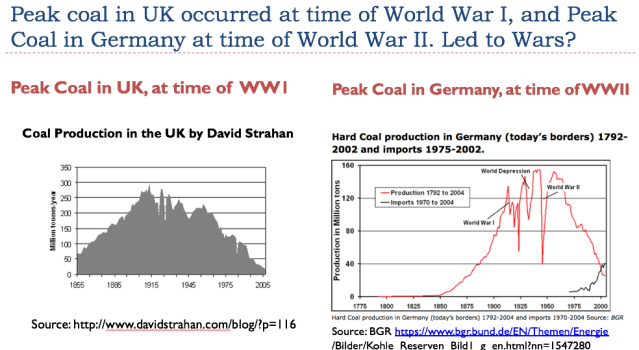

Reason 4. Over the next few years, China’s coal supply is likely to fall significantly because of depletion. This lower fuel supply is likely to lead to a shrinkage of China’s industrial capability, and, indirectly, falling world commodity prices of all kinds.

The problem that China is encountering in Figure 3 is “peak coal.” This is a similar problem to that encountered by the United Kingdom immediately before World War I, and to that Germany encountered just before World War II.

(Click on image to enlarge)

Figure 5. The timing of the peaks is peculiar, relative to wars.

Coal tends to be the industrial fuel of choice because it is cheap. Goods made with coal tend to be inexpensive, especially if wages paid to workers are low and if the company making the goods does not spend much money on pollution prevention. Hydroelectric can be an adequate substitute for coal if the water flow can be depended upon. Wind and solar are too intermittent and not sufficiently inexpensive to be adequate substitutes for coal. Wind and solar (included in “Other Ren” in Figure 3) are also far smaller in quantity than coal.

Outsourcing a large share of the world’s manufacturing to China seemed like a great idea back when it was started, often in the early 2000s. If at some point, China cannot really handle the responsibility it has taken on, outsourcing gets to be a huge problem.

The reason why coal prices cannot rise very high is because if they do, the prices of finished goods will need to rise as well. Wages of workers around the world will not rise at the same time because the higher cost of production takes place due to something that is equivalent to “growing inefficiency.” The coal mined is of lower quality, or in thinner seams, or needs to be transported further. This means that more workers and more fuel is needed for each ton of coal extracted. This leaves fewer workers and less fuel for other industrial tasks, so that, in total, the economy can manufacture fewer goods and services. Because of these issues, countries experiencing peak coal are pushed toward economic contraction.

Unfortunately, rather than leading to high prices (to compensate for the higher extraction costs), running short of inexpensive-to-extract fuel tends to lead to war, or to tariff fights. Countries whose coal is depleting will try to maintain their own supply as long as possible. They will invent excuses to stop importing coal. Back in September 2018, the Financial Review reported, “China has introduced unofficial restrictions on coal imports in a bid to prop up domestic prices by slowing down customs approvals at key ports.” China needed higher internal prices to make it profitable to extract coal from its depleting coal mines.

(Click on image to enlarge)

Figure 6. Chart showing prices of Brent Oil, China Qinhuangdao Spot Coal price, and Asian Marker Coal, all in US$ of the day. Amounts from BP 2019 Statistical Review of World Energy. Note also that the units of coal (ton) are much larger than the units of oil (barrel) used on this chart. Thus, the same number of dollars of buys a much larger quantity of coal than of oil; coal is cheaper.

If higher coal prices really were possible over the long term, it would make it possible to open new mines in more distant locations. The location of coal mines is important because transport costs by rail or truck tend to be high. China built the large ghost city of Ordos, Inner Mongolia, on the expectation that coal prices would rise, making development of coal in the area profitable. Unfortunately, coal prices fell, making the project not economic. I visited the area in 2015, after teaching a short course on Energy Economics in Beijing. There was a large almost empty airport, and few vehicles were using nearby multi-lane roads.

Reason 5. All of the concern about future tariffs artificially raised China’s 2018 industrial production and commodity prices. Because production was brought forward into 2018, China’s production and world commodity prices can be expected to be lower in 2019 and in future years.

Manufacturers wanted to front-run tariffs, so they tended to ramp up production in advance of the tariff implementation date. This higher production, in turn, tended to raise commodity production and prices around the world. Note in Figure 6, above, that coal and oil prices are both higher in 2018 than in 2017. Prices in 2019, not shown, are tending to trend downward again.

China badly needed higher coal prices in order to help its coal extraction. Thus, part of the reason that China was able to continue to function as well as it did in 2018 was because of all of the discussion about future tariffs. If this discussion had not taken place, employment in China would likely have been lower. With this lower employment, sales of automobiles and smartphones would have been lower as well.

Note, too, that even with the demand brought forward into 2018, China’s economy was not functioning very well in 2018. Private passenger automobile sales for the year fell by 4%. Smartphone sales fell by a worrisome 15.5%. Clearly, workers were having difficulty buying the kinds of goods a person would expect a growing economy to be selling. I would attribute these problems to the peak coal problem mentioned earlier, making it increasingly difficult to increase the amount of industrial operations provided by China’s economy.

Reason 6. The Chinese economy has been gradually changing and adapting to hide its energy problems. Even more, changes will be needed in the future, potentially affecting the world economy, with or without tariffs.

The Chinese economy reports carefully massaged GDP numbers, which many analysts consider to be inflated in recent years. Its debt level keeps rising to try to keep all of its operations going.

We know that China discontinued one major industry at the beginning of 2018: recycling plastic and other types of low-valued recycling. With low oil and natural gas prices, this type of recycling cannot be profitable. Of course, discontinuing a major industry can be expected to lead to a loss of jobs within China. But, on the positive side, it frees up coal and other energy resources in China for other industries that can (perhaps) make more profitable use of them.

On a world basis, the loss of the plastic recycling industry becomes a problem. If rich countries are willing to subsidize the cost of sending plastic recycling to China, this subsidy allows containers that bring goods to rich countries to be sent back to China with a paid load inside. Thus, operating the plastic recycling industry helps keep the cost of shipment of goods from China to the US or Europe down because the shipping costs only need to cover the one-way cost of transit, rather than also covering the cost of shipping the empty container back. Without the subsidy to pay the freight of the plastic recycling, costs for the shipping industry rise, making international trade more expensive. Eliminating the subsidy that rich countries are paying to ship otherwise-empty containers back full of mixed trash is part of what pushes the world economy to contraction.

Other countries are not taking over very much of China’s role in recycling plastic, either. The net effect is that the loss of recycling is one of the things pushing the world toward contraction.

China has no doubt been cutting back in other ways as well. It is likely that it is not building as many uninhabited cities and roads that are really not needed. Ugo Bardi recently posted this chart showing global cement production.

(Click on image to enlarge)

Figure 7. World Cement Production by Ugo Bardi from a blog post on January 19, 2019.

China produces over half of the world’s cement; part of the reduction we are seeing relates to China’s falling use of concrete in new buildings and roads.

In some cases, China is moving in the direction of being a service economy. A recent video states that of the $237.45 cost of producing an iPhone in China, Chinese workers only provide assembly services, worth $8.46. The US contributes $68.69 of the cost, mostly in the design and distribution phases. The parts are generally outsourced from other parts of the world.

One way of looking at what is happening in China’s economy is to analyze the country’s oil consumption in terms of the relative amounts of diesel (used primarily by industry) and gasoline (often used by private passenger vehicles).

(Click on image to enlarge)

Figure 8. Gasoline and diesel consumption for China, based on data from 2019 BP Statistical Review of World Energy.

Based on Figure 8, it appears that China’s industrial growth suddenly leveled off about 2012. This, not by coincidence, is about the time that China’s coal problems were becoming apparent in China. China’s gasoline consumption has continued to rise, however. It appears that once it became apparent that its coal supplies were starting to seriously deplete, China began to “grow” China’s economy more as a service economy. After 2012, most growth seems to have come in the non-industrial sectors of China.

Reason 7. A major concern should be a financial collapse, far worse than 2008, both in China and for the world as a whole.

The world needs a growing energy supply to support the world economy. China is increasingly having difficulty with its energy supply. When China has trouble with its energy supplies, the world as a whole has a problem with its growth in energy supplies.

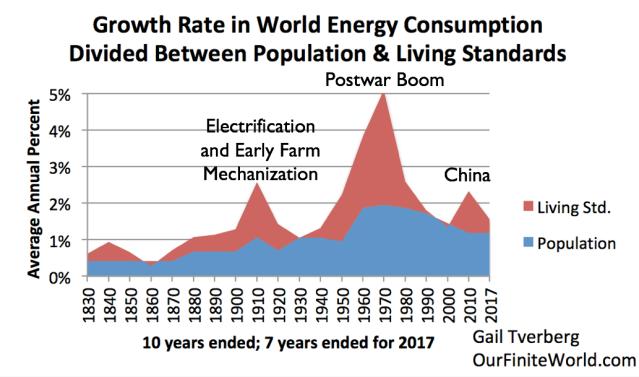

A few months ago, I showed the role China has played in the world economy is this chart:

(Click on image to enlarge)

Figure 9. Ten-year growth in world energy consumption, divided between the blue portion associated with rising population, and the red portion associated with higher energy consumption per capita, which I have called “Living Std.”, meaning “Higher Living Standards.”

China added a little bump in GDP growth at the end of the nearly 200-year time period shown, after it joined the World Trade Association in December 2001. The energy added by China (mostly in the form of coal) allowed the world economy to continue to grow, when it otherwise would have been up against limits.

Now we are reaching a situation where China’s energy production is likely to flatten or fall because of the depleted state of its coal mines, and the fact that coal prices can’t rise high enough, for long enough, to open new mines. The world economy, over the period shown, has always had rising energy consumption. In most cases, energy consumption rose faster than population growth, allowing some growth in the standard of living over time.

Changing to a situation of shrinking energy consumption per capita would likely be extraordinarily traumatic. The population would likely fall. Commodity prices would drop to low levels. Debt would tend to default; prices of shares of stock would fall. Many governments would fail. If shrinking energy consumption per capita starts in one country (whether China or elsewhere), it could easily spread to other countries around the world.

We don’t know what is ahead, but we know that the low points in Figure 9 were very bad times, even though energy consumption in total was not contracting. The decade of 1860 to 1870 was the decade of the US Civil War. The decade of the 1930s was the decade of the Great Depression. The decade of the 1990s was the decade of the collapse of the central government of the Soviet Union.

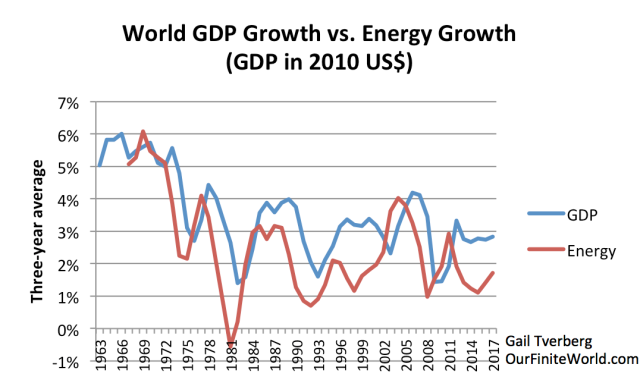

We also know that world energy consumption and GDP growth tend to be highly correlated.

(Click on image to enlarge)

Figure 10. World GDP Growth versus Energy Consumption Growth, based on data of 2018 BP Statistical Review of World Energy and GDP data in 2010$ amounts, from the World Bank.

This is as we would expect because energy consumption is required for the many aspects of GDP growth. Transportation, heating and/or cooling, and electricity all require energy consumption, for example.

The recent divergence between GDP and energy consumption in Figure 10 may be the result of overstated GDP amounts by China, India, and other countries. If a country wants to appear inviting for new investment, there is a temptation to overstate GDP since other countries seem to be doing so, without penalty.

Back during the Great Recession of 2008-2009, our problem was with homeowners who took out loans that were far higher than they could really afford. Today, we have whole economies taking on more debt than properly stated GDP reports would suggest they are able to handle. We go from one version of optimism regarding debt levels to another.

Conclusion. If a person doesn’t understand how badly the energy situation is working out for China, or how important energy consumption is, it is easy to think that the problems China is facing are primarily tariff-related. In fact, China’s situation is a very worrisome one, with or without tariffs being added.

To fix the situation, China would need a very cheap, non-intermittent, locally produced, non-polluting additional energy source. This energy source would also need to be rapidly scalable. Such an energy resource doesn’t appear to be available.

Disclosure: None.

I have questions about this article. An amazing amount of production is concentrated in China because China has 1.4 billion people. So poin 1 really is hard to understand. Point 2 really has more to do with China's internal policy than reasons why we should not import from them. As the author states, the world depends on China's energy fulfillment, because the world depends on China! But saying that means we can buy from elsewhere seems like wishful thinking. JMO.