In opening articles, I focus on the main commodities associated with a company –> copper, uranium, gold, silver, lithium, etc. The Company in this case is a gold (“Au“) junior. There’s essentially only one topic most want to hear about on Au, the price!

Au is +50% from a 2-yr. low in September 2022 to US$2,412/oz., within 3% of an all-time high! That’s an epic move, comfortably outpacing increases in All-in Sustaining-Costs (“AISC“).

Second-quarter results are coming in very strong, just imagine what 2H 2024 will bring. Shares of Agnico Eagle, Kinross, IamGold, Harmony Gold & Eldorado Gold are up an average of +98% from 52-week lows. Just look at this Au chart… will high-quality junior miners remain depressed or bounce?

(Click on image to enlarge)

Majors, including; Newmont, Barrick, Agnico Eagle, AngloGold Ashanti, Kinross, Gold Fields, and Alamos Gold have pristine balance sheets and are printing money. They’re stacking so much cash, they need to make acquisitions to justify their soaring valuations.

Mid-tier producers want to beef up production pipelines and become attractive targets themselves. The best M&A targets are in safe jurisdictions, can commercialize quickly (low operating / technical risks), and have blue-sky exploration upside.

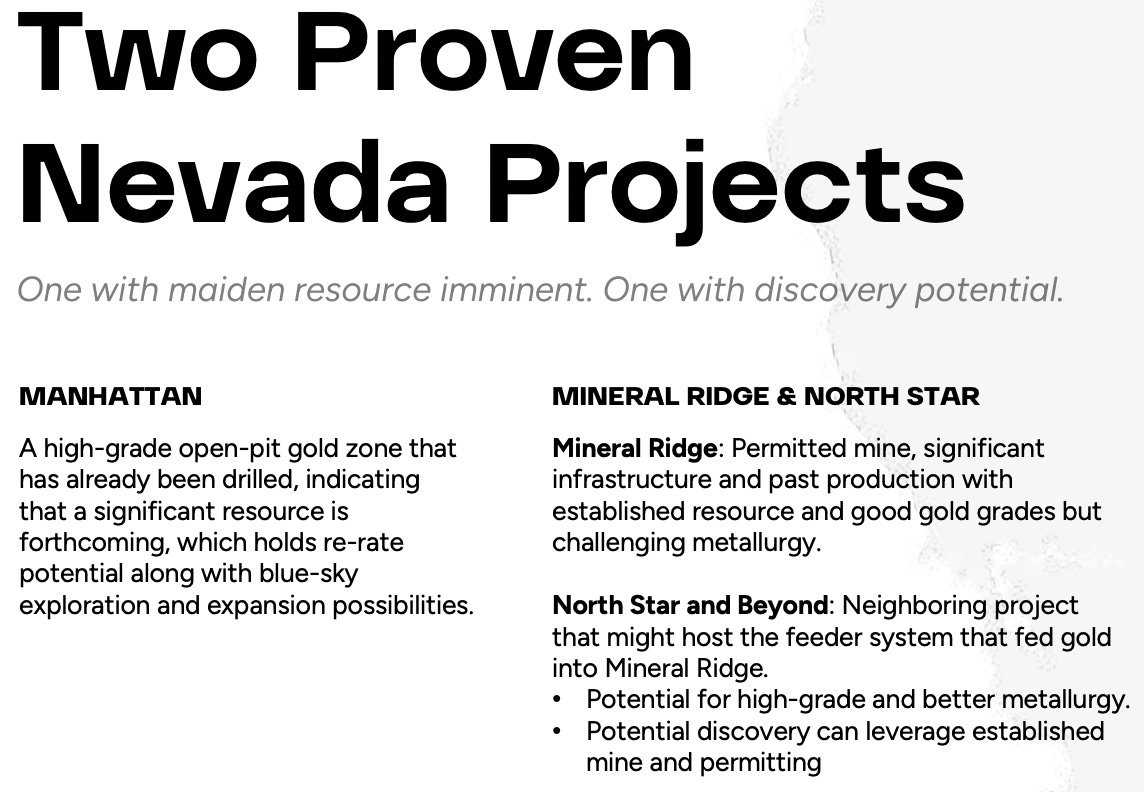

Scorpio Gold (TSX-v: SGN / OTCQB: SRCRF) holds 100% interest in the past-producing Manhattan/Goldwedge (with a permitted 400-ton/day gravity mill) & Mineral Ridge [“MR“] mines in Nevada’s world-famous Walker Lane Trend.

The Company’s consolidated Manhattan District comprises the advanced exploration-stage Goldwedge project. Adjacent to Goldwedge is the Manhattan Project, centered on two past-producing pits.

(Click on image to enlarge)

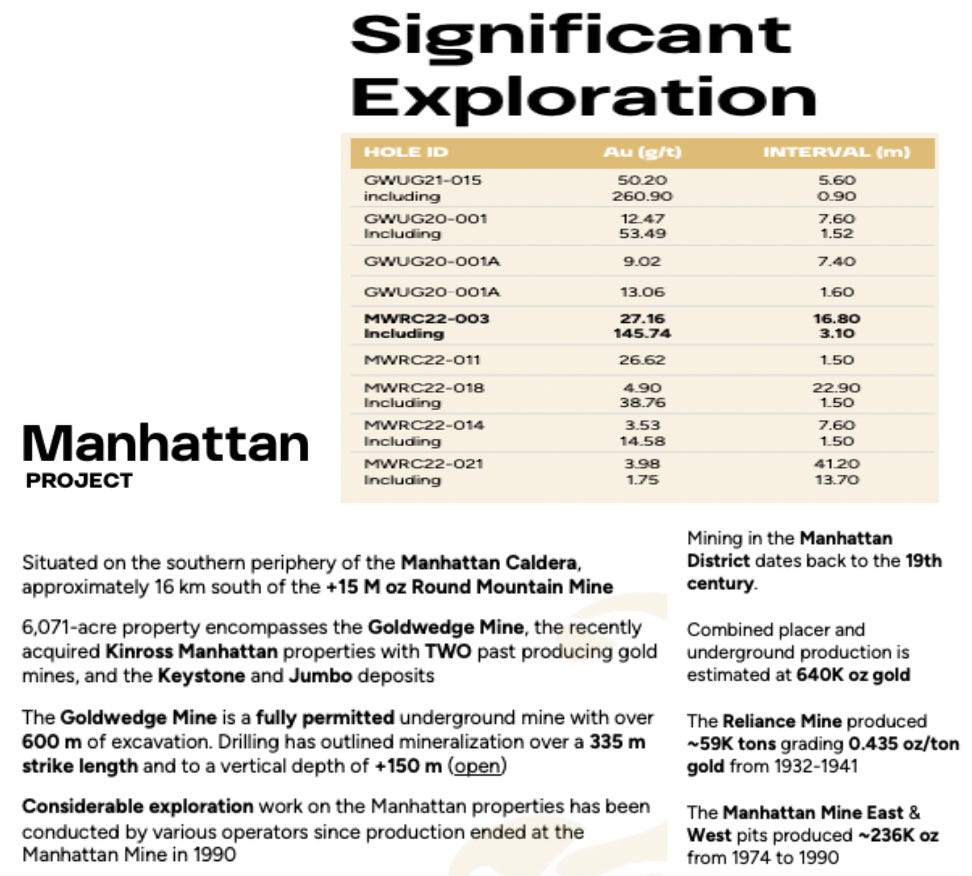

Both projects enjoy extensive permitting & water rights. Manhattan was acquired from Kinross in March 2021. Since then, Au is up nearly $700/oz.! This is a valuable project with over 100,000 meters of historical drilling. Manhattan boasts some serious high-grade results, incl. 5.6 m @ 50.2 g/t Au & 16.8 m @ 27.2 g/t Au.

Drilling 100k+ meters in Nevada today would take years and cost more than twice Scorpio’s current enterprise value {market cap + debt – cash} of ~$20M. The combined replacement value of the decades of work done on [Manhattan/Goldwedge + the 400 tpd Mill] & MR/Northstar is > $100M.

The 2,457-ha Manhattan property encompasses the Goldwedge Mine, the acquired Kinross Manhattan properties with two past-producing mines, and the Keystone & Jumbo deposits. Manhattan is a high-grade open-pit Au zone with a significant mineral resource estimate expected within six months.

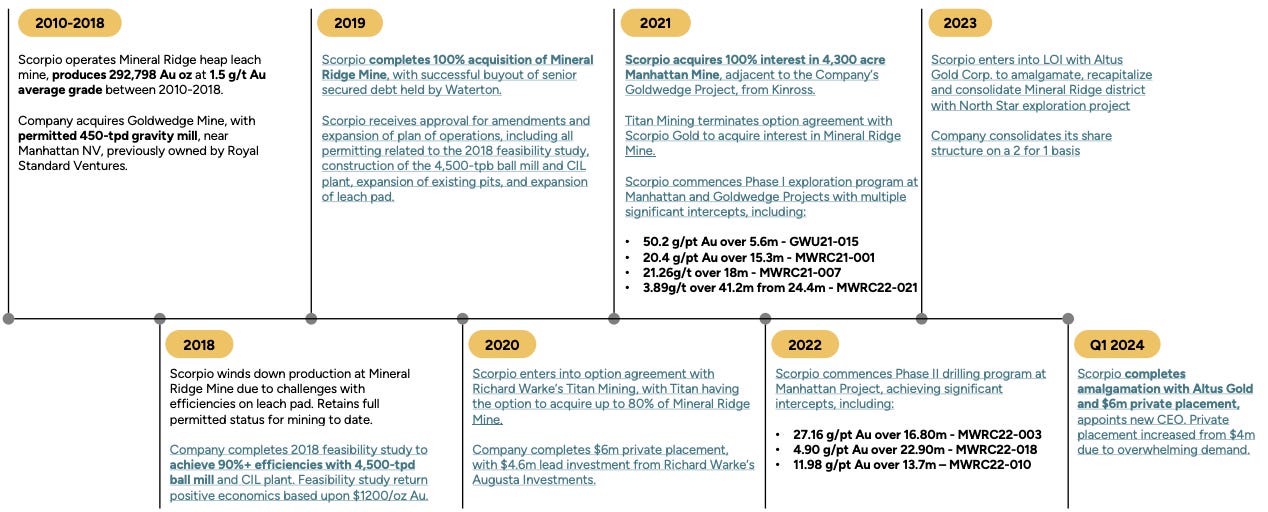

Importantly, management believes there’s potential for the Goldwedge, Echo Bay West, Echo Bay East, and the Caldera Splay zone to be connected in a single large deposit {see map below}. On August 1st, the Company announced that it had completed its Phase 1 drill campaign [five holes / 1,178 m] at Manhattan.

Is Goldwedge tied to Echo Bay West? Is it also tied to Echo Bay East?

(Click on image to enlarge)

Phase 2, starting right away, is anticipated to be ~13 holes / 3,109 m. VP of Exploration Harrison Pokrandt commented,

“Phases 1 & 2 were planned in close coordination with our advisory team led by Daniel Kunz of Daniel Kunz & Associates (“DKA“), with the dual purpose of being follow-ups to historic drilling, alongside moderate step-outs of known structures to connect multiple zones of mineralization, particularly the Goldwedge underground & Manhattan West Pit,”

This year’s drilling aims to extend known mineralization along strike into untested areas. Drilling will provide data for preliminary metallurgical testing, confirm previously drilled intervals, and expand the understanding of mineralized structures.

New drill data will aid in the planning & execution of a claim-wide structural mapping campaign in September.

Scorpio also holds a 100% interest in the Mineral Ridge project, a past producer [operated by Scorpio] in the 2010s. The 5,617-hectare MR property is equidistant between Reno & Las Vegas, NV along the California border.

Before Scorpio’s acquisition in March 2010, MR produced ~575,000 ounces from both open pit & underground operations. While readers are familiar with mine restart stories, rarely is the operation being rehabilitated one that the existing company ran in the past.

Who better to restart a mine than the company that last mined it? Who knows the geology, geochemistry, nearby communities, and mining conditions as well?

MR is a conventional, low-risk, low-cap-ex, open-pit heap leach operation. Looking back to the 4-yr. period 2014-2017 when annual revenue averaged ~C$74M (at the current C$/US$ exch. rate), the Company was not generating much, if any, positive cash flow.

(Click on image to enlarge)

However, it’s no mystery why that was the case, Au averaged just $1,234/oz. during that time. While operating costs are certainly up since then, today’s price of $2,412/oz. is +95%! If in 2017 the AISC was ~$1,150-$1,200/oz., call it $1,175/oz., that cost [might be] +40% now to $1,645/oz.

This suggests the operating margin could soar from just $59/oz. to $767/oz.!! Therefore, as long as MR can be reopened at a reasonable upfront cap-ex, Scorpio should be quite profitable. For example, at 30,000 oz./yr., Au @ $2,412/oz., and all-in costs of $1,645/oz., operating income would be ~C$31.5M.

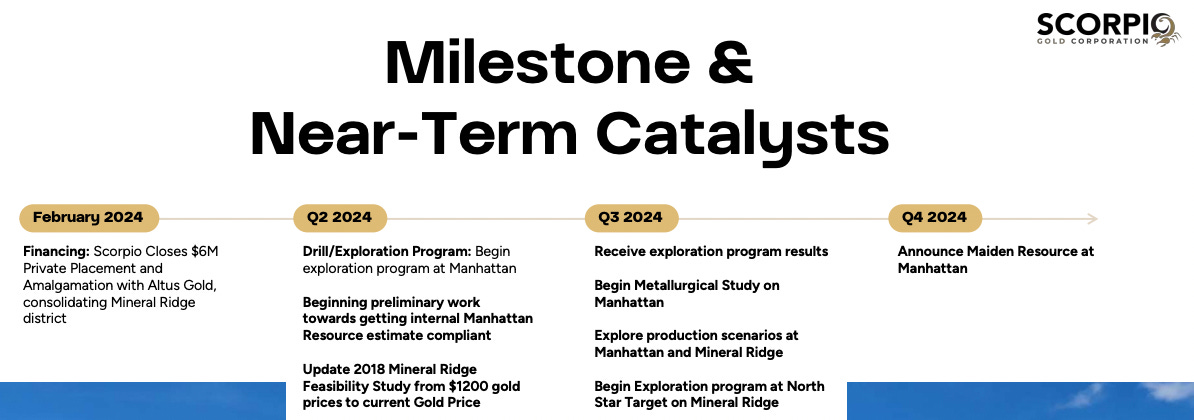

CEO Zayn Kalyan’s team believes that funding cap-ex at MR could be (mostly) done on a non-equity dilutive basis. Since MR is fully permitted, it could be back in production in 1H/25. A 2018 Feasibility Study on a 7.5-year heap leach restart showed an after-tax NPV of ~C$49M but that was based on US$1,250/oz. Au.

At $2,400/oz., the NPV quadruples to ~C$200M before adjusting for *call it* +40% higher op-ex & cap-ex, knocking the pro forma NPV down to ~C$150M. That’s a strong 100%-owned NPV vs. Scorpio’s valuation of ~C$20M.

(Click on image to enlarge)

With a proven & probable reserve, valuable permits, water rights, infrastructure, and an option to acquire a 90% interest in the adjacent Northstar property, MR has very significant near-term development potential. Northstar has high-grade mineralization with surface channel & grab samples

of up to 36.9 g/t Au.

Management believes that Northstar could host the feeder system that fed gold into MR. In addition to high grade, the new property could have better metallurgy. Discoveries on MR and/or Northstar would leverage Scorpio’s valuable mine infrastructure, water rights & permiting status.

Scorpio’s plans are backed by a stellar mgmt. team, board & advisors, especially for a company of this size.

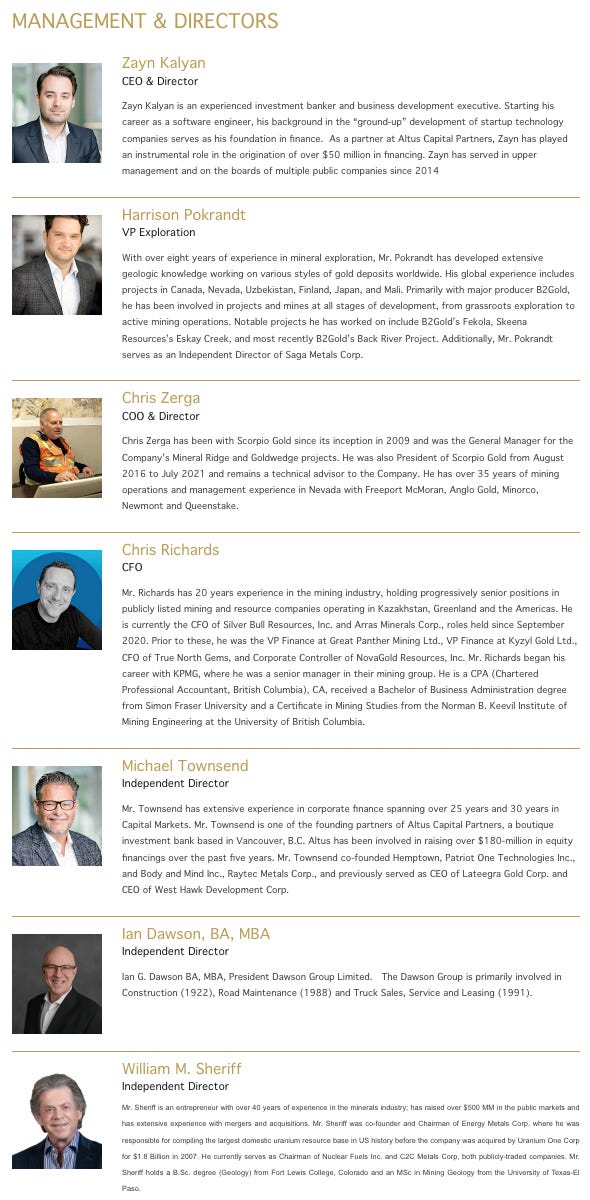

CEO/Dir. Zayn Kalyan is an experienced investment banker & business development exec. As a partner at Altus Capital Partners, Zayn has played an instrumental role in the origination of > $50M in financing. Zayn has served in upper management and on the boards of multiple public companies since 2014.

COO/Dir. Chris Zerga has been with Scorpio since its inception in 2009 and was general manager of the Mineral Ridge & Goldwedge projects. He was President from Aug. 2016 to July 2021 and remains a technical advisor. He has > 35 years’ experience in Nevada with Freeport McMoran, Anglo Gold, Minorco, Newmont & Queenstake.

VP Exploration Harrison Pokrandt has worked on numerous styles of gold deposits worldwide, in Canada, the U.S., Uzbekistan, Finland, Japan & Mali –> primarily with B2Gold Corp., where he was involved in all stages of development. Notable projects include; B2Gold’s Fekola, Skeena Resources’ Eskay Creek, and B2Gold’s Back River.

Independent Dir. Bill Sheriff, has an MSc in mining geology & 40+ years’ experience, incl. decades working on Au projects in Nevada, the western U.S. & Canada. Mr. Shefiff is a leading uranium expert in the U.S., most notably as executive chairman of EnCore Energy. He excels in capital markets and has a proven track record in M&A.

The establishment of Scorpio’s advisory panel is a new strategic initiative to add considerable bench strength to the Company’s growing team. Management is engaged in discussions with several highly qualified candidates with proven track records in technical & capital market domains.

(Click on image to enlarge)

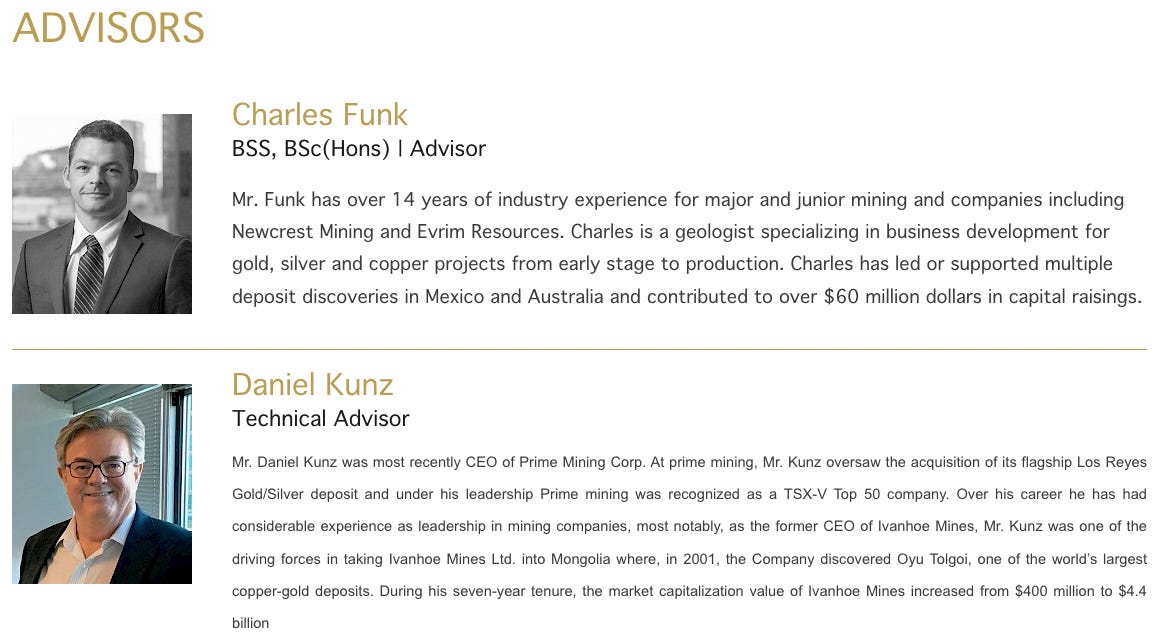

Technical advisor Daniel Kunz was most recently CEO of Prime Mining Corp. where he oversaw the acquisition of its flagship Los Reyes Au/Ag deposit. He was CEO of Ivanhoe Mines when, in 2001, he was a key person in the discovery of one of the world’s largest copper-gold deposits.

Tech. advisor Charles Funk, BSS, BSc (Hons) has > 14 years’ experience with companies incl. Newcrest (now Newmont) & Evrim Resources. As a seasoned geo, he specializes in business development for Au, Ag & Cu projects and has led or supported multiple discoveries in Mexico & Australia. Mr. Funk is CEO/Dir. of Heliostar Metals.

(Click on image to enlarge)

Scorpio Gold (TSX-v: SGN) / (OTCQB: SRCRF) is well positioned with near-term production potential (next year) from a low-risk, low-cap-ex, heap leach project in Nevada. It also has tremendous exploration upside on its two main assets + associated targets. A great team is driving the Company forward.

If the Au price were < $2,000/oz., the Scorpio narrative would be far less compelling, but Au > $2,400/oz. is within 3% of an all-time high. Many investment banks are calling for Au prices of $2,500-$3,000/oz. in 2025. Those in production sooner rather than later will be worth their weight in gold!

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Scorpio Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Scorpio Gold are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Scorpio Gold was an advertiser on [ER] and Peter Epstein owned no shares in the company.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

More By This Author:

Are Tesla Moonshots Priced Into Its Share Price?

Frontier Lithium: Down, Down, Down — But Not Out

Is Standard Lithium The Next Producer In The U.S.?

Comments

Log in or sign up to join the conversation.