Photo by Delfino Barboza on Unsplash

As the world braces for a seemingly inevitable recession, commodities have taken a hit. The prices of oil, copper and iron ore are all sharply down from their peaks earlier this year. That’s not surprising, as demand for raw materials tends to move up and down with economic activity. But another factor is the capital cycle: the amount of investment entering or exiting an industry. Given the severe lack of money that has flowed into conventional energy and raw materials in recent years, it’s possible that commodities will deliver positive returns even as the economy contracts.

Despite the energy crisis triggered by Russia’s invasion of Ukraine, many investors fear that demand for hydrocarbons will vaporise over the coming years. Oil giant BP says that if governments are to realise their pledges to reduce net carbon emissions to zero by 2050, the share of fossil fuels in final energy consumption must fall to 20%, from the current level of around 65%. The prospect of such a dramatic decline makes energy companies reluctant to invest in big-ticket projects with multi-decade payoffs.

Canadian scientist Vaclav Smil, author of “How the World Really Works”, dismisses the notion that the globe is on the verge of giving up fossil fuels. Hydrocarbons aren’t just used for transport and heating but are an essential input in the production of what he calls the “four pillars of civilisation”: steel, concrete, plastics and ammonia (for fertiliser). It’s unlikely, says Smil, that these industries will eliminate their dependence on fossil fuels in the decades to come, especially in low-income countries with enormous infrastructure needs. “We still do not know most of the particulars of this coming transition,” he writes, “but one thing is certain: it will not be (it cannot be) a sudden abandonment of fossil carbon, nor even its rapid demise – but rather its gradual demise.”

Adam Rozencwajg, managing partner at natural resources investment firm Goehring and Rozencwajg, points out that renewable energy has huge upfront costs, consuming large amounts of conventional energy and raw materials. The construction and installation of a 1.5-megawatt GE wind turbine, he says, uses 190 tonnes of steel, 600 tonnes of concrete and 9 tonnes of copper. It takes several years for renewable sources of power such as wind and solar to pay back the energy used in their construction. Thus the transition to green power will, in the medium term, boost demand for hydrocarbons.

Investors don’t need to spend too much time obsessing about future demand, though. The capital cycle approach recommends they direct their attention instead to current supply. Here the picture is much clearer. Capital spending by energy firms and miners has declined since the investment boom peaked in the middle of the last decade.

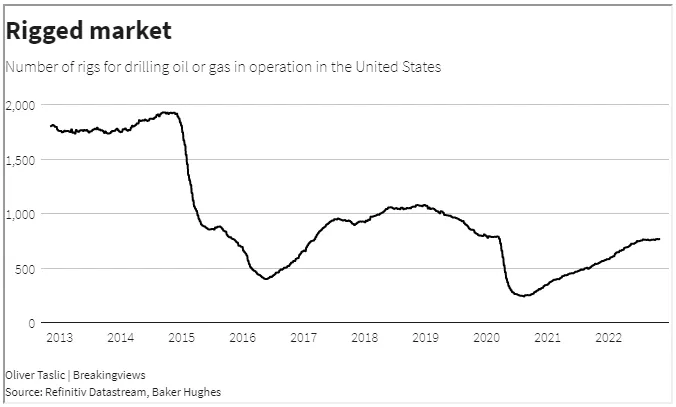

Output from conventional oil production hasn’t increased since Lehman Brothers collapsed in 2008. Instead, the incremental growth in demand for the black stuff has been mostly met by increased output of U.S. shale oil. But shale resources run dry much more rapidly than conventional oil fields and their output is not being replaced. The number of active oil rigs in the United States is just 40% of its 2014 peak. Over the last year, rising oil demand has been met from American wells drilled before the pandemic and by tapping into the U.S. government’s Strategic Petroleum Reserve. Both these sources of extra supply are nearly exhausted.

Spending by oil majors on finding and drilling new wells has picked up over the last year. But it’s way down on historic levels. Capital spending by large European oil companies has fallen from more than twice depreciation in the mid-2010s to less than one times, according to Bernstein. In 2013, U.S. giant Chevron’s capital expenditure was $38 billion. Last year it was $8 billion.

Even if oil companies overcome their aversion to new investment, a severe shortage of equipment and labour means the supply situation won’t improve any time soon. Halliburton, the giant oil services company, has reduced its spending on property, plant and equipment by two-thirds since 2013. Nor will exploration of new oil fields in deep water pick up any time soon. After suffering massive losses, the U.S. offshore rig industry has consolidated, causing a reduction in the number of available “floaters” – platforms that do not rest on the ocean floor.

A similar picture emerges in the mining industry, whose capital spending boom also ended around eight years ago. My former colleague Lucas White, who runs the investment firm GMO’s resources strategy, calculates that capital expenditure by commodity producers is down 65% in real terms since 2014. Given the 10-year lead time for new mines, underinvestment will restrain supply for at least the next decade.

Copper is one of the key materials required for weaning the world off hydrocarbons. It’s used in electric vehicles, renewable energy production, and electricity grids. According to S&P Global, the energy transition could double demand for copper by 2035. That implies annual supply will have to grow by 5% a year, roughly double the rate between 2000 and 2020. Yet current supply is hardly sufficient to meet current demand. And once again, mining firms aren’t investing enough. Freeport-McMoRan, one of the world’s largest copper producers, cut capital spending from $7.2 billion in 2014 to $2.1 billion last year.

Commodity prices collapsed at the start of the 2008 recession. But Rozencwajg argues the energy and mining sectors are better placed today. Their situation is more comparable to the late 1920s, an era when commodity investment was curtailed as capital flowed into new technologies like electricity, automobiles and radio. Having been starved of cash, oil and mining stocks delivered positive returns between 1929 and 1937, while the U.S. stock market was cut in half. Even if the global economy were to collapse once again, the capital cycle could allow commodities producers to deliver positive returns.

More By This Author:

U.S. Weekly FundFlows Insight Report: During the Midterm Election Week Bond ETFs Attract A Net $3.7 BillionTSX Earnings Scorecard 22Q3 - Thursday, Nov. 10

Seeking Safety

Comments

Log in or sign up to join the conversation.