Image Source: Pixabay

As the recession narrative dissipates, what’s left to uplift the gold price? Will fundamentals continue to unfold as expected?

While the recession crowd amplified rate-cut hysteria and helped propel the yellow metal higher, we warned on Apr. 6 that the Fed’s tightening cycle was far from over. We wrote:

With relatively weak PMIs and a deceleration in JOLTS job openings garnering all of the attention this week, the recession crowd has bid bonds and the anxiety has helped uplift the PMs. Moreover, with fears of a banking crisis helping to increase their safe-haven appeal, gold, silver and mining stocks have outperformed.

Yet, we’ve seen this movie before and the permabulls are often the loudest near the top. Furthermore, since the fundamentals contrast the narrative – like they did during the countertrend rallies in 2021 and 2022 – another sharp reversal should be on the horizon.

To that point, with solid economic data shifting the narrative, the fundamentals continue to unfold as expected. For example, U.S. nonfarm payrolls came in at 339,000 versus 180,000 expected on Jun. 2, which highlights how labor demand remains abundant.

Please see below:

More importantly, the payrolls outperformance weighed on the gold price, as we’ve warned repeatedly that a resilient U.S. economy is bearish for the PMs.

Please see below:

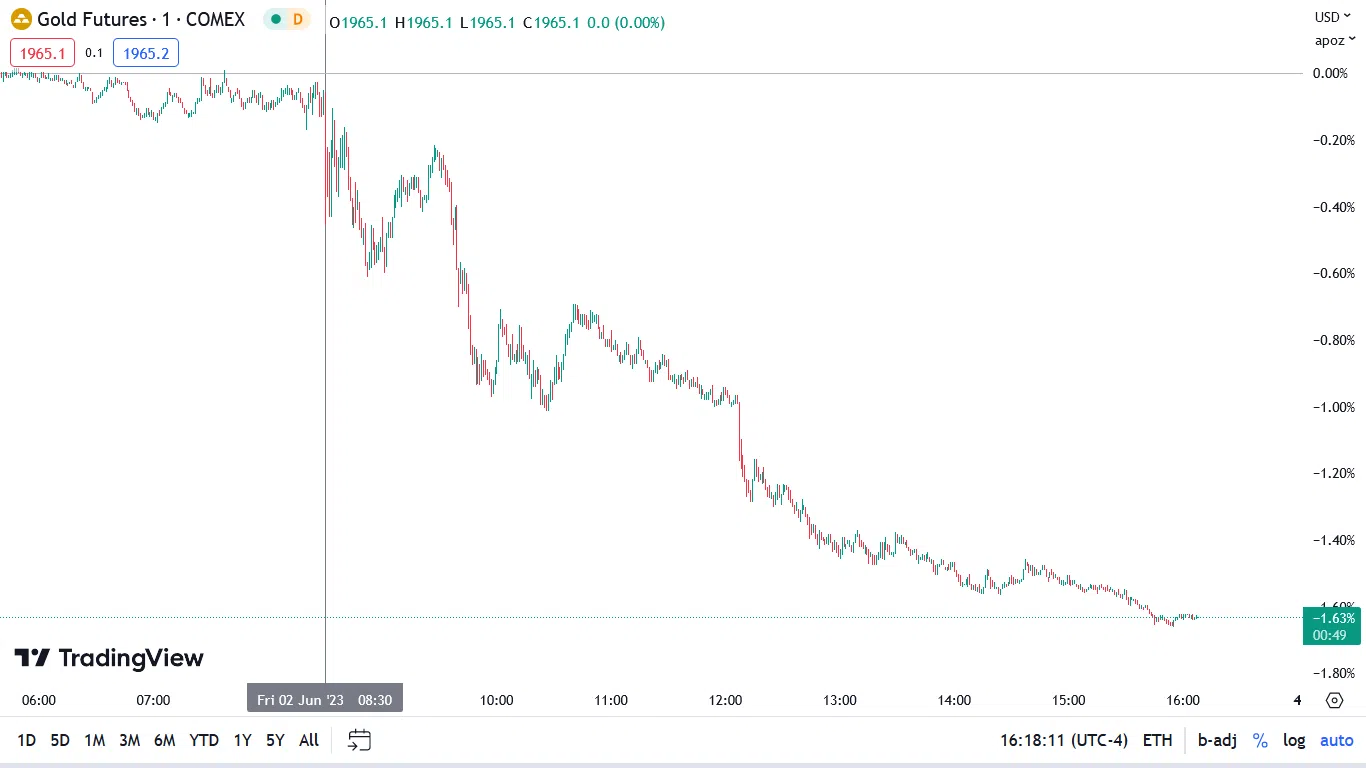

(Click on image to enlarge)

To explain, the candlesticks above track the gold futures price. If you analyze the vertical gray line, you can see that after the payrolls print hit the wire at 8:30 a.m. ET, it was all downhill for the yellow metal. As such, while the medium-term technicals and fundamentals have been aligned for some time, the pair have begun to showcase their might.

The Inflation Puzzle

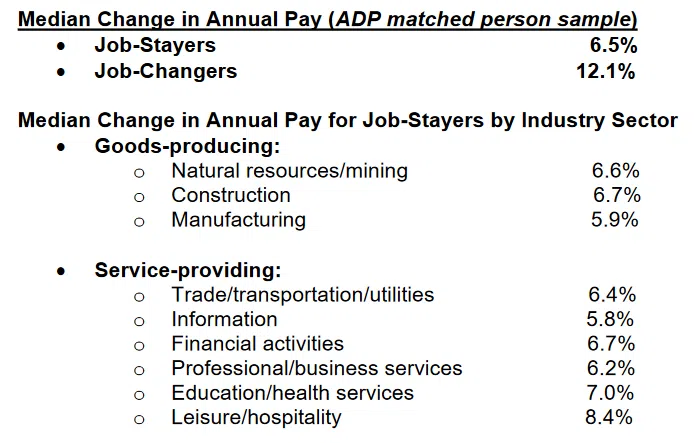

While U.S. average hourly earnings met expectations at 4.3% year-over-year (YoY), ADP’s private payrolls highlight sticky wage growth (data released on Jun. 1).

Please see below:

To explain, the median change in annual pay for job-stayers and job-switchers hit 6.5% and 12.1% in May. In addition, all of the industries tracked by ADP are experiencing wage inflation of ~6% or more.

Therefore, while base effects have reduced output inflation, those benefits run out after June. And while recession fears weighed on economically-sensitive commodities, which also helps reduce headline inflation, the S&P GSCI (commodity index) has rallied materially in June. So, unless the Fed engineers a real recession, the inflation merry-go-round should continue.

Speaking of which, BlackRock CEO Larry Fink said on May 31 that “The Fed is not finished. Inflation is still too strong, too sticky.” And with the metric poised to stay in the 4% to 5% range “for some time,” he added, “I just don’t see the evidence around a reduction in inflation.”

Please see below:

On top of that, while the crowd assumes that inflation is old news, we have warned for many months that the fundamentals contrast investors’ optimism and the gold enthusiast’s medium-term bull thesis. And with Gallup’s May 18 poll supporting our argument, the Fed’s inflation problem can’t be wished away. The report stated:

“A separate Gallup poll, conducted by telephone April 3-25, finds inflation is by far the top trouble mentioned when Americans are asked to name the most important financial problem facing their family. The cost of owning or renting a home (11%) ranks a distant second to inflation, while having too much debt (9%) and a lack of money or low wages (7%) follow close behind.”

Please see below:

(Click on image to enlarge)

To explain, the vertical green bar at the top shows how 35% of Americans cited inflation as their most pressing problem. Thus, the prospect of the Fed cutting interest rates to exacerbate this problem was, and still is, foolish.

Likewise, the green bars at the bottom show how Americans remain unconcerned about job losses and interest rates. Therefore, it further confirms our belief that interest rates are too low to create the demand destruction necessary to eradicate inflation.

In reality, reducing inflation requires interest rates and job losses to rise to restrict consumption and economic growth. And if this were the case, more Americans would be worried about higher financing costs and prospective unemployment. So, the unfortunate truth is that for the top green bar to decrease, the bottom green bars need to increase.

Finally, Bank of America’s President of Retail Banking Holly O'Neill reiterated our long-standing argument on May 31. She said:

“The consumer is still very healthy. Savings and account balances are still well above where they were pre-pandemic.”

As a result, data from the second-largest U.S. bank says that investors are still too optimistic about rate cuts and QE over the next several months.

Overall, the Fed’s tightening cycle is incomplete, which means that real interest rates and the USD Index should continue to rise over the medium term. And since gold, silver and mining stocks often move opposite to these metrics, they should suffer as the drama unfolds. Consequently, we expect more downside before long-term buying opportunities emerge.

Why do U.S. nonfarm payrolls keep outperforming expectations?

More By This Author:

Silver’s Swoon Should Resume

What to Make Of Silver’s Sorry Performance

Silver’s Slide Was Far From A Surprise

Comments

Log in or sign up to join the conversation.