Goldilocks Or Dorothy?

Many of us have used Goldilocks as a metaphor for desirable economic conditions. Not too hot, not too cold, just right. We’ve also taken to calling Federal Reserve Chairman Powell as “Goldilocks in a suit” on multiple occasions for his tendency to soften his messages during post-FOMC press conferences. It’s a bit odd to consider that a naïve young girl is the metaphor preferred by a cadre of macho traders.

Yet I wonder if a simple country girl from Kansas might be the more appropriate market metaphor these days. Why? “The Wizard of Oz”, the movie gets a happy ending when Dorothy simply clicks her heels together and repeats the phrase “there’s no place like home” until she magically returns to her farm.1 I get the sense that investors are hoping for a similar outcome. If enough of us click our heels together and repeat “soft landing, soft landing, soft landing…”, will one magically appear?

As we recently noted, Fed Funds expectations had a major reset last week. Fed Funds futures went from a modest chance for an additional (final) hike to zero. They also placed higher probabilities for additional, accelerated cuts in the coming months. A cut is not considered likely by May and certain by June. A second cut in July is considered a near-certainty. These changing expectations have encouraged both equity and fixed income investors, and prices have rallied sharply in both markets.

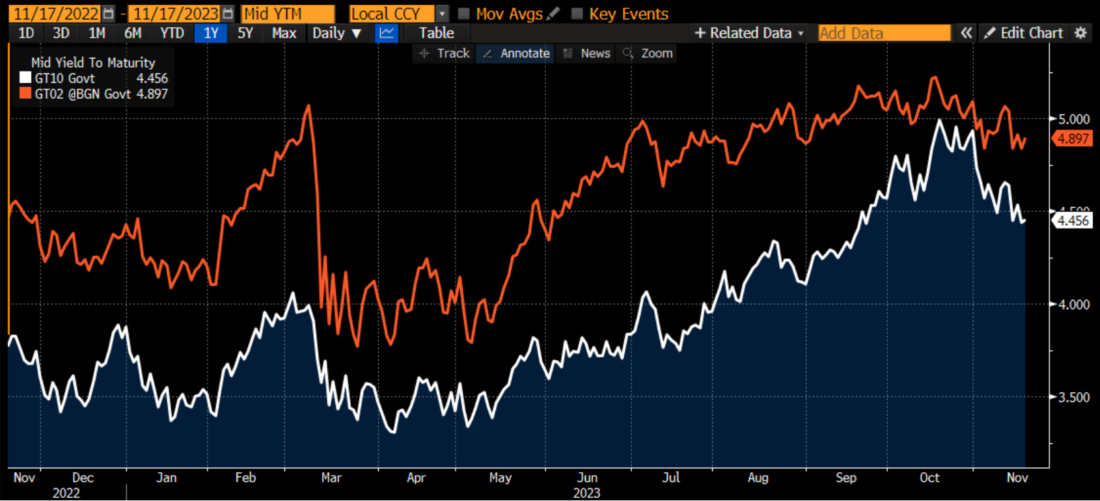

The drops in yields have indeed been quite dramatic. Since their recent peak in mid-October, 2-year Treasury yields have dropped from 5.22% to 4.89%. That essentially reflects the elimination of an additional 25-basis point hike. Meanwhile, 10-year yields have plunged from 4.99% to 4.45%. There is much more to that move than 25bp here and there. It incorporates some resetting of inflationary expectations over the coming years while still exhibiting some consideration for a decent economy.2 Yet when viewed over a longer period of time, these moves fit well within the context of the prior year. The 2-years are still near their highs over that period, while the 10-year yield is still well above levels from just before the summer:

(Click on image to enlarge)

1 Year Line Chart, 2-Year (red) and 10-Year (white) Yields Source: Bloomberg

At the beginning of 2022, we questioned whether the famed pilot “Sully” Sullenberger was in fact the better analog for Chair Powell than Goldilocks. We wrote:

…it occurred to me that investors have decided that Jerome Powell is a financial version of Captain Chesley Sullenberger. For those who have forgotten the reference, “Sully” became famous for guiding a stricken airplane to a safe landing in the Hudson River. Faced with a set of unexpected, incredibly difficult circumstances – in his case, a commercial airliner with both engines disabled by bird strikes shortly after takeoff – he used his knowledge and training to ultimately bring the plane under his command to a safe landing.

Here’s the problem with that analogy: we have no idea if Mr. Powell will be able to land the market without incident this time around. While it is clear that investors are enamored with the Fed’s response to the Covid crisis in early 2020, the current situation is quite different.

Sullenberger was famous for his skillful landing under essentially impossible circumstances. But it wasn’t a soft landing.

The situation is quite different now than it was in 2022. We didn’t know it at the time, but the S&P 500 (SPX) peaked just a week prior at a level we have yet to recoup. Rates had begun to rise but were nowhere close to where they are now. The 2-year had nearly doubled in about 2 months, but from only 0.5% to 0.89%, while the 10-year had moved about 20bp higher over that span to 1.75%. It’s hard to imagine rates returning to that level – barring a catastrophe – yet SPX is only about 6% below its January 2022 peak. Equity markets – or at least the mega-cap tech stocks that dominate the major indices – have largely adjusted to the higher rate environment and the anticipation that rates are likely to dip from here on out.

We also need to reconcile the fact that some key commodities could be hinting at something other than a soft landing. Crude oil prices have plunged recently, though only back to levels that have prevailed for much of this year, while copper is near its lows:

(Click on image to enlarge)

Crude Oil, Rolling Front Month Contract, 1-Year Daily Candles Source: Interactive Brokers

(Click on image to enlarge)

Copper, Rolling Front Month Contract, 1-Year Daily Candles Source: Interactive Brokers

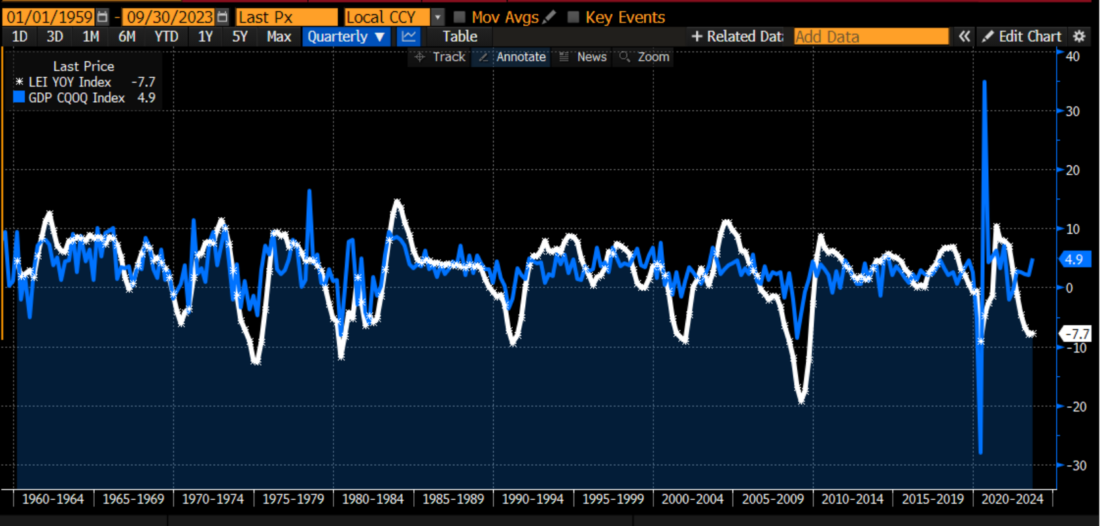

Meanwhile, a long-term chart of Leading Economic Indicators (LEI) shows us near historic cyclical lows, even as recent Gross Domestic Product prints don’t confirm the recent dip:

(Click on image to enlarge)

Leading Economic Indicators (white) and Gross Domestic Product (blue) since 1959 Source: Bloomberg

The data leads me to think that rather than some fictional girls, the correct market persona is an experience proven pilot. He undoubtedly has engineered many soft landings during his career, yet he is most famous for a difficult, but ultimately successful under incredibly difficult circumstances. I’d much prefer to put my faith in someone like that than a mythical figure.

(And perhaps the best analog would be a very capable, highly successful young woman who doubles as a business mogul when she’s not performing. But as I noted in an article yesterday, I need to leave Taylor Swift out my reports. It would be “lame” to do otherwise.)

1 Never mind that she prefers sepia-toned, black-and-white Kansas to the technicolor Oz.

2 Or concerns about US indebtedness…

More By This Author:

Turning A Market Adage Upside Down

Playing Musical Chairs With Bankrupt Shares

Is A Potential Pause An “All Clear” For Investors?

Disclosure: FUTURES TRADING

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC ...

more