Gold Thrives In Rate-Hike Cycles

Gold-futures speculators’ most-feared hobgoblin is Fed-rate-hike cycles. These super-leveraged traders wielding outsized influence on gold prices flee in terror when rate hikes loom. The resulting heavy selling hammers gold sharply lower, damaging sentiment. But these myopic speculators apparently have no history books, as gold actually thrives during Fed-rate-hike cycles! They’ve proven very bullish for this asset.

In mid-June 2021, the Federal Reserve’s Federal Open Market Committee responsible for setting this central bank’s monetary policy met in one of its eight scheduled meetings per year. The FOMC didn’t even hint at rate hikes, but every other meeting is accompanied by a Summary of Economic Projections of individual top Fed officials. Their future federal-funds-rate expectations are detailed in its so-called dot plot.

Fully 2.5 years after the last FFR hike, just a third of those Fed decision-makers were looking for maybe two quarter-point hikes way out into year-end 2023. Despite that being an eternity away in market time, gold-futures speculators panicked. Their extreme long-contract dumping crushed gold 5.2% lower over three days, spawning serious bearish psychology! These guys assume Fed rate hikes are bad news for gold.

Then in early August after better-than-expected monthly US jobs report upped Fed-rate-hike odds, the same gold-futures speculators responded with epic short selling. That slammed gold down another 4.1% in just two trading days! Later in mid-September a big upside surprise in monthly US retail sales also pressuring the Fed to start hiking shook lose more heavy gold-futures selling, forcing gold 2.2% lower that day.

The examples are legion of these excitable traders puking out huge bouts of leveraged selling battering gold on Fed-rate-hike fears. That even seems logical on the surface. Gold yields nothing, so higher rates pushing up yields on competing US-dollar-denominated bonds should leave the yellow metal looking less attractive right? The problem is hard facts slaughter this flawed thesis, gold thrives during Fed-rate-hike cycles.

The same irrational paranoia from gold-futures speculators plagued gold in late 2015 heading into the Fed’s maiden hike of its last cycle in mid-December that year. So leading into that I decided to crunch the historical data to see if those worries were righteous. They weren’t. I updated that research thread again in late March 2017. Now we’re staring down the loaded barrels of another imminent Fed-rate-hike cycle.

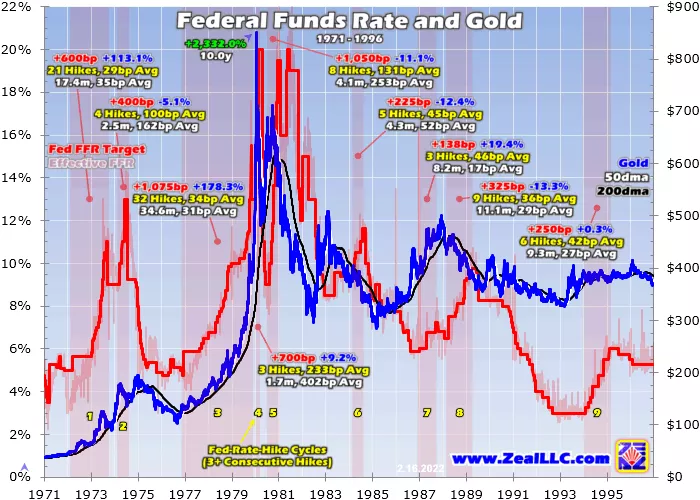

The modern era of monetary policy began in 1971 when the US dollar went fully fiat being completely severed from the gold standard. So this past half-century, the 51.2 years since that fateful pivot year commenced, are the extensive study period. This research is somewhat challenging, as the further back in time the more sketchy historical data gets. The Fed maintains extensive but often-changing datasets.

Getting gold prices is easy, but finding the exact days where the FOMC changed its federal-funds-rate target in regular or emergency meetings decades ago is problematic. In earlier iterations of this research I used New York Fed documents detailing FFR changes and dates. But in the five years since that last update, the St. Louis Fed has published a far-more-thorough and seemingly better daily record of FFR targets.

So I switched over to that dataset, integrated it into our spreadsheets, and re-ran all this analysis from scratch. The result was claimed dates of a handful of FOMC meetings either starting or ending hiking cycles way back in the 1970s and 1980s changed by a few weeks or so. That affected their durations, thus gold’s price performances over those particular spans. The ultimate impact on this research was immaterial.

But it did slightly change gold’s average gains and losses during Fed-rate-hike cycles compared to my March-2017 update. The definition of a Fed-rate-hike cycle remains the same, three-or-more consecutive federal-funds-rate-target increases by the FOMC with no interrupting decreases. It’s hard to argue that a lone hike or even two isolated hikes bracketed by cuts makes a cycle. The Fed has occasionally done both.

Since 1971, the FOMC hiked once before cutting six times. It boosted the FFR twice in a row before reversing those rate hikes another half-dozen times. But there have been fully twelve real Fed-rate-hike cycles comprised of three-or-more uninterrupted FFR increases over that long span. That encompassed all possible gold environments, bulls and bears, rampant herd greed and fear, and the whole gamut of inflation.

So if gold-futures speculators are right that Fed rate hikes are a dire bearish threat to gold, the past dozen Fed-rate-hike cycles would prove that out. But these traders are dead-wrong, blinded by myopia from the super-short time horizons their extreme leverage requires for survival. Despite being derided as a sterile asset because of its lack of yield, the FOMC raising its federal-funds rate has proven very bullish for gold!

These charts reveal that heretical truth. They superimpose daily gold prices over both the FOMC’s actual federal-funds-rate target and the daily effective FFR since 1971. This market FFR fluctuates around that target, requiring the Federal Reserve to actively manipulate interest rates through open-market buying and selling of bonds to force rates in line. Modern computerized markets have made that much easier.

Each Fed-rate-hike cycle is highlighted, with key stats noted. They include total federal-funds-rate hikes in basis points, gold’s exact gains between its close the day before each cycle’s first hike to the day of its final hike, how many hikes in each cycle and each cycle’s duration in months between its maiden and terminal hike. Average FFR hikes within cycles are also noted, across both their total increases and durations.

Since a half-century of all this data wouldn’t fit legibly in one chart, it is spread out across two. Frightened gold-futures speculators should stop reading here, lest this heterodox historical record shatters your false worldview. For everyone else capable of handling the truth, gold and thus gold-stock portfolio allocations should be greatly upped when the Fed is threatening and executing hikes. Gold thrives during Fed-rate-hike cycles!

Gold-futures speculators use extreme leverage that should be illegal to bully gold prices around. Just this week, each contract controlling 100 ounces of gold only required traders maintain cash margins of $6,000 in their accounts. Yet at $1,875 gold each contract is worth $187,500, making for ludicrous maximum leverage of 31.3x! Since 1974 the legal limit in the stock markets has been 2.0x, or 50% margin at most.

Every dollar traded in gold futures can have up to 31x the gold-price impact as a dollar invested outright! That makes these guys effectively rogue traders. They’ve faced huge fines and legal settlements in recent years for truly-illegal manipulative trading including spoofing. That means entering massive gold-futures sell orders, then quickly withdrawing them before they are executed artificially slamming gold lower.

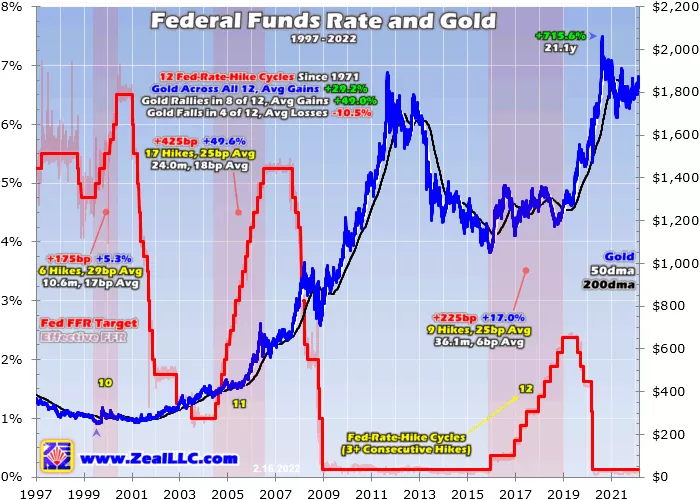

These locusts are a plague on the gold world, stealing from investors for decades. But even gold-futures speculators don’t have to remember far back to realize Fed-rate-hike cycles are bullish for gold. The last one, the twelfth since 1971, ran over 36.1 months from mid-December 2015 to mid-December 2018. That included fully nine hikes for 225 basis points before the Fed caved and capitulated as stock markets plunged.

Gold actually rallied 17.0% during that cycle! Today’s secular gold bull was actually born the day after the Fed’s maiden hike in mid-December 2015 at $1,051. That must be a fluke, right? Surely higher yields are bearish for zero-yielding gold. Before that the Fed’s eleventh rate-hike cycle of this modern era was a monster, running 24.0 months from late June 2004 to late June 2006 with reckless-abandon hiking.

The FOMC hiked fully 17 times for a 425-basis-point total increase to a lofty terminal federal-funds rate of 5.25%. Such levels today sound apocalyptic!If Fed rate hikes were so terrible for gold, it really should’ve suffered in that mega-hiking cycle. Yet this yellow metal actually powered 49.6% higher over that exact span! The gold-futures speculators pulling their Chicken-Little bullshit can’t even remember these last two cycles.

They each averaged 13 hikes for 325bp, far worse than current expectations for maybe eight quarter-point hikes or 200bp for this imminent thirteenth cycle. The federal-funds rate averaged 3.8% as they ended, nearly double the likely 2.0% next time around. Their average duration was 30.1 months, far longer than most see this next cycle lingering. Yet gold still averaged hefty 33.3% gains during their exact spans!

Gold thrived during the past couple decades’ rate-hike cycles, and it will thrive again during the next one. The coming gains will shred the foolish gold-futures speculators who are leveraged-short, betting higher yields will crush gold. Their panicked selling fits will reverse to desperate short-covering buying, which will catapult gold sharply higher. May their losses be huge, which is just for anyone fighting the Fed and history!

Unlike those guys repeatedly freaking out about nothing, prudent contrarian speculators and investors do have history books. Instead of relying on conventional wisdom about markets which often proves wrong, we can consider 51.2 years of historical precedent to see how gold really fares during Fed-rate-hike cycles. That answer is really damned well! Consider this dataset, a dozen Fed-rate-hike cycles over a half-century.

During them, the FOMC hiked a whopping 123 times, for an astounding total of 5,588 basis points! They each averaged 10 hikes for 466bp, with average durations of 13.7 months. If Fed-rate-hike cycles were really bearish for gold, it would have been pummeled through most of these tightenings. Yet the yellow metal averaged truly-outstanding 29.2% absolute gains across all dozen modern hiking cycles’ exact spans!

Any major asset soaring on the order of 30% in just over one year is impressive. Realize the major gold stocks tend to amplify gold’s gains between 2x to 3x, so they can easily power far higher when the FOMC is forcing up its FFR. Drilling down further, gold has actually rallied during eight of these twelve Fed-rate-hike cycles or fully two-thirds. During those including the last four, gold averaged massive 49.0% gains!

But maybe those gullible gold-futures speculators aren’t totally duped, as gold did fall during four of these twelve modern cycles. Provocatively though the last time that happened was way back into early 1989 in the eighth cycle. During those four Fed-rate-hike cycles where gold fell, its average losses weighed in at an asymmetrically-small 10.5%. Even when gold falters a third of the time during Fed hikings, its losses are mild.

Gold’s worst loss during any modern cycle was 13.3% in that eighth one ending in February 1989. But its best gain was a colossal 178.3% during the third one that gave up its ghost in October 1979! Back then gold was skyrocketing parabolic on raging inflation unleashed by extreme Fed money printing. We’re in a similar scary-inflationary backdrop today, with even headline-CPI inflation now soaring by 7.5% year-over-year!

By looking at gold’s two-thirds wins and one-third losses during modern Fed-rate-hike cycles, we can get an idea of what factors influence gold’s performances. This hard historical data revealed two major ones, how aggressive the FOMC’s hiking is and how high gold’s price was entering those cycles. The former is readily apparent when looking at the average pace of Fed rate hikes between gold’s winners and losers.

In those eight Fed-rate-hike cycles where gold rallied, the FOMC hiked an average of 12 times for 449bp over 17.7-month durations. That made for an average monthly FFR hiking rate of 69 basis points. But in the other four cycles where gold fell, there were seven hikes for 500bp on average but compressed into a far-shorter 5.5-month duration. Happening over just one-third the time, that monthly hiking pace soared to 124bp!

So gold fares best during Fed-rate-hike cycles when they are gradual. I’d define that today as no more than one quarter-point FFR hike per regularly-scheduled FOMC meeting, or about once every six weeks. That’s the Fed’s modus operandi now, trying not to ignite serious stock-market selloffs by hiking too fast. During its last couple of rate-hike cycles, the FOMC hiked 26 times but never lifted its FFR target more than 25bp.

Today’s Fed isn’t likely to hike more than 25bp a pop either, despite the recent 50bp-in-March hype that one loose-cannon Fed official spawned. Federal-funds-futures-implied odds for this looming thirteenth cycle’s maiden hike in mid-March were running at 63% for a quarter-point and just 37% for a half-point in the middle of this week. If this FOMC hikes too fast, these QE4-levitated bubble-valued stock markets will collapse.

In addition to a more measured pace of Fed rate hikes being bullish for gold, its own relative levels are also important for its performance during Fed-rate-hike cycles. When gold enters them relatively high by recent standards, really overbought and drenched in popular greed, it is way more likely to suffer a normal healthy correction during them. Gold can’t rally anytime if preceding massive uplegs exhausted buying.

Conversely if gold is relatively-low heading into a new hiking cycle, if sentiment is fairly-bearish or apathy reigns, it is much more likely to rally as the FOMC forces its federal-funds rate higher. If you carefully study these charts to see where gold entered and exited each of these past dozen Fed-rate-hike cycles, this truth is readily-apparent. Heading into this coming thirteenth cycle, gold remains relatively-low which is bullish.

This secular gold bull’s last major upleg to new record highs peaked at $2,062 way back in early August 2020. During most of the 18.4 months since gold has been grinding sideways-to-lower in a giant pennant chart formation. Much of that weakness since mid-June was fueled by gold-futures speculators freaking out about coming Fed rate hikes. After mostly consolidating low for a year-and-a-half, gold is relatively-low.

While gold is now decisively breaking out from that massive bullish continuation pattern over this past week, it is nowhere near overbought and herd sentiment remains fairly bearish. Thus gold is entering the Fed’s looming next cycle well-positioned to surge much higher. Odds are this metal’s rally through these coming hikes will ultimately prove way bigger than average due to exceptionally-bullish conditions today.

That raging inflation unleashed by this FOMC’s insane money printing is a major one. Although the US CPI is intentionally-lowballed for political reasons, that latest print’s huge 7.5%-YoY increase still proved the hottest read since way back in February 1982! Yet gold has really lagged this scary inflation so far, partially because of gold-futures speculators’ inane bouts of heavy selling on their Fed-rate-hike boogeyman.

During the last similar episodes of extreme CPI inflation back in the 1970s, gold prices doubled during the first then later more than quadrupled during the second! So gold prices ought to at least double this time around. Today’s raging inflation isn’t going away either. Since March 2020’s pandemic-lockdown stock panic, this profligate Fed has ballooned its balance sheet a terrifying 113.5% or $4,719b in just 23.5 months!

That effectively more than doubled the US monetary base, unleashing vastly more newly-conjured fiat dollars competing for and bidding up the prices on far-slower-growing goods and services! Hiking rates will do nothing to destroy that epic deluge of quantitative-easing money printing. All that new money will remain in the system until the Fed musters the courage to unwind it with proportionally-huge quantitative tightening.

The more traders feel the pain from monetary inflation and fear it, the more they will flock to gold. Very ominously, the FOMC failed to slay those colossal 1970s inflation super-spikes until it hiked the FFR well above headline-CPI inflation rates! The latest dot plot from mid-December 2021 revealed Fed officials are only contemplating a 2.5% terminal FFR today, which remains crazy-easy in a world with 7.5% CPI inflation.

If the FOMC actually forced rates high enough to overcome inflation, these QE4-levitated stock markets would crash and help spawn a severe recession if not a full-blown depression. The political pressure on the Fed to stop way before that would be overwhelming. The $4.9t of QE4 money printing ballooned the elite S&P 500 companies’ average trailing-twelve-month price-to-earnings ratios up to 30.2x entering February!

Dangerous bubble territory starts at 28x, which is twice the past-century-and-a-half fair value of 14x. So these lofty stock markets could be more than cut in half before returning to normal valuations! There’s no way this hyper-easy FOMC wants to get blamed for that. Actually, the primary reason gold rallies during Fed-rate-hike cycles is they are bearish for US stock markets, threatening and eventually forcing recessions.

Major persistent stock-market weakness helps investors and speculators alike remember gold, which has proven the ultimate portfolio diversifier for many centuries if not millennia. The more the Fed hikes, the more stock markets retreat, the more traders prudently up their portfolio allocations to gold. Given all of this, gold’s outlook during this threatened thirteenth modern Fed-rate-hike cycle is exceedingly-bullish.

With the Fed more than doubling the US money supply, much-higher gold prices are guaranteed. The biggest beneficiaries will be the fundamentally-superior mid-tier and junior gold stocks. They achieve far-better production growth off smaller bases than the majors, and their lower market capitalizations leave them easier to bid higher. The better gold stocks will greatly leverage gold’s gains as the Fed hikes!

The bottom line is gold thrives during Fed-rate-hike cycles. Despite gold-futures speculators’ paranoia, a half-century of market history has proven this in spades. Gold rallied strongly on average during fully two-thirds of all modern hiking cycles. Gold performed best entering them relatively low with the FOMC hiking its federal-funds rate gradually. Both conditions are true today heading into the Fed’s looming thirteenth cycle.

Investors flock back to gold during Fed-rate-hike cycles because they are bearish for stock markets and threaten or trigger economic recessions. Gold is remembered and bought since it tends to power higher on balance as stock markets weaken. Gold’s upside potential in this next hiking cycle is way bigger than normal due to the raging inflation the Fed’s extreme money printing unleashed, driving bubble-valued stocks.

Yes, people don't understand that. Good article.