Image source: Wikipedia

Yesterday the FOMC concluded their September meeting yesterday, leaving rates at their 22-year high. It signaled another rate hike was coming, this side of Christmas. The FOMC also amended its projection for 2024 rates, raising them from 4.6% to 5.1%. Unsurprisingly the US dollar surged whilst gold fell back.

Prior to the FOMC statement gold had made modest gains towards $1,950 an ounce, reaching its highest in two weeks. However, following the statement it has continued to extend losses for a third consecutive day, trading around $1,925. This is to be expected given such a hawkish stance from the FOMC and a clear commitment to extend to at least one more hike this year as well as a new expectation that rates will remain high well into next year.

FOMC Dots Won’t Solve Anything

Interestingly, whilst the statement put out by the Committee was a near-perfect copy of the July statement, the same can’t be said for September’s dot plot.

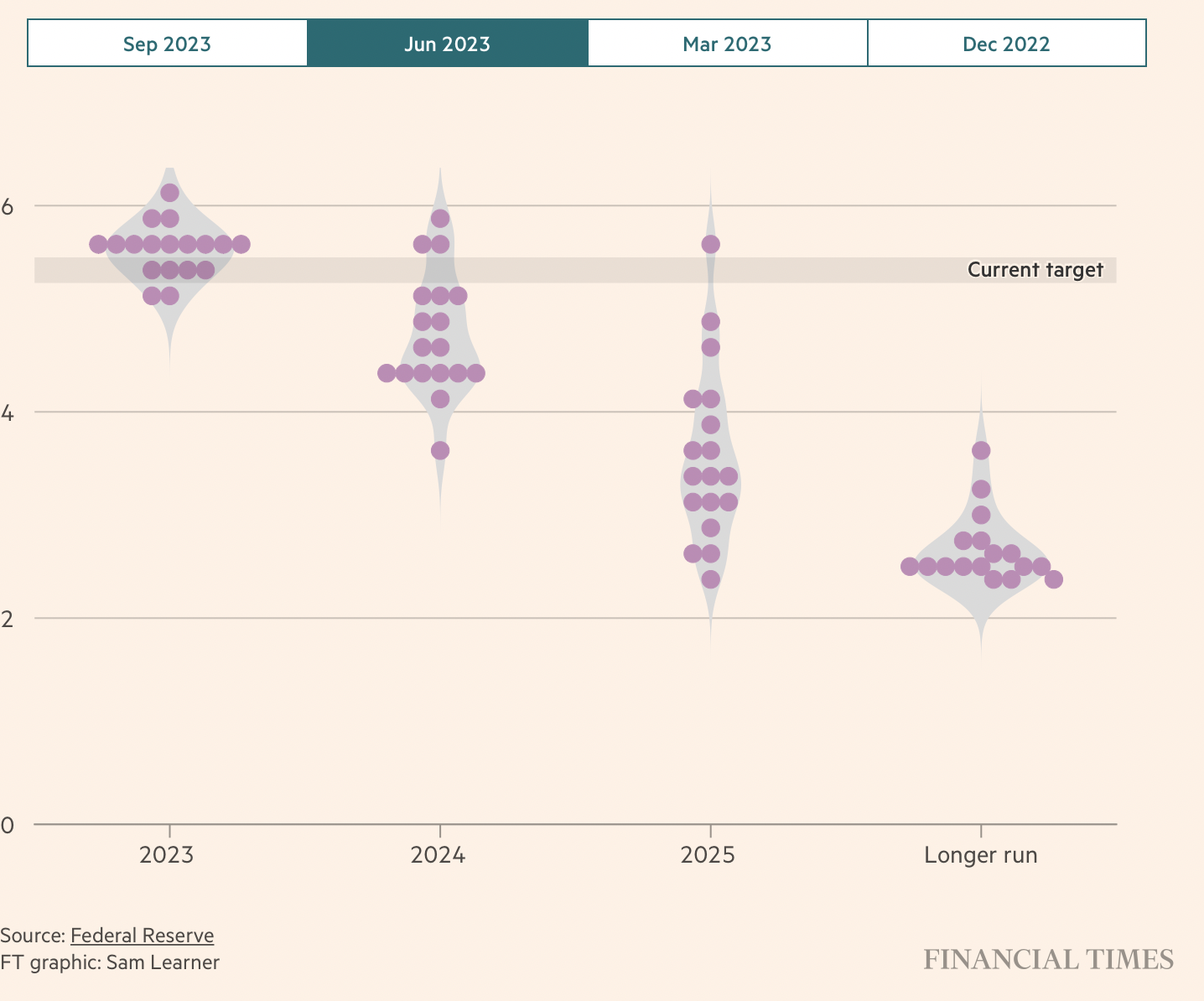

Released quarterly, the FOMC dot plot is a set of projections from committee members based on their view of the economy and monetary policy. They show each FOMC official’s predictions on the federal funds rate. It’s useful to look at as it can help us to identify where trends and biases lie in regard to future rate decisions.

As Bloomberg pointed out, whilst the statement from the FOMC was pretty vanilla, the dot plot was a different story. The difference between June and September’s dot plot is one that shows a hawkish shift.

When you compare the two dot plots from June and September, a hawkish tilt is evident when comparing the 2024 dots to the previous projection. The projection from June’s dot plot with the highest frequency, or mode, was 4.375% (6 dots). In the latest dot plot, it ranges between 4.875% to 5.375%. It’s as much as a 100 bps shift.

This hawkish stance was almost in contradiction to other Fed predictions that suggested a ‘soft landing’ and showed some higher growth forecasts.

Has the Fed Cured Inflation?

The Fed is clearly feeling optimistic about the economy, its statement was pretty dovish in this regard. It sees the economy growing by 2.1% this year (a marked improvement on June’s 1% projection). It also clearly feels confident that high rates are not causing the recession that so many doomsayers declared would happen.

The OECD disagrees. It feels the impact of higher rates is only just starting to be felt. Earlier this week the economic group released its interim economic outlook, in which it downgraded its economic forecasts for next year. Stating that “the impact of tighter monetary policy is becoming increasingly visible — business and consumer confidence have turned down, and the rebound in China has faded”.

But the FOMC is confident that high rates aren’t doing much harm, but is still convinced that it will remain locked in battle with inflation for the next couple of years. Inflation remains stubbornly above its 2% target. The FOMC’s own projections don’t expect it to return to this level until 2026. ..yet it holds a dovish stance when it comes to economic performance.

Overall this was a very confusing day for anyone watching out for what the FOMC was planning. As former PIMCO Chief and economist Mohammed El Erian said:

“I worry that the economic and policy signals coming out of this Federal Reserve press conference may come across to many as both confused and confusing.Some will deem this an inevitable consequence of this phase of the inflation and policy cycle; others will view it as further evidence of challenged Fed communication.”

Of course, all of these reactions by the market, whether the fall in equities, the increase in Treasuries or oil – the fact is trillions of dollars worth of assets were repriced as traders based their actions on some projections that all of us know, will be wrong. And it’s not just the history books that will tell us they were wrong, we’ll know it in a matter of months. Data projections will be revised and new statements will be made.

The truth of it is, it’s obvious that nothing is on the way to being ‘sorted’. Markets are just trading to make cash until the fat lady sings. The FOMC is coming from a country whose debt on September 18th passed the $33 trillion mark. This was $1 trillion higher than just three months before. If you use the Fed’s own projections, blended interest on US debt will be $2 trillion come 2026. This is not sustainable.

This isn’t just about the US

The monetary policy meetings don’t stop in the US. Over in the UK, the Bank of England will be meeting later today. Markets had fully expected the sick man of Europe to hike rates for the 15th consecutive time. However, improved inflation data showed an expected rise to 7% in August (from 6.8% in July) was pessimistic, actual data showed prices fell and inflation was 6.7%.

Prior to the data release, swap markets were predicting an 80% likelihood that the Bank of England’s Monetary Policy Committee would hike rates for the 15th time. Now, the market is split 50-50, with some expecting a hike of 0.25 basis points, and others expecting a long-awaited pause.

For a long time, the UK has been touted as the weak point in Europe. Outcast thanks to its Brexit vote and shoddy leadership issues in recent years. However, markets this week have made it very clear that they are not feeling too favorable about the Eurozone either.

Last week the ECB raised rates to their highest point since the birth of the Euro. Markets were none too impressed or reassured. Theoretically, currencies should perform well when rates are hiked (see the US Dollar) but not in the case of the Euro. Following the announcement, the currency dropped to a three-month low against the dollar. It was a bit like when you ask your kids to stop drawing on the walls but they carry on anyway. It doesn’t fill you with confidence in your authority or ability to keep things under control.

Is anything under control?

The truth of it all is, very little is under control. It’s not just an issue for Christine Lagarde.

Economies’ positions across the globe are simply unsustainable. The Institute of International Finance’s global debt monitor report showed that borrowing as a share of GDP is on the up again, after two years of declines, rising to 336% in June this year. Unsurprisingly, higher interest rates are pushing up borrowing costs and putting governments under serious strain.

A few interest hikes and optimistic statements about the economy are not fixing this. That’s why we’re not concerned about gold’s reaction yesterday, today, or at the next FOMC. Nothing is ‘real’ here. Statements and projections are finger-in-the-air calculations, at best.

And finally…

Some are wondering if the UK got rid of Liz Truss a bit too quickly. At the end of a speech in which she defended her time as the UK’s shortest-lived prime minister she said, that central banks “have played an important role in pumping the system full of money, keeping interest rates artificially low, essentially enabling . . . excessive government spending”. As they say, those who can’t…teach.

More By This Author:

When The Weight Of Inflation Becomes Too Much

Expect $2,500 – $3,000 Gold In The Next 12 Months

Betting On Gold And Global Dominance: How India’s Boom Could Dethrone China

Comments

Log in or sign up to join the conversation.