Image Source: Pixabay

Gold has just hit a new all-time high. Is this an underlying trend or a passing phase? In any case, all the conditions are in place to fuel this ascent. Uncertainty, the spearhead of the yellow metal, is omnipresent in today's major issues. How will the Middle East conflict end? Will the West finally abandon Ukraine? Will China go on the offensive against Taiwan as Xi Jinping calls for greater military preparedness? How will the split between Western and Eastern powers evolve? What will be the outcome of the US elections? How will governments and central banks react to economic and financial tensions?

Back in January, we predicted that gold would reach new record highs. There was no doubt that the period we were already living through, with so many issues at stake, was conducive to a rise in the yellow metal. Although the year is not yet over, gold has already gained 32% (on course for its best year since 1979), while US indices such as the S&P 500 and Nasdaq are up 20% and 30% respectively. This difference will be all the more marked in the long term, as gold's rise is based on structural factors, whereas the performance of US markets depends largely on support from the Federal Reserve.

To understand this year's movement, we need to look back at the key events. Inflation, the traditional driving force behind gold's rise, is at the heart of this dynamic. Often perceived as a simple rise in prices, it is in fact the visible manifestation of a much deeper phenomenon: the devaluation of money. Over time, modern money - i.e., debt money - loses its value through abundant creation. This phenomenon is all the more obvious in the case of the euro, which has lost almost 85% of its value since its creation in the 2000s.

Gold, on the other hand, is by nature immune to this erosion. For in this equation, scarcity is the central element: gold's market capitalization stands at $20 trillion, while world debt today exceeds $315 trillion... Just as you can't print wheat or cotton, you can't print gold, whose quantity is limited, unlike debt. The current period, which is putting an end to decades of cheap money and a world without limits, seems to have highlighted this issue, both ideologically and, of course, financially, which is why institutional and individual investors are so attracted to it. So when inflation accelerates, as has been the case since the health crisis, with abundant liquidity creation and double-digit inflation, the appeal of gold increases. It soars against the major currencies, more than offsetting the impact of rising prices.

This brings us to another crucial point that is often overlooked: that of debt refinancing since the risk of financial tensions has always served as a catalyst for the yellow metal. In this respect, the United States is a major case in point, as the unsustainability of US debt is now becoming a tangible reality. In addition to the fact that US public debt has risen by $500 billion in the last three weeks (or $1,500 per household!), and that its ceiling will be raised once again following the US elections, the US Treasury will have to issue more debt in the coming months than... available demand.

This means that the solution will probably be for the US central bank to monetize the debt, thereby increasing the money supply and further devaluing the US currency. In this respect, the level of refinancing of maturing debt is a fact to be observed everywhere. France, for example, is now paying €50 billion in interest on its debt (or around €800 per French citizen!), but is planning to raise almost €175 billion by 2025, with the sole aim of repaying its debts. On a broader international scale, around 75% of financial market transactions are now dedicated to refinancing existing loans! With an average maturity of seven years, this means that some $50 trillion of global debt needs to be refinanced every year. It's a veritable time bomb, and more than ever, it bears out our analysis that central banks are in a dilemma between monetary and financial crises.

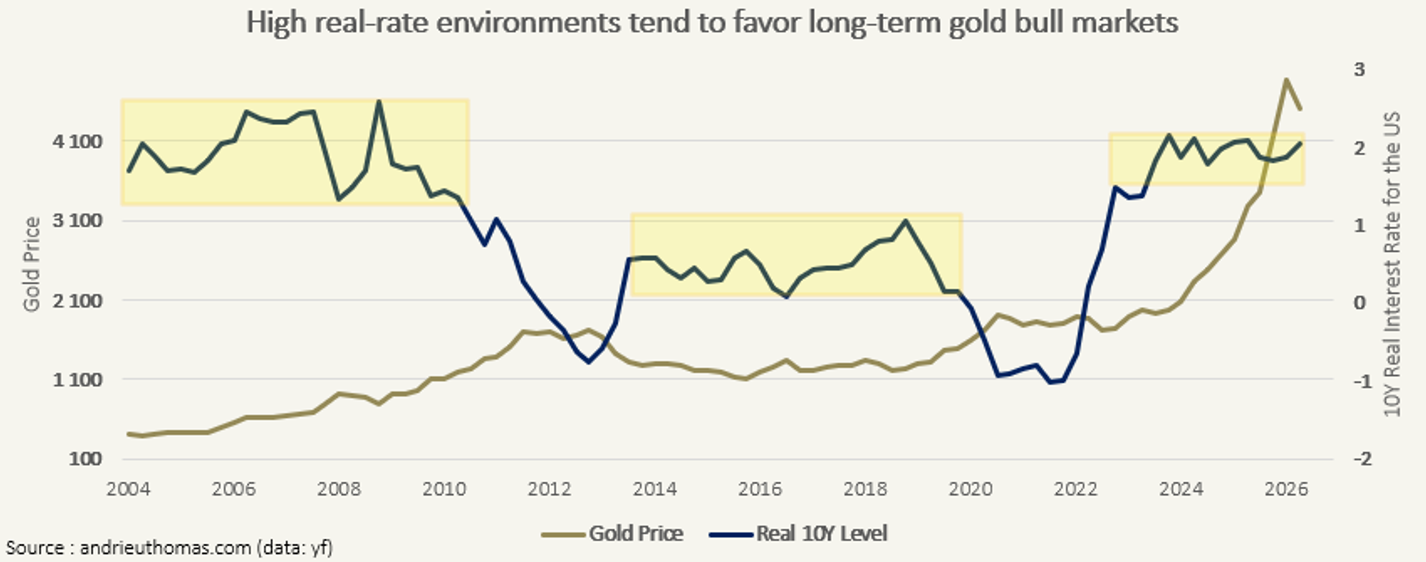

Moreover, their decisions, and in particular those of the Fed, which remains the world's central bank, have played a key role in gold this year. After a period of monetary tightening, they opted for a pause over the summer, followed by an interest rate cut, marking a turning point after four years of increases. This decision weakened the value of bonds and short-term assets, which in turn boosted gold's appeal. The forthcoming interest-rate cuts scheduled for the coming weeks and months will further amplify this trend. Furthermore, if the dollar's influence on the gold price is almost non-existent today (with gold now decoupled from its historical influences), the current overvaluation of the US currency - estimated at almost 10% - could also provide further support for the yellow metal.

The global financial landscape is also changing. De-dollarization is becoming a priority for many states, local currencies are gaining ground in international trade, and the economic headlong rush of the Western powers is giving air to the creation of new structures by the BRICS - including the Russian messaging system currently underway. This period is leading to changes in fiscal and financial policies that benefit gold (it also lends itself perfectly to the organization of a new international economic system at a summit dedicated to the BRICS).

With this in mind, it's worth remembering that the central banks of the BRICS countries are the main buyers of gold. And their contribution is of major importance. They are continuing to build up their reserves at a steady pace, enabling solid and visibly sustainable institutional demand. By acquiring more than 1,000 tons per annum over the past two years - a historic threshold never reached before - they are demonstrating a clear determination to secure their economies in the face of growing global instability and unilateral economic sanctions by the West (notably those targeting Iran in the early 2010s and Russia in 2022). This trend could accelerate, especially after statements such as those made by Donald Trump who, if re-elected, intends to impose 100% tariffs on countries that abandon the use of the dollar. Over the past few years, the dollar's extraterritoriality, combined with the economic sanctions imposed in the past, has led to an acceleration in global de-dollarization. Today, 65% of trade between the BRICS countries already takes place outside the dollar, not to mention the fact that the share of reserves in US currency continues to decline...

Among these major players, China occupies a central position. At the head of this movement, it is particularly motivated by the accumulation of gold for financial reasons (not all of its purchases are recorded, by the way) as well as political, given the ongoing tensions with the United States. But China is not isolated in this dynamic. This phenomenon is part of a global trend towards reserve diversification. Ongoing geopolitical conflicts (including Ukraine, the Middle East, and the growing risks in Taiwan), the American election, which will have a major influence on the world stage, and central bank purchases, which play a confidence-building role, are pushing investors more widely to abandon traditional financial assets, deemed too risky, and turn to gold. Not only in the so-called “South”, but also among Western investors, who have been buying gold on a massive scale since the summer, with back-to-back purchases in gold-backed exchange-traded funds.

These massive movements are no accident. They are part of a historical dynamic in which, in every period of uncertainty, gold serves not only as a safe haven but also as an indicator of future crises. This year's trend is further proof of this, as geopolitical conflicts intensify and the global economy shows its fragility more than ever. This obvious fact, however, can only be understood through a long-term analysis. We are at the dawn of major transformations, and gold seems ready to play its historic role more than ever.

More By This Author:

Silver Vs U.S. Stock Indexes Says "Silver Is Cheap"A Massive Short Squeeze On Gold?

US Fiscal Policy Paves The Way For A New Inflationary Cycle

Comments

Log in or sign up to join the conversation.