One day after futures ramped overnight (if only to crater during the regular session) on hopes China was easing its highly politicized Zero Covid policy after it cut the time of quarantine lockdowns, this morning futures slumped early on after China's President Xi Jinping made clear that Covid Zero isn't going anywhere and remains the most “economic and effective” policy for China during a symbolic visit to the virus ground zero in Wuhan, in which he cast the strategy as proof of the superiority of the country’s political system.

That coupled with renewed recession worries (market is again pricing in a rate cut in Q1 2023) even as monetary policy tightens in much of the world to fight supply-side inflation, sent US futures and global markets lower. S&P futures dropped 0.2% and Nasdaq 100 futures were down 0.4% after the underlying index slumped on 3.1% on Tuesday. The dollar was steady after rising the most in over a week while WTI crude climbed above $112 a barrel, set for a fourth session of gains. In cryptocurrencies, Bitcoin dipped below the closely watched $20,000 level on news crypto hedge fund 3 Arrows Capital was ordered to liquidate.

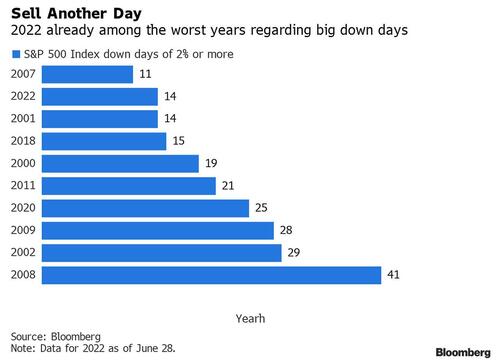

The Nasdaq's Tuesday’s slump added to what was already one of the worst years in terms of big daily selloffs in US stocks. The S&P 500 Index has fallen 2% or more on 14 occasions, putting 2022 in the top 10 list, according to Bloomberg data.

Not helping the tech sector, on Wednesday morning JPMorgan cut its earnings estimates across the sector, especially for companies exposed to online advertising, citing macroeconomic pressures, forex and company-specific dynamics.

One of the chief drivers for overnight weakness, China's Xi said during a trip Tuesday to Wuhan where the virus first emerged in late 2019 that relaxing Covid controls would risk too many lives in the world’s most populous country. China would rather endure some temporary impact on economic development than let the virus hurt people’s safety and health, he said, in remarks reported Wednesday by state media. As a result, China’s CSI 300 Index extended loss to 1.4% after the headline, while the yuan drops as much as 0.2% to trade 6.7132 against the dollar in the offshore market.

Among key premarket movers, Tesla slipped in US premarket trading. The electric-vehicle maker laid off hundreds of workers on its Autopilot team as it shuttered a California facility, according to people familiar with the matter. Carnival slumped as Morgan Stanley analysts warned that the London and New York-listed cruise vacation company’s shares could lose all their value in the event of another demand shock. Pinterest gained 3.7% as the company’s co- founder and CEO Ben Silbermann quit and handed the reins to Google and PayPal veteran Bill Ready in a sign the social-media company will focus more on e-commerce. Also, despite the pervasive weakness, the Energy Select Sector SPDR Fund ETF (XLE) rebounded off key support (50% Fibonacci) relative to the SPDR S&P 500 ETF (SPY). That said, energy was alone and most other notable movers were down in the premarket:

- Carnival (CCL US) shares fall 8% premarket as Morgan Stanley analysts warned that the cruise vacation firm’s shares could lose all their value in the event of another demand shock.

- Nio (NIO US) shares drop 8.2% after short-seller Grizzly Research published a report on Tuesday alleging that the electric carmaker used battery sales to a related party to inflate revenue and boost net income margins. The company rejected the claims.

- Upstart Holdings (UPST US) shares slump about 9% after Morgan Stanley downgraded the consumer finance company to underweight from equal-weight amid rising cyclical headwinds.

- Ormat Technologies (ORA US) rallies as much as 5% after the renewable energy company is set to be included in the S&P Midcap 400 Index.

- 2U (TWOU US) shares rise 16% premarket. Indian online-education provider Byju’s has offered to buy the company in a cash deal that values the US-listed edtech firm at more than $1 billion, a person familiar with the matter said.

- Watch Amazon (AMZN US) shares as Redburn initiated coverage of the stock with a buy recommendation and set a Street-high price target, saying “there is a clear path toward a $3 trillion value for AWS alone.”

- Shares in data center REITs could be active later in the trading session after short-seller Jim Chanos said in an FT interview that he’s betting against “legacy” data centers. Watch Digital Realty (DLR US) and Equinix (EQIX US), as well as data center operators Cyxtera Technologies (CYXT US) and Iron Mountain (IRM US)

Investors are growing increasingly skeptical that the Fed can avoid a bruising economic downturn amid sharp interest-rate hikes. Evaporating consumer confidence is feeding into concerns that the US might tip into a recession. Naturally, Fed officials sought to play down recession risk. New York Fed President John Williams and San Francisco’s Mary Daly both acknowledged they had to cool inflation, but insisted that a soft landing was still possible.

“It seems the market is in this tug of war between on the one hand the hope that we are close to the peak in inflation and rates, and on the other hand the challenge of a slowing economy and potential recession,” Emmanuel Cau, head of European equity strategy at Barclays Bank Plc, said in an interview with Bloomberg TV. “Central banks are walking a very tight line and to a certain extent dictate the mood in the markets.”

European equities snapped three days of gains, trading poorly but off worst levels with sentiment also hurt by China remaining committed to its zero-Covid approach. Spanish inflation unexpectedly surged to a record, dashing hopes that inflation in the euro zone’s fourth-biggest economy had peaked, and emboldening European Central Bank policy makers pushing for big increases in interest rates. The ECB should consider raising interest rates by twice the planned amount next month if the inflation outlook deteriorates, according to Governing Council member Gediminas Simkus, as calls not to exclude an outsized initial move grow. German benchmark bonds rose, while 10-year Treasury yields slipped to 3.16%. DAX lags, dropping as much as 1.8%. Real estate, autos and miners are the worst performing sectors.

In notable moves in European stocks, Hennes & Mauritz (H&M) gained after the Swedish low-cost retailer’s earnings beat analyst estimates. Just Eat Takeaway.com NV tumbled to a record low after Berenberg analysts rated the stock sell, saying the food delivery firm’s UK business will remain under pressure. Here are some of the biggest European movers today:

- Just Eat Takeaway shares plunge as much as 21% after Berenberg initiated coverage with a sell rating, saying the firm’s UK business will remain under pressure and a sale of its Grubhub unit is unlikely to satisfy the bulls.

- Carnival stocks slumped over 12% in London as Morgan Stanley analysts warned that the cruise vacation firm’s shares could lose all their value in the event of another demand shock.

- Pearson drops as much as 6.1% after the education company was cut to sell at UBS, which reduced forecasts to reflect a weak outlook for 2022 college enrollments.

- Grifols shares plunge as much as 13% on a media report the Spanish plasma firm is weighing a capital raise of as much as EU2b to cut its debt.

- Diageo shares fall after downgrades for the spirits group from Deutsche Bank and Kepler Cheuvreux, while Pernod Ricard also dips on a rating cut from the latter.

- Diageo declines as much as 4.2%, Pernod Ricard -3.7%

- Fluidra shares fall as much as 8.4% after Santander cut its rating on the Spanish swimming pools company. The bank’s analyst Alejandro Conde cut the recommendation to neutral from outperform.

- H&M shares rise as much as 6.8% after the Swedish apparel retailer reported 2Q earnings that beat estimates. Jefferies said the margin beat in particular was reassuring, while Morgan Stanley said it was a “positive surprise” overall.

- Ipsen shares rise as much as 3.1% after UBS analyst Michael Leuchten said that accepting palovarotene refiling priority review should be a net present value and confidence boost.

Asian stocks fell, halting a four-day gain, as renewed angst over the outlook for global economic growth and inflation help drive a selloff across most of the region’s equity markets. The MSCI Asia Pacific Index dropped as much as 1.5%, led by consumer discretionary and information sectors. Chinese equities in particular took a hit, as the CSI 300 Index fell 1.5% Wednesday after Xi Jinping reiterated his firm stance on Covid zero. Tech-heavy indexes in markets such as South Korea and Taiwan took the brunt of Wednesday’s drop amid lingering concerns that monetary tightening in much of the world to fight inflation will cause an economic slowdown. While Federal Reserve members have played down the risk of a US recession, gloomy data such as US consumer confidence have damped investor sentiment.

“Volatility is going to be the enduring feature of the market, I suspect, for the next couple of quarters at least until we get a firm sense that peak inflation has passed,” John Woods, Credit Suisse Group AG’s Asia-Pacific chief investment officer, said in an interview with Bloomberg TV. “Markets, I think, have aggressively priced in quite a serious or steep recession.” China’s four-day winning streak came to a halt, putting its advance toward a bull market on hold. “We will continue to see a risk of targeted lockdowns, and that spoils the initial euphoria seen in the markets from the announcement on relaxation of quarantine requirements,” said Charu Chanana, market strategist at Saxo Capital Markets. “Still, economic growth will likely be prioritized as this is a politically important year for China.”

Japanese equities decline as investors digested data that showed a drop in US consumer confidence over inflation worries and increased concerns of an economic downturn. The Topix Index fell 0.7% to 1,893.57 in Tokyo on Wednesday, while the Nikkei declined 0.9% to 26,804.60. Toyota Motor Corp. contributed the most to the Topix’s decline, decreasing 1.8%. Out of 2,170 shares in the index, 1,114 fell, 984 rose and 72 were unchanged. “There are concerns about stagflation,” said Hideyuki Suzuki a general manager at SBI Securities. “The consumer sentiment from the University of Michigan, which provides one of the fastest data points, has already shown poor figures.”

Stocks in India tracked their Asian peers lower as brent rose to the highest level in two weeks, while high inflation and slowing global growth continued to dampen risk-appetite for global equities. The S&P BSE Sensex fell 0.3% to 53,026.97 in Mumbai, while the NSE Nifty 50 Index declined by an equal measure. Both gauges have lost more than 4% in June and are set for their third consecutive month of declines. The main indexes have dropped for all but one month this year. Twelve of the 19 sub-sector gauges compiled by BSE Ltd. eased, led by banking companies while power producers were the top performers. Investors will also be watching the expiry of monthly derivative contracts on Thursday, which may lead to some volatility in the markets. Hindustan Unilever was the biggest contributor to the Sensex’s decline, decreasing 3.5%. Out of 30 shares in the Sensex, 10 rose and 20 fell.

The Bloomberg Dollar Spot Index inched up modestly as the greenback traded mixed against its Group-of-10 peers; the Swiss franc led gains while Antipodean currencies were the worst performers and the euro traded in a narrow range around $1.05. The relative cost to own optionality in the euro heading into the July meetings of the ECB and the Federal Reserve was too low for investors to ignore and has become less and less underpriced. The yen strengthened and US and Japanese bond yields fell.

In rates, fixed income has a choppy start. Bund futures initially surged just shy of 200 ticks on a soft regional German CPI print before fading the entire move over the course of the morning as Spanish data hit the tape, delivering a surprise record 10% reading for June and more hawkish ECB comments crossed the wires. Treasuries and gilts followed with curves eventually fading a bull-steepening move. Long-end gilts underperform, cheapening ~4bps near 2.75%. Peripheral spreads are tighter to core.

Treasuries are slightly higher as US trading day begins, off the session lows reached as bund futures jumped after the first monthly drop since November in a German regional CPI gauge. Yields are lower across the curve, by 1bp-2bp for tenors out to the 10-year with long-end yields little changed; 10-year declined as much as 5.3bp vs as much as 8.2bp for German 10- year, which remains lower by ~3bp. Focal points for the US session include a final revision of 1Q GDP, comments by Fed Chair Powell, and anticipation of quarter-end flows favoring bonds. Quarter-end is anticipated to cause rebalancing flows into bonds; Wells Fargo estimated that $5b will be added to bonds, with most of the flows occurring Wednesday and Thursday.

In commodities, crude futures advance. WTI drifts 0.3% higher to trade near $112.13. Base metals are mixed; LME tin falls 5.6% while LME zinc gains 0.4%. Spot gold falls roughly $5 to trade near $1,815/oz

Looking ahead, the highlight will be the panel at the ECB Forum that includes Fed Chair Powell, ECB President Lagarde and BoE Governor Bailey. We’ll also be hearing from ECB Vice President de Guindos, the ECB’s Schnabel, the Fed’s Mester and Bullard, and the BoE’s Dhingra. On the data side, releases include German CPI for June, Euro Area money supply for May, and the final Euro Area consumer confidence reading for June. From the US, we’ll also get the third reading of Q1 GDP.

Market Snapshot

- S&P 500 futures little changed at 3,829.00

- STOXX Europe 600 down 0.8% to 412.69

- MXAP down 1.3% to 159.96

- MXAPJ down 1.6% to 531.04

- Nikkei down 0.9% to 26,804.60

- Topix down 0.7% to 1,893.57

- Hang Seng Index down 1.9% to 21,996.89

- Shanghai Composite down 1.4% to 3,361.52

- Sensex little changed at 53,204.17

- Australia S&P/ASX 200 down 0.9% to 6,700.23

- Kospi down 1.8% to 2,377.99

- German 10Y yield little changed at 1.59%

- Euro little changed at $1.0510

- Brent Futures down 0.4% to $117.46/bbl

- Gold spot down 0.2% to $1,816.09

- U.S. Dollar Index little changed at 104.55

Comments

Log in or sign up to join the conversation.