Futures Slide After China's "Huge" Data Miss Sparks "Broad-Based Recession Talk"

Friday's bear market rally dead-cat bounce appears to be over, and global stocks have started the new week in the red with US equity futures lower after a "huge miss", as Bloomberg put it, in Chinese data fueled concerns over the impact of a slowdown in the world’s second-largest economy. As reported last night, China’s industrial output and consumer spending hit the worst levels since the pandemic began, hurt by Covid lockdowns.

(Click on image to enlarge)

And even though officials took another round of measured steps to help the economy by cutting the interest rate for new mortgages over the weekend to bolster an ailing housing market, even as they left the one-year policy loan rate was left unchanged Monday, few believe that any of these actions will have a tangible impact and most continue to expect much more from Beijing.

As such, after a weekend that saw even Goldman's perpetually optimistic equity strategists slash their S&P target (again) from 4,700 to 4,300, and amid growing fears that a recession is now inevitable, Nasdaq 100 futures slid as much as 1.2%, before paring losses to 0.4% as of 730 a.m. in New York. S&P 500 futures were down 0.3%. 10Y Treasury yields were flat at 2.91% and the dollar dipped modestly while bitcoin traded just above $30,000 dropping from $31,000 earlier in the session.

(Click on image to enlarge)

Among notable moves in premarket trading, Spirit Airlines jumped as much as 21% following a report that JetBlue Airways is planning a tender offer at $30 a share in cash. Major US technology and internet stocks were down after rebounding on Friday, while Tesla shares dropped, with the electric-vehicle maker set to recall 107,293 cars in China over a potential safety risk. Twitter shares fall 3.4% in premarket trading on Monday, on course to wipe out all the gains the stock has made since billionaire Elon Musk disclosed his stake in the social media platform. Twitter fell to as low as $37.86 -- below the the April 1 close of $39.31, before Musk disclosed his stake.

US stocks have been roiled this year, with the S&P 500 on tick away from a bear market as recently as last Thursday, on worries of an aggressive pace of rate hikes by the Federal Reserve at a time when macroeconomic data showed a slowdown in growth. Data from China on Monday highlighted a massive toll on the economy from Covid-19 lockdowns, with retail sales and industrial output both contracting.

Although lower valuations sparked a rally in stocks on Friday, strategists including Morgan Stanley’s Michael Wilson warned of more losses ahead as equity markets also price in slower corporate earnings growth. Goldman Sachs strategists led by David Kostin cut their year-end target for the S&P 500 on Friday to 4,300 points from 4,700.

"The broad-based recession talk is the major catalyzer this Monday,” Ipek Ozkardeskaya, a senior analyst at Swissquote, wrote in a note. “Activity in US futures hint that Friday’s rebound was certainly nothing more than a dead cat bounce” just as we said at the time.

The risk of an economic downturn amid price pressures and rising borrowing costs remains the major worry for markets. Goldman Sachs Group Senior Chairman Lloyd Blankfein urged companies and consumers to gird for a US recession, saying it’s a “very, very high risk.” Traders remain wary of calling a bottom for equities despite a 17% drop in global shares this year, with Morgan Stanley warning that any bounce in US stocks would be a bear-market rally and more declines lie ahead.

In Europe, the Stoxx Europe 600 index fell as much as 0.8% before paring losses, with declines for tech and travel stocks offsetting gains for basic resources as industrial metals rallied. The Euro Stoxx 50 falls 0.4%. IBEX outperforms, adding 0.3%. Tech, personal care and consumer products are the worst performing sectors. Here are some of the biggest European movers today:

- Basic Resources stocks outperformed with broad gains among mining and steel companies; ArcelorMittal +3.5%; SSAB +2.6%; Glencore +2.1%; Voestalpine +3.1%.

- Sartorius AG and Sartorius Stedim shares gain as UBS upgrades both stocks to buy following a “significant de-rating” for the lab-equipment companies, seeing supportive global trends.

- Carl Zeiss Meditec gains as much as 4.9% after HSBC raised its recommendation to buy from hold, saying the medical optical manufacturer is “well-equipped to deal with supply chain challenges.”

- Interpump rises as much as 7.6%, extending winning streak to five days, as Banca Akros upgrades the stock to buy from accumulate following Friday’s 1Q results.

- Casino shares jump as much 5.8% after the French grocer said it’s started a process to sell its GreenYellow renewable energy arm, confirming a Bloomberg News report from Friday.

- Ryanair shares decline as much as 4.3% on FY results, with analysts focusing on the low-budget carrier’s recovery outlook. They note management is cautiously optimistic about summer travel.

- Vantage Towers shares decline after the company posted FY23 adjusted Ebitda after leases and recurring free cash flow forecasts that missed analyst estimates at mid- points.

- Unilever falls after a 13-F filing from Nelson Peltz’s Trian shows no position in the company, according to Jefferies, damping speculation after press reports earlier this year that the fund had built a stake.

- Michelin shares fall as much as 3.7% after being downgraded to neutral from overweight at JPMorgan, which says it writes off any chance of seeing a recovery in volume production growth in FY22.

Earlier in the session, Asian stocks eked out modest gains as surprisingly weak Chinese economic data spurred volatility and caused traders to reassess their outlook on the region. The MSCI Asia-Pacific Index was up 0.1%, paring an earlier advance of as much as 0.9% on stimulus hopes. The region’s information technology index rose as much as 1.5%, with TMSC giving the biggest boost. A sub-gauge on materials shares fell the most.

Equities in China led losses, as Beijing’s moves to cut the mortgage rate for first-time home buyers and ease lockdown restrictions in Shanghai failed to reverse the downbeat mood. Asian stocks were trading higher early Monday, building on Friday’s rally, only to trim or reverse gains as data showed a sharper-than-expected contraction in Chinese activity in April. Signs of an earnings recovery in China are needed for investors to come back, Arnout van Rijn, chief investment officer for APAC at Robeco Hong Kong Ltd., said on Bloomberg Television.

“It looks like China is not going to meet the 15% earnings growth that people were looking for just a couple of months ago. So now we’re looking for five, 10, maybe it’s even going to fall to zero.” Meanwhile, JPMorgan analysts, who had called China tech “uninvestable” in March, upgraded some tech heavyweights including Alibaba in a Monday report, citing less regulatory uncertainties. Benchmarks in Japan, Australia, India and Taiwan maintained gains while Hong Kong also recovered some ground later in the day. Markets in Singapore, Thailand, Malaysia and Indonesia were closed for holidays.

Japanese equities were mixed, with the Topix closing slightly lower after worse-than-expected Chinese economic data amid the impact from virus-related lockdowns. The Topix fell 0.1% to close at 1,863.26, with Honda Motor contributing the most to the decline after its forecast for the current year missed analyst expectations. The Nikkei advanced 0.5% to 26,547.05, with KDDI among the biggest boosts after announcing its results and a 200 billion yen buyback. “Though the lockdowns in China are pushing down the economy and causing supply chain difficulties, there’s a positive outlook since the weekend that there could be a gradual easing of the lockdowns as it seems that virus cases have peaked out,” said Masashi Akutsu, chief strategist at SMBC Nikko Securities.

In Australia, the S&P/ASX 200 index rose 0.3% to 7,093.00, trimming an earlier advance of as much as 1.1% after soft Chinese economic data stoked concerns about global growth. Read: Aussie, Kiwi Slump After Weak China Data: Inside Australia/NZ Brambles was the top performer after confirming it’s in talks with private equity firm CVC Capital Partners on a takeover proposal. Qube also climbed after completing a A$400 million share buyback. In New Zealand, the S&P/NZX 50 index fell 0.1% to 11,157.66.

In rates, Treasuries were steady with yields within 1bp of Friday’s close. US 10-year yield near flat ~2.91% with bunds cheaper by ~5bp, gilts ~3.5bp amid heavy. German 10-year yield up 5 bps, trading narrowly below 1%. Italian 10-year bonds underperform, with the 10-year yield up 8 bps to 2.93%. Peripheral spreads are mixed to Germany; Italy and Spain widen and Portugal tightens. The Italy 10-year was cheaper by more than 6bp on the day amid renewed ECB jawboning. Core European rates are higher, pricing in ECB policy tightening. During Asia session, Chinese data showed industrial output and consumer spending at worst levels since the pandemic began. The dollar issuance slate includes CBA 3T covered SOFR; $30b expected for this week as syndicate desks seek opportunities for pent-up supply. Three-month dollar Libor +1.13bp at 1.45500%.

In FX, the Bloomberg Dollar Spot Index was little changed while the greenback advanced against most of its Group-of-10 peers. Treasuries inched lower, led by the front end, and outperformed European bonds. The euro inched up against the dollar. Italian bonds dropped, leading peripheral underperformance against euro- area peers, while money markets showed increased ECB tightening wagers after policy maker Francois Villeroy de Galhau said a consensus is “clearly emerging” at the central bank on normalizing monetary policy and that June’s meeting will be “decisive.” He also signaled that the weakness of the euro is focusing the minds of ECB policy makers at a time when the currency is heading toward parity with the dollar. The euro may resume its rally versus the pound in the spot market as options traders pile up bullish wagers. The pound fell against both the dollar and euro, staying under selling pressure on concerns that high UK inflation will weigh on the economy. Markets await testimony from Bank of England Governor Andrew Bailey and other central bank officials later in the day, ahead of a reading of April inflation later in the week. Australian and New Zealand dollars fell after Chinese industrial and consumer data fanned concerns of a further slowdown in the world’s second-largest economy.

In commodities, WTI drifts 0.4% lower to trade above $110. Spot gold pares some declines, down some $6, but still around $1,800/oz. Most base metals trade in the green; LME tin rises 3.4%, outperforming peers. Bitcoin falls 4.6% to trade below $30,000

Looking ahead, we get the US May Empire manufacturing index, Canada April housing starts, March manufacturing, wholesale trade sales. Central bank speakers include the Fed's Williams, ECB's Lane, Villeroy and Panetta, BOE's Bailey, Ramsden, Haskel and Saunders. We get earnings from Ryanair, Take-Two Interactive.

Market Snapshot

- S&P 500 futures down 0.3% to 4,008.75

- STOXX Europe 600 little changed at 433.33

- MXAP up 0.2% to 160.34

- MXAPJ up 0.2% to 523.32

- Nikkei up 0.5% to 26,547.05

- Topix little changed at 1,863.26

- Hang Seng Index up 0.3% to 19,950.21

- Shanghai Composite down 0.3% to 3,073.75

- Sensex up 0.6% to 53,119.79

- Australia S&P/ASX 200 up 0.3% to 7,093.03

- Kospi down 0.3% to 2,596.58

- German 10Y yield little changed at 0.98%

- Euro up 0.1% to $1.0424

- Brent Futures down 1.4% to $109.98/bbl

- Gold spot down 0.8% to $1,797.30

- US Dollar Index little changed at 104.46

Top Overnight News from Bloomberg

- NATO members rallied around Finland and Sweden on Sunday after they announced plans to join the alliance, marking another dramatic change in Europe’s security architecture triggered by Russia’s war in Ukraine

- The euro area’s pandemic recovery would almost grind to a halt, while prices would surge even more quickly if there are serious disruptions to natural-gas supplies from Russia, according to new projections from the European Commission

- UK energy regulator Ofgem plans to adjust its price cap every three months instead of every six. Changing the level more often would help consumers to take advantage of falling wholesale prices more quickly, it said in a statement Monday. This would also mean higher prices filter through bills quicker

- Boris Johnson has warned Brussels that the UK government will press ahead with unilateral changes to parts of the Brexit agreement if it does not engage in “genuine dialogue”

- While debt bulls on Wall Street have been crushed all year, market sentiment has shifted markedly over the past week from inflation fears to growth. That theme gathered more strength Monday, when data showing China’s economy contracted sharply in April set off fresh gains for Treasuries

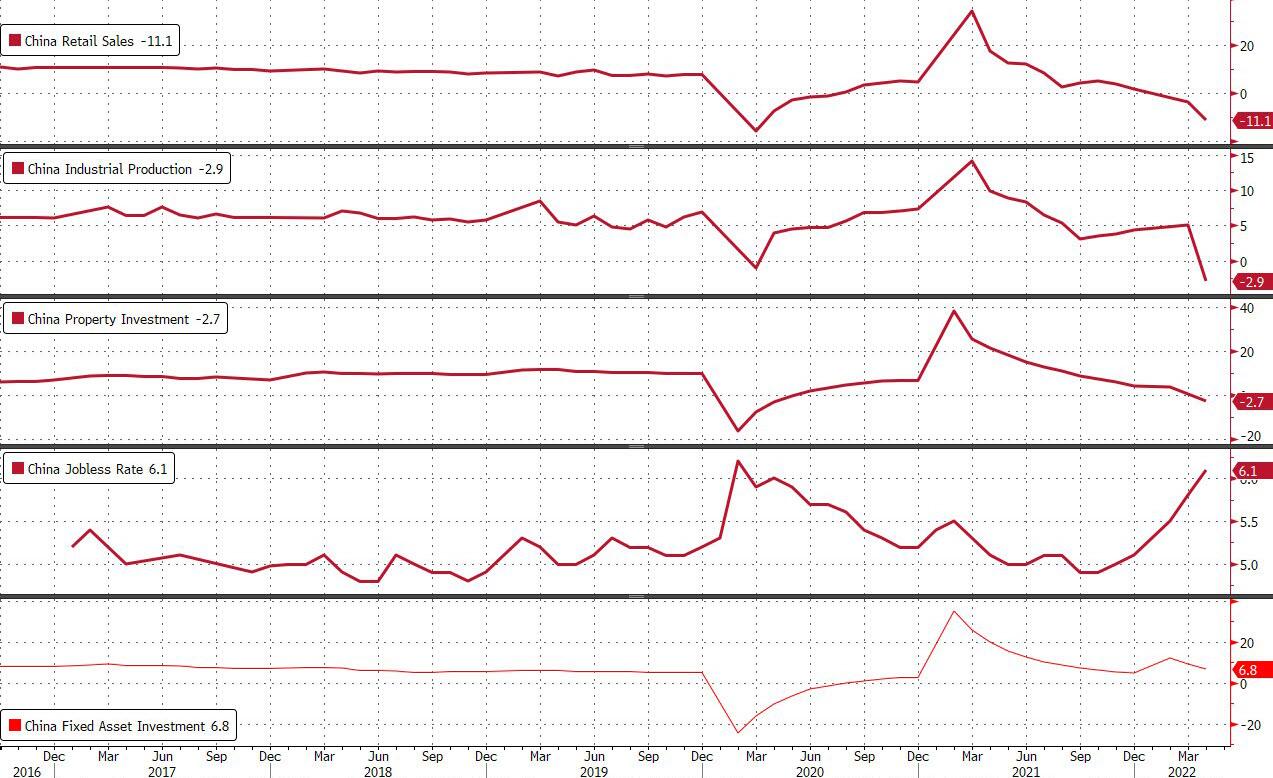

- China’s economy is paying the price for the government’s Covid Zero policy, with industrial output and consumer spending sliding to the worst levels since the pandemic began and analysts warning of no quick recovery. Industrial output unexpectedly fell 2.9% in April from a year ago, while retail sales contracted 11.1% in the period, weaker than a projected 6.6% drop

- Japanese manufacturers are increasingly looking to move offshore operations to their home market, according to a Tokyo Steel Manufacturing Co. executive. The rapidly weakening yen, global supply-chain constraints, geopolitical risks and shifting wages patterns are prompting the switch, Kiyoshi Imamura, a managing director of the steelmaker, said in an interview in Tokyo last week

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed after disappointing Chinese activity data clouded over the early momentum from Friday’s rally on Wall St. ASX 200 was higher as tech stocks were inspired by US counterparts and amid M&A related newsflow with Brambles enjoying a double-digit percentage gain after it confirmed it had talks with CVC regarding a potential takeover by the latter. Nikkei 225 kept afloat as earnings releases provided the catalysts for individual stocks but with gains capped by a choppy currency. Hang Seng and Shanghai Comp initially gained with property names underpinned after China permitted a further reduction in mortgage loan interest rates for first-time home purchases and with casino stocks also firmer in the hope of a tax reduction on gaming revenue. However, the mood was then spoiled by weak Chinese data and after the PBoC maintained its 1-year MLF rate.

Top Asian News

- PBoC conducted a CNY 100bln in 1-year MLF with the rate kept unchanged at 2.85% and stated the MLF and Reverse Repo aim to keep liquidity reasonably ample, according to Bloomberg.

- Beijing extended work from home guidance in several districts and announced three additional rounds of mass COVID-19 testing in most districts including its largest district Chaoyang, according to Reuters.

- Shanghai will gradually start reopening businesses including shopping malls and hair salons in China's financial and manufacturing hub beginning on Monday following weeks of a strict lockdown, according to Reuters.

- Shanghai city official said 15 out of the 16 districts achieved zero-COVID outside quarantine areas and the city's epidemic is under control but added that risks of a rebound remain and they will need to continue to stick to controls. The official said the focus until May 21st will be to prevent risks of a rebound and many movement restrictions are to remain, while they will look to allow normal life to resume in Shanghai from June 1st and will begin to reopen supermarkets, convenience stores and pharmacies from today, according to Reuters.

- Chinese financial authorities permitted a further reduction in mortgage loan interest rates for some home buyers whereby commercial banks can lower the lower limit of interest rates on home loans by 20bps based on the corresponding tenor of benchmark Loan Prime Rates for purchases of first homes, according to Reuters.

- China's stats bureau spokesman said economic operations are expected to improve in May and that China is steadily pushing forward production resumption in COVID-hit areas, while they expect China's economic recovery and rebound in consumption to quicken but noted that exports face some pressure as the global economy slows, according to Reuters.

- Macau is reportedly considering a tax cut for casinos amid a decline in gaming revenue in which a cut could be as much as 5% off the current 40% levied on casino gaming revenue, according to Bloomberg.

European bourses are mixed, Euro Stoxx 50 -0.6%, following a similar APAC session with impetus from Shanghai's reopening offset by activity data and geopolitics. Stateside, futures are lower across the board, ES -0.4%, with the NQ marginally lagging as yields lift; Fed's Williams due later before Powell on Tuesday. US players are focused on whether the end-week bounce is a turnaround from technical bear-market levels or not. China's market regulator says Tesla (TSLA) has recalled 107.3k Model 3 & Y vehicles, which were made in China. JetBlue (JBLU) is to launch a tender offer for Spirit Airlines (SAVE); JetBlue is to offer USD 30/shr, but prepared to pay USD 33/shr if Spirit provides JetBlue with requested data, WSJ sources say. Elon Musk tweeted that Twitter’s (TWTR) legal team called to complain that he violated their NDA by revealing the bot check sample size and he also tweeted there is some chance that over 90% of Twitter’s daily active users might be bots.

Top European News

- UK PM Johnson is reportedly set to give the green light for a bill on the Northern Ireland protocol, according to the Guardian.

- UK PM Johnson said he hopes the EU changes its position on the Northern Ireland protocol and if not, he must act, while he sees a sensible landing spot for a protocol deal and will set out the next steps on the protocol in the coming days, according to Reuters.

- UK PM Johnson is expected to visit Northern Ireland on Monday for talks with party leaders in an effort to break the political deadlock at Stormont, according to Sky News.

- Irish Foreign Minister Coveney says the EU is prepared to move on reducing checks on goods coming into the region from Britain, via Politico.

- UK Cabinet ministers have turned on the BoE regarding rising inflation, whereby one minister warned that the Bank was failing to "get things right" and another suggested that it had failed a "big test", according to The Telegraph.

- Group of over 50 economists warned that the UK's post-Brexit plans to boost the competitiveness of its finance industry risk creating the sort of problems that resulted in the GFC, according to Reuters.

- European Commission Spring Economic Forecasts: cuts 2022 GDP forecast to 2.7% from the 4.0% projected in February. Click here for more detail.

Central Banks

- ECB's Villeroy expects a decisive June meeting and an active summer meeting, pace of further steps will account for actual activity/inflation data with some optionality and gradualism; but, should at least move towards the neutral rate. Will carefully monitor developments in the effective FX rate, as a significant driver of imported inflation; EUR that is too weak would go against the objective of price stability.

- ECB’s de Cos said the central bank will likely decide at the next meeting to end its stimulus program in July and raise rates very soon after that, while he added that they are not seeing second-round effects and are monitoring it, according to Reuters.

FX

- Euro firmer following verbal intervention from ECB’s Villeroy and spike in EGB yields EUR/USD rebounds from sub-1.0400 to 1.0435 at best.

- Dollar up elsewhere as DXY pivots 104.500, but Yen resilient on risk grounds as Chinese data misses consensus by some distance; USD/JPY capped into 129.50.

- Franc falls across the board after IMM specs raise short bets and Swiss sight deposits show SNB remaining on the sidelines; USD/CHF above 1.0050 at one stage.

- However, HKMA continues to defend HKD peg amidst CNY, CNH weakness in wake of disappointing Chinese industrial production and retail sales releases.

- Norwegian Crown undermined by pullback in Brent and narrower trade surplus, EUR/NOK over 10.2100.

- SA Rand soft as Gold retreats to test support around and under Usd 1800/oz.

- Loonie slips with WTI ahead of Canadian housing starts, manufacturing sales and wholesale trade, Sterling dips before BoE testimony; USD/CAD 1.2900+, Cable sub-1.2250.

Fixed income

- EGBs rattled by ECB rhetoric inferring key policy meetings kicking off in June and extending through summer.

- Bunds down towards 153.00 and 10 year yield back up around 1%, Gilts almost 1/2 point adrift and T-note erasing gains from 12/32+ above par at best.

- Eurozone periphery underperforming with added risk-off angst following much weaker than expected Chinese data.

In commodities

- WTI and Brent are pressured, but well off lows, and torn between China's lockdown easing and poor activity data amid numerous other catalysts

- Specifically, the benchmarks are around USD 110/bbl and USD 111/bbl respectively,

- Saudi Aramco Q1 net income rose 82% Y/Y to INR 39.5bln for its highest quarterly profit since listing, according to Sky News.

- Saudi Energy Minister says they are going to get to 13.2-13.4mln BPD, subject to what is done in the divided zone, by end-2026/start-2027; can maintain production when there, if the market demands this.

- OPEC+ to continue with monthly output increases, according to Bahrain's oil minister via Reuters.

- Iraqi state-run North Oil Company said Kurdish armed forces took control of some oil wells in northern Kirkuk, according to Reuters.

- Iraq oil minister says they aim to increase oil production to 6mln BPD by end-2027, OPEC is targeting a energy market balance not a price; adding, current production capacity is 4.9mln BPD, will reach 5mln BPD before the end of 2022.

- China is to increase fuel prices from Tuesday, according to China's NDRC; gasoline by CNY 285/t and diesel by CNY 270/t.

US Event Calendar

- 08:30: May Empire Manufacturing, est. 15.0, prior 24.6

- 16:00: March Total Net TIC Flows, prior $162.6b

DB's Jim Reid concludes the overnight wrap

Markets managed a big bounce on Friday but the mood has soured again in the Asian session after a weak slew of data from China as covid lockdowns had an even worse impact than expected. Industrial production (-2.9% vs +0.5% expected), retail sales (-11.1% vs -6.6% expected) and property investment (-2.7% vs -1.5% expected) all crashed through estimates by a large margin. The slump in retail sales and industrial production was the weakest since March 2020. The latter also had the lowest print on record, with the worst decline coming from auto manufacturing (-31.8%). The surveyed jobless rate (6.1% vs estimates of 6.0%) also ticked up by more than expected from 5.8% in March and is now close to the high of 6.2% in February 2020. Although the 1-year policy loan rate was left unchanged today, the PBoC did ease the rate on new mortgages this weekend. In other data releases, Japan’s April PPI (+10.0%) came in above estimates of +9.4%, the highest since 1980.

Amid this, the Shanghai Composite (-0.51%) and the Hang Seng (-0.43%) are in the red, and outperformed by the KOSPI (-0.21%) and the Nikkei (+0.46%). The sentiment has soured in American markets too, with S&P 500 futures also trading lower (-0.68%) and the US 10y yield declining by -2.2bps. Oil (-1.48%) is edging lower too on growth concerns.

After last week’s meltdown in crypto markets, Bitcoin is back at above $30k this morning – a jump since the lows of nearly $26k last Thursday but way short of the $38k it traded at in the beginning of the month and $68k early last November. The infamous TerraUSD, the stablecoin that fuelled the crypto slide, is at $0.18. It is supposed to trade at $1 at all times.

Looking forward now and there's not a standout event to focus on this week but they'll be plenty to keep us all occupied. US retail sales (tomorrow) looks like the highlight alongside Powell's speech the same day. There will also be US housing data smattered across the week and UK and Japanese inflation on Wednesday and Friday respectively.

Let's start with US retail sales as it will be a good early guide for Q2 GDP. Our US economists are anticipating a +1.7% print, up from +0.7% in March. Rebounding auto sales should help the headline number. For more on the consumer, Brett Ryan put out this chartbook last week on the US consumer (link here). US industrial production is out the same day.

We have a long list of central bank speakers this week headed by Powell and Lagarde (tomorrow) and BoE Bailey today. There are many more spread across the week and you can see the list in the day by day event list at the end. We do have the last ECB meeting minutes on Thursday but the subsequent push towards a July hike might make these quite dated.

US housing will be a big focus next week. It's probably too early for the highest mortgage rates since 2009 to kick in but with these rates around 220bps higher YTD, some damage will surely soon be done after the highest YoY price appreciation outside of an immediate post WWII bounce, in our 120 year plus housing database. On this we will see the NAHB housing market index (tomorrow), April’s US building permits and housing starts (Wednesday), and existing home sales (Thursday).

Turning to corporate earnings, it will be another quiet week after 457 of the S&P 500 companies and 368 of the STOXX 600 companies have reported earnings this season so far. Yet, it will be an important one to gauge how the US consumer is faring amid inflation at multi-decade highs, including reports such as Walmart, Home Depot (tomorrow), Target and TJX (Wednesday). Results will also be due from China's key tech and ecommerce companies like JD.com (tomorrow), Tencent (Wednesday) and Xiaomi (Thursday). Other notable corporate reporters will include Cisco (Wednesday), Applied Materials, Palo Alto Networks (Thursday) and Deere (Friday).

A quick recap of last week’s markets now. Fears that global growth would slow due to the tightening task at hand for central banks sent ripples across markets, without a clear specific catalyst. Equities declined, credit spreads widened, the dollar rallied, and sovereign yields declined.

The S&P 500 fell for the sixth consecutive week for the first time since 2011, falling -13.0% over that time. Even with a +2.39% rally on Friday, it fell -2.41% last week. Large cap technology firms underperformed, with the NASDAQ falling -2.80% (+3.82% Friday), while the FANG+ index fell -3.48% (+5.45% Friday). Volatility was elevated, with the Vix closing above 30 for 6 straight days for the first time since immediately following the invasion, narrowly avoiding a 7th straight day above 30 by closing the week at 28.8. European equities outperformed, with the STOXX 600 climbing +0.83% after a banner +2.14% gain Friday. The Itraxx crossover ended the week at 446bps, its widest level since June 2020. Crypto assets sharply declined, with Bitcoin down -12.51% and Coinbase -34.58% over the week, with a number of so-called ‘stablecoins’ breaking their pledged parity, forcing some to stop trading.

The growth fears drove a flight to quality. The dollar index increased +0.87% (-0.27% Friday) to its highest levels since 2002. Only the yen outperformed the US dollar in the G10 space. Sovereign yields rallied significantly, with 10yr Treasuries, bunds, and gilts falling -19.3bps (+8.5bps Friday), -23.0bps (+6.2bps Friday), and -28.7bps (+4.7bps Friday), respectively.

Reports that the EU was considering softening their oil-related sanctions due to member resistance combined with growth fears to send oil prices much lower at the beginning of the week, with Brent crude futures almost breaking $100/bbl. When all was said and done, a gradual rally over the back half of the week saw Brent merely -1.04% lower (+3.82% Friday). On the back of disappointing data from China it is down -1.48% this morning.

There was a lot of high-profile central bank speak to work through, as there will be this week. The main takeaways included Fed officials aligning behind a series of +50bp hikes the next few meetings, downplaying the chances of +75bp hikes until September at the earliest. Meanwhile, momentum in the ECB is growing toward a July policy rate hike, with policy rates breaching positive territory by the end of the year.

In terms of data Friday, the University of Michigan survey of inflation expectations for the next five years was unchanged at 3 percent, though inflation has weighed on consumers’ perception of the current situation.

Disclosure: Copyright ©2009-2022 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies every ...

more