(Click on image to enlarge)

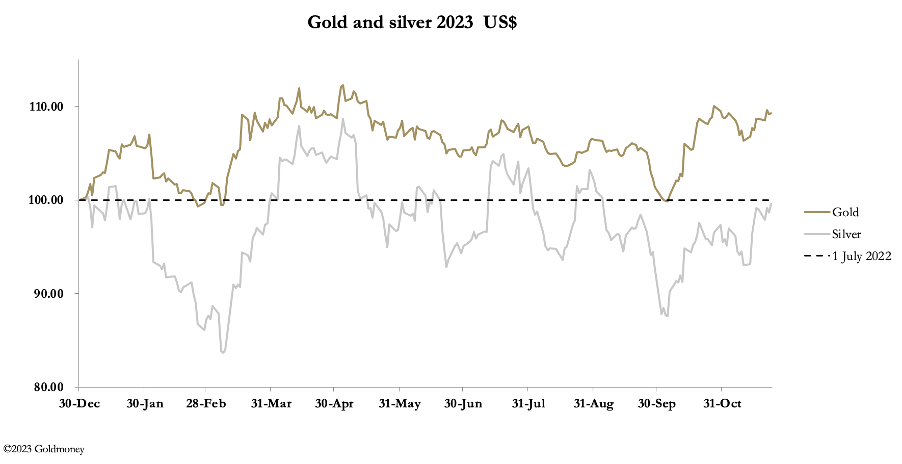

Ahead of a possible challenge on the $2000 level, gold consolidated recent rises this week, and silver held up well. This morning in European trade, gold was $1995, up $15 from last Friday’s close, and silver was $23.70, unchanged on the week. Comex volumes were healthy, despite the Thanksgiving holiday in the US.

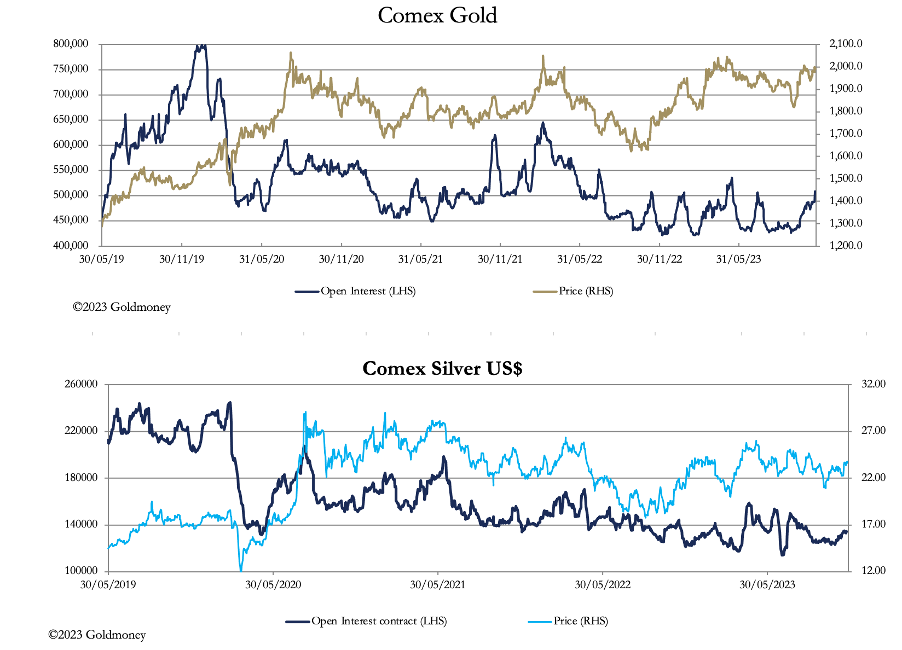

Open Interest in both Comex contracts is rising, as shown below.

(Click on image to enlarge)

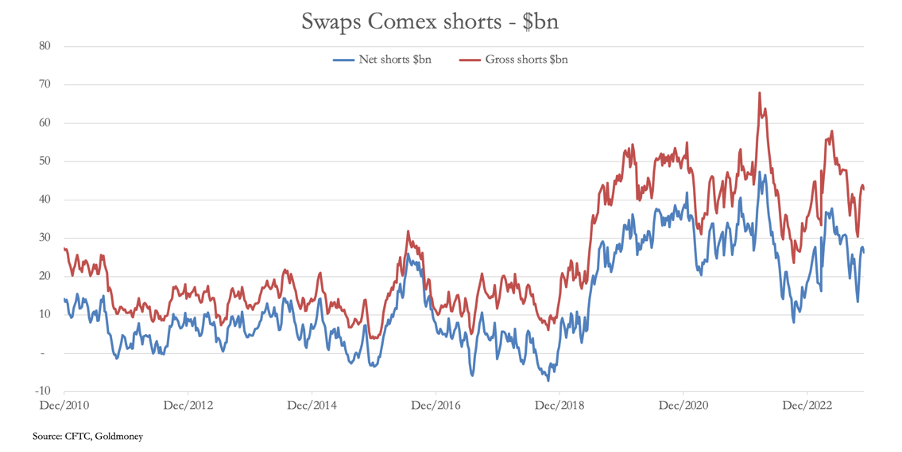

Gold’s OI is now over 500,000 contracts, which is putting pressure on the shorts, predominantly bullion bank trading desks, while silver still remains subdued. From the Commitment of Traders reports, the position of the gold swaps (mainly bullion banks) is shown below and reflects the developing squeeze on their positions.

(Click on image to enlarge)

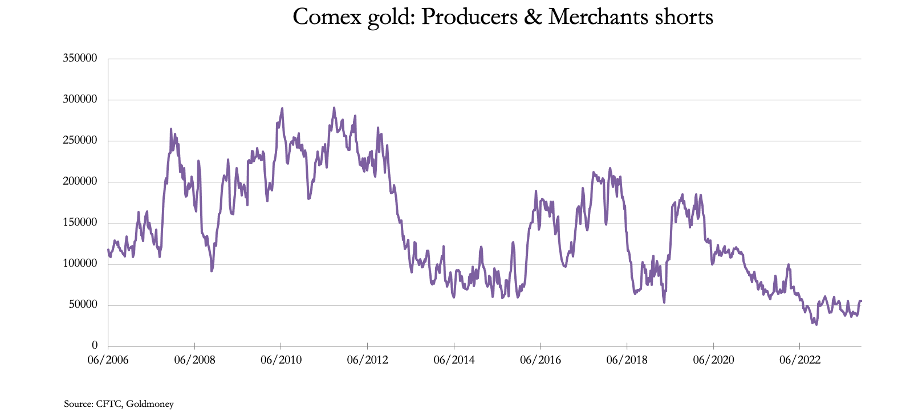

The Swaps have a problem. Their traditional target, hapless money managers, carries a smaller net long position than the Other Reported category, some of which are using Comex paper to secure delivery and is less susceptible to takedowns. Additionally, the Producer/Merchants category who hedge their future deliveries into the market by being net short has reduced its exposure significantly over time.

(Click on image to enlarge)

This throws responsibility for the short side onto the Swaps, compromising their ability to manage the price. There is now an increasing possibility that the Swaps will lose control of the gold price, bearing in mind that a convincing break above $2000 is likely to unleash a flood of long demand.

For the Swaps, the position in silver is precarious for other reasons including sheer lack of contract marketability. The Managed Money position is close to even, showing on balance their lack of interest. And the Swaps are similarly balanced — short less that 2,000 contracts net. Unlike in gold, the swing factor is mine hedging, either by silver producers or their banking representatives.

With silver’s volatility this is understandable. But if gold breaks above the $2000 level convincingly, will producers be so keen to sell their production forward? The juniors short on cash flow and needing finance have no option. But the larger profitable producers are likely to reduce or even cease their hedging activity.

Combined with the lack of market liquidity, the effect on the silver price could be explosive.

Underlying the market position in precious metals is the decline in the dollar’s trade-weighted index now that bond yields have eased. In the financial establishment, there will be sighs of relief all round, particularly at the Fed. The Fed has two urgent problems. The first is the funding program for a soaring US Government deficit, which is made virtually impossible when bonds are in a bear market. And fending off complaints by foreign central banks of the ruinous effects on their currencies and bonds of the Fed’s interest rate policies.

This new trend appears to be supporting gold, which has an eye on the inflationary implications. And foreign holders of dollars, faced with the opportunity of a rally in Treasuries and a fall in the dollar are likely to turn sellers of dollars in favour of gold.

More By This Author:

Is Gold About To Take Off?

Playing Into Putin’s Hands – Again

Calm Before The Storm

Comments

Log in or sign up to join the conversation.