International benchmark Brent crude oil traded cautiously on Thursday in Europe with the pullback seen earlier in the week clearly losing a little steam. Prices had risen quite sharply into October as the OPEC+ group of producers (the Organization of Petroleum Exporting Countries and allies) announced it would cut production by a collective two million barrels per day. Along with supply outages in Libya and planned stoppages in Norway, that was enough to see prices rally sharply from late September’s eight-month lows and, indeed, to eye the psychologically important $100/barrel level once again.

Recession Forecasts Put Demand In Spotlight

However, the market is fretting over likely fundamental demand as western economies strain under rampant inflation, depressed consumers, and widespread forecasts of either weak growth or outright recession. The situation is particularly acute in Europe, with the International Monetary Fund predicting this week that Germany could slip into recession in 2023.

Meanwhile, both OPEC and the US Energy Department have slashed their demand outlooks for this year, with the former citing in addition to high inflation the re-emergence of strict Covid containment measured in China. The latter now sees us consumption increasing by 0.9% next year, from a previously forecast 1.7%.

Weaker demand for crude is clearly boosting current inventories. If this trend becomes entrenched, and without significant drawdowns, it will only continue to weigh on prices. The next major scheduled event for the market will come later in the global day when the US Energy Information Administration releases its inventory data on both crude and refined-product stocks for the week ending October 7. Given the current pervasive gloom, it’s hard to imagine news of inventory builds coming as much of a shock.

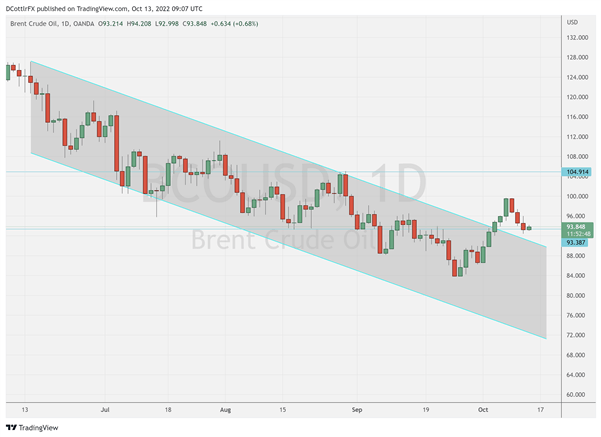

Brent Crude Oil Technical Analysis

(Click on image to enlarge)

Chart Prepared by David Cottle Using TradingView

Last week’s strong gains saw prices move significantly above the previously dominant downtrend channel which had previously been in place since June 9. However, bulls have failed to build a convincing platform from which to challenge the last significant high, August 29’s intraday peak of $105.026. They may yet have a chance to try again, but, if so, they can’t afford to see the market slide much from current levels. The markets seem current to be flirting with a cluster of support between $92.044 and $96.18 which is where it hovered between September 8 and 15. If it can consolidate here then the market may make another attempt at that August 29 top. However, the downward pressure on prices appears significant, with that downtrend channel likely to be reasserted on any daily close below $90.71. A bullish appetite to keep the market above that level as we head into this week’s close could well be key for short-term direction. Any slides below that level will put the significant lows of September 27 back in the bears’ sights.

More By This Author:

Nasdaq 100, S&P 500 And Dow Waver But End LowerS&P 500 Seesaws After Hawkish Fed Minutes, Stock Market Fate Tied To Inflation Data

EUR/USD Struggles As Markets Look To EU Energy Meet

Comments

Log in or sign up to join the conversation.