.webp)

Photo by Zlaťáky.cz on Unsplash

The growing dominance of passive investing has hit the mining industry harder than many observers assume. While active investors specifically seek out opportunities in individual stocks, in the passive world, capital only flows where indices and ETFs allow it to. Those not included in any fund remain in the shadows – often chronically undervalued, no matter how strong their fundamentals or prospects are.

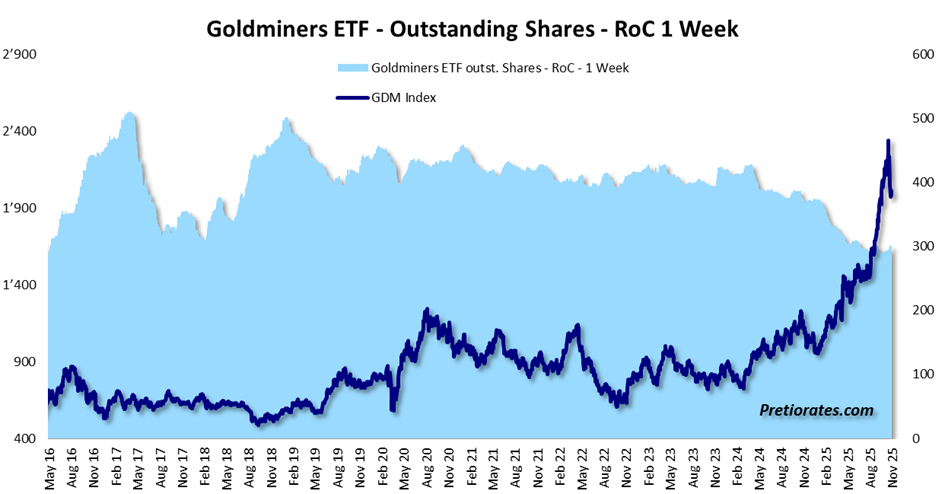

After years of stagnation, the mining industry has recently regained attention. With the rise in Gold and Silver prices, demand for mining stocks picked up. Since its low in spring 2024, the GDM Gold mining index has gained more than 170 percent – a spectacular recovery in less than two years. Nevertheless, the big money flow failed to materialize. The passive investment world, which now controls more than half of global investment volume, has ignored Gold mines. A look at outstanding ETF shares speaks volumes: despite rising prices, they have declined significantly. Apparently, many investors focused on physical metal rather than stocks – and after the sharp rise, many mining stocks are now likely to be considered «too expensive».

(Click on image to enlarge)

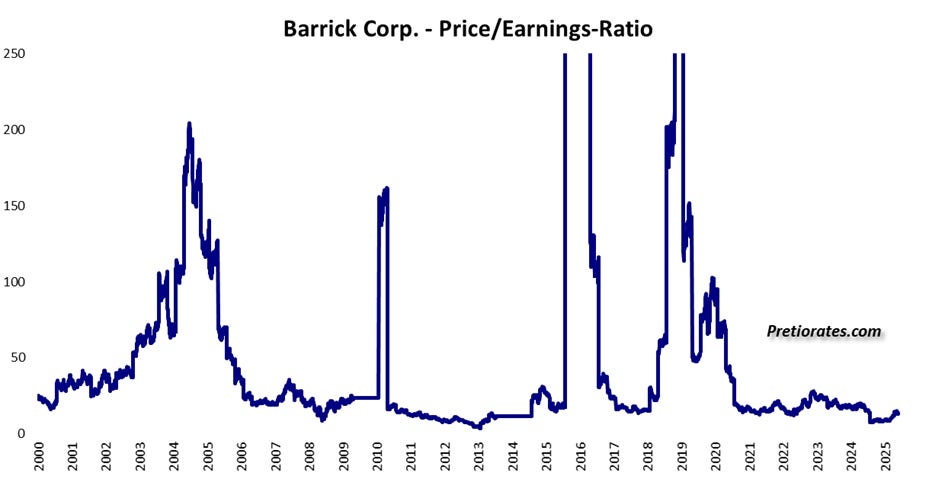

But this is precisely where the fallacy lies. Mining stocks work differently from traditional industrial stocks. They produce goods whose prices change daily – and with them margins, cash flows, and profits. This makes simple valuation metrics such as the price-earnings ratio unreliable. Value adjustments and price fluctuations distort profits and cause the P/E ratio to jump. A low ratio is no guarantee of a favorable valuation – it often simply signals high production costs, impending margin losses, or simply that the deposits have been exhausted.

(Click on image to enlarge)

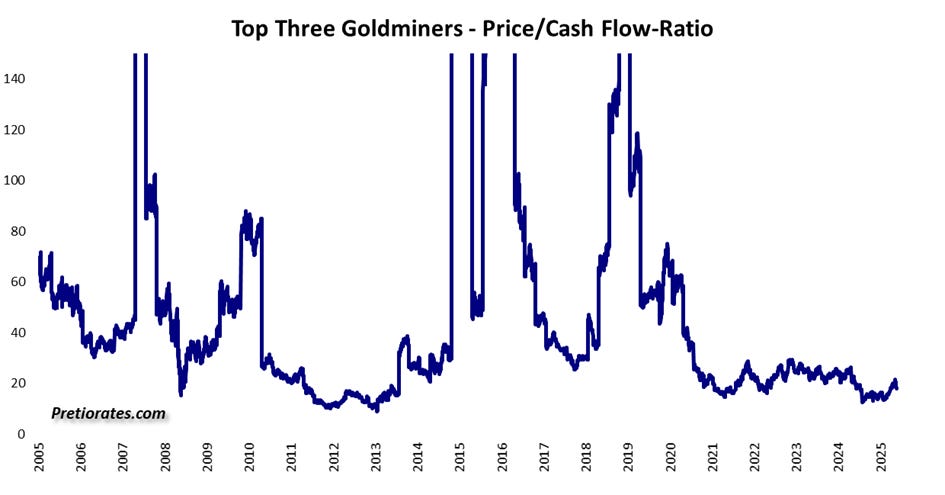

The price-to-cash flow ratio (P/CF) is more meaningful, as it excludes special balance sheet effects and value adjustments. It shows how much investors are willing to pay for a company’s actual cash flow – and thus whether Gold mining stocks are considered expensive or cheap in the market. If the price of Gold falls significantly, margins shrink and the ratio shoots up. Then the stocks appear expensive, even though their prices have usually already fallen noticeably.

It is interesting to note that the top three producers, such as Newmont (NEM), Agnico Eagle Mines (AEM), and Barrick (GOLD), continue to appear extremely cheap based on historical valuation metrics, despite significant price gains.

(Click on image to enlarge)

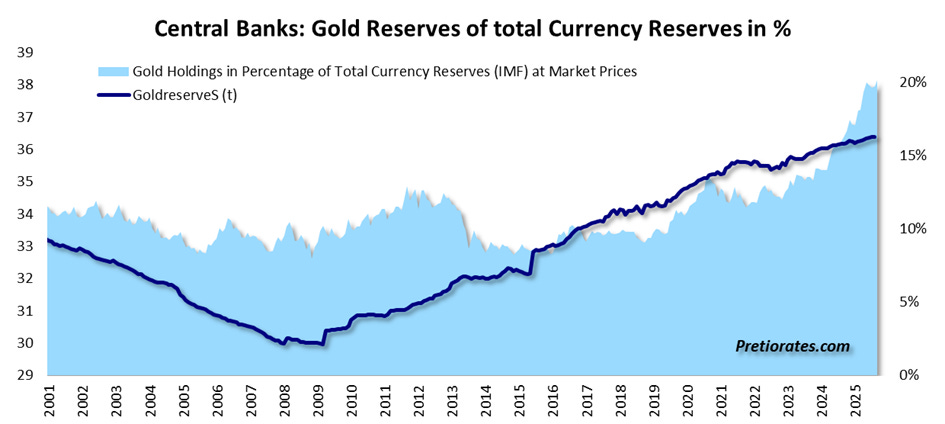

Central banks, on the other hand, continue to focus their interest on physical holdings. They have increased their Gold reserves from around 30,000 to over 36,000 tons over the past 15 years. Gold now accounts for around 20 percent of their balance sheets – a clear signal that precious metals are regaining importance in the global financial system.

(Click on image to enlarge)

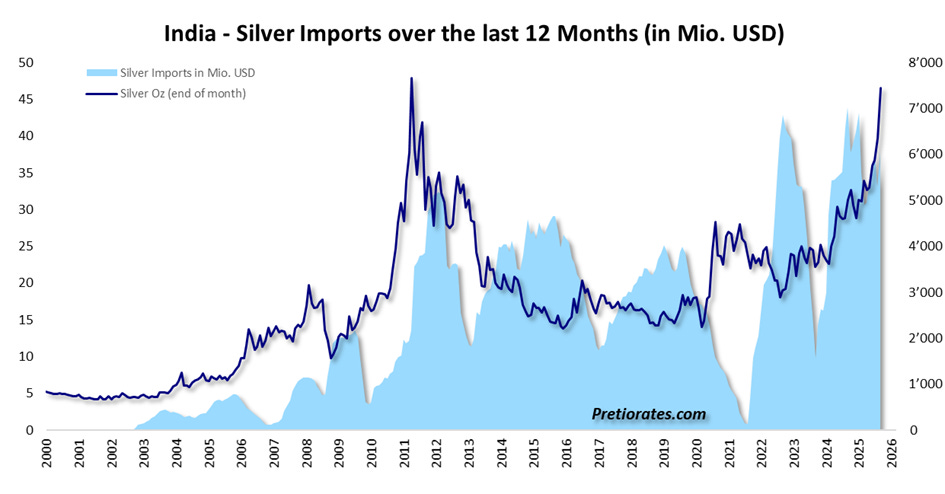

A recent report on the Indian central bank (RBI) caused quite a stir. It allegedly plans to allow Silver as collateral for bank and non-bank loans from April 2026 onwards – with a Silver-Gold ratio of 10 to 1. Silver would once again have the character of money for the RBI, but we find the ratio extremely exciting. Not at 80:1, which is the current ratio between Gold and Silver prices, but at 10. This means that Silver can be used as collateral in the Indian credit system at 10% of the price of Gold. Why should a borrower deposit Gold with the Indian central bank when they only have to deposit 10% of the equivalent value in Silver?

(Click on image to enlarge)

If the report in the Jerusalem Post proves to be true, India could import huge quantities of Silver in the future. The country has already significantly increased its purchases over the past years. And this could also be interpreted as a new chapter in the Silver market.

(Click on image to enlarge)

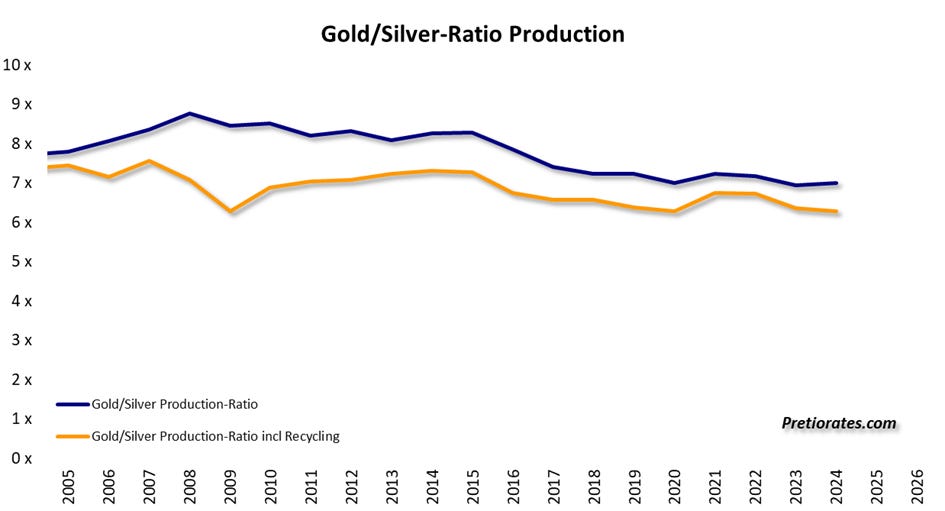

Even if the report proves to be premature, a closer ratio would be entirely plausible from a geological perspective. Silver is only about 15 to 20 times more abundant than Gold and is mined only about seven times more frequently – the current market ratio of more than 80 to 1 seems unsustainable.

(Click on image to enlarge)

More By This Author:

Don’t Be Emotional With Emotional AssetsThe Quiet Stories In The Base Metals Complex

Gold Shines And Silver Rocks

Comments

Log in or sign up to join the conversation.