AgMaster Report - Wednesday, March 29

MAY CORN

(Click on image to enlarge)

China has embarked on a very aggressive buying program – making Flash 8 am buys of US Corn 10 of the last 11 trading days – totaling over 3MMT – which has rallied the May Corn 40 cents (610-650)! We expect this buying frenzy to continue – as US Corn is very competitive in the South American Mkt! The major headwind in all commodities besides the inflation/IR fight by the Fed is the recent banking crisis – which has seen 2 US banks close – but that seems to have stabilized – and Corn has gone up regardless! The USDA Planting/Qtly Stks Mar 31 report this Friday should reflect 2.4 MA more than 2022! Arg/Brzl is about ¾ done! The Argentine drought has generally tightened carry-over – putting much pressure on the US!

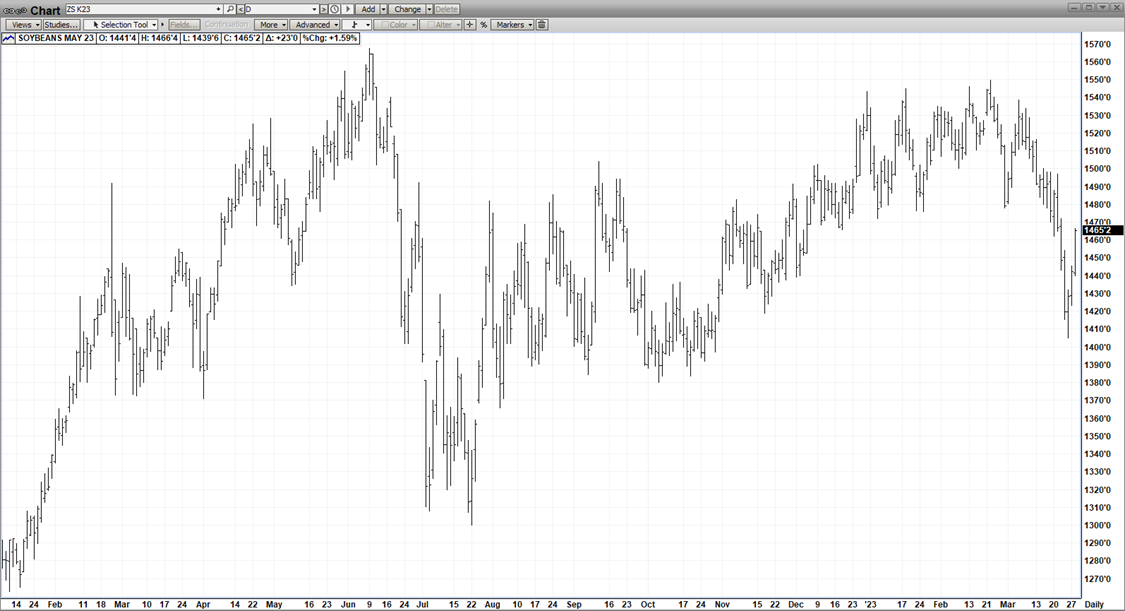

MAY BEANS

(Click on image to enlarge)

May Beans have been weighed down by “negative Macros” – including the INFLATION/IR conundrum faced by the Fed & the closure of 2 US banks in the past week! but in the last 3 days, the mkt has come alive – seemingly responding more to its own supply/demand fundamentals than the outsides! The result has been a stunning 60 cent rally 1405-1465! The mkt sees that Argentina has a half crop, that its 2023 acres are about the same as last year, that the US Growing season may begin with planting delays & that exports will improve! All of this with a back-drop of tighter – not more abundant – carryover stocks – will make bean futures very upward-sensitive to any US weather issues this coming growing season!

MAY WHT

(Click on image to enlarge)

Russia has basically owned the Wht Mkt in the past 4-5 months – inundating the global marketplace with very cheap exports from their record crop to help finance their war with Ukraine! But now, all of a sudden, they think wht is too cheap, globally & they’re talking about limiting exports or putting surcharges on them! That mentality – coupled with the ongoing uncertainty regarding the Russian-Ukraine Corridor Pact & substandard Winter Wheat ratings issued Mon – have a generated an impressive 40 cent rally (655-705) in May Wht! And the forecast acreage increase of 3.5 MA may not come to fruition – further enhancing the rally potential from today’s levels!

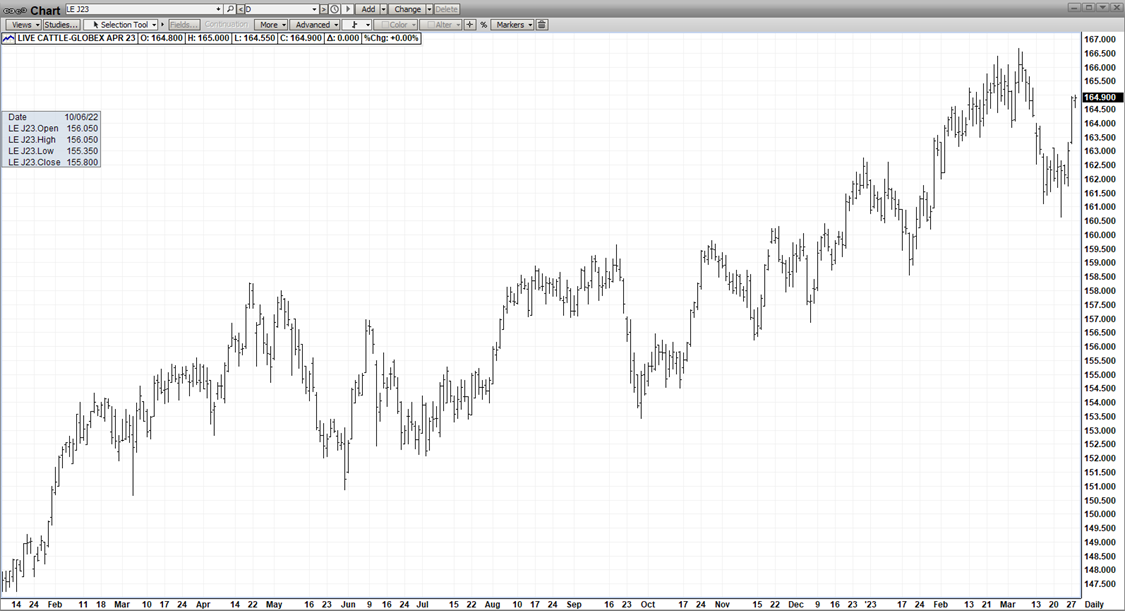

APL CAT

(Click on image to enlarge)

After correcting $6.00 (166.50 – 160.50), Apl Cat have come roaring back with a $4.50 rally – on the strength of lesser production & the onset of the Spring Barbeque Demand season! Beef production for the 2nd Qtr is expected to be down 6.2% from 2022 & also down 210 million pounds from the 1st Qtr – only the 2nd decline in the last 20 years! And the June cattle especially stands out – being a significant discount to cash & leaving a small upside gap on its daily chart! OLD BULL MKTS DIE HARD!

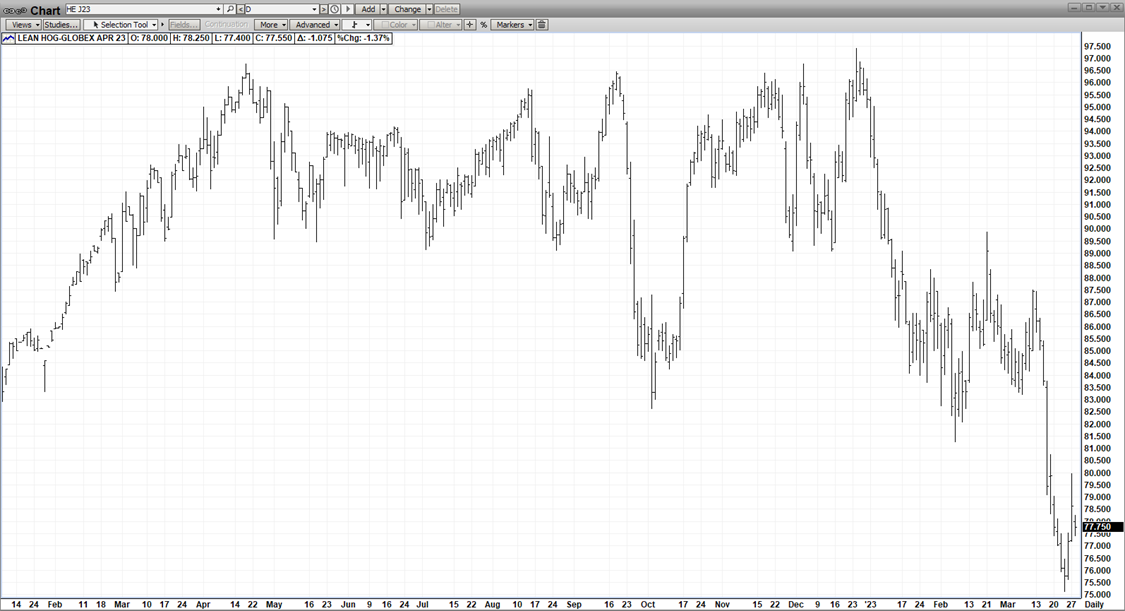

APL HOGS

(Click on image to enlarge)

Maybe this time! It looked for all the world that April Hogs spike low at 81.27 on 2/7 would hold but not to be! But the 75.12 spike on 3/23 appears to be the real deal – as the technicals are supported by solid fundamentals this time! Second Qtr production is due to be under 2022 & also 455 million pounds under the First Qtr – t75.1he 3rd largest drop in history! The mkt rallied $5.00 after hitting 75.12 last week! And the best demand period of the year is right around the corner! Roll out those grills!

On Thursday, the USDA will provide more info with a 2 pm release of the Qtly Pig crop Report – total hogs, kept for breeding & kept for mktg are expected to be about the same as a year ago!

More By This Author:

AgMaster Report - Tuesday, March 21AgMaster Report - Tuesday, March 14

AgMaster Report - Wednesday, Feb. 22