A Global Macro Look Back At Commodities In 2020

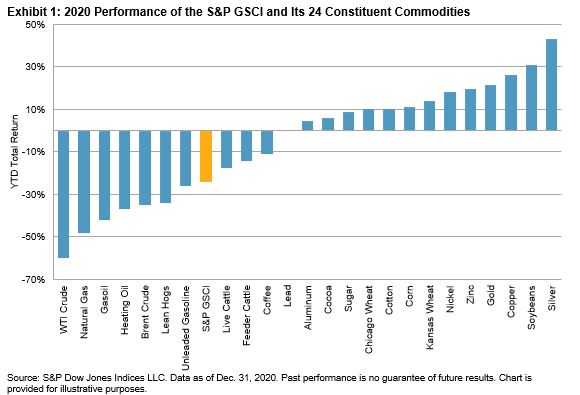

Over the past 50 years, commodities have displayed mostly positive yearly performances, as measured by the world-production-weighted S&P GSCI. The index rose in 34 out of those 50 years, or roughly 70% of the time. Usage as an inflation hedge coupled with its low correlation to other asset classes has given market participants ample reasons to fit commodities into investment portfolios. However, the past decade has been an exception. Commodities only rose four times during the 2010s, making it the worst decade for the asset class, with an annualized 10-year return of -8.65% for the S&P GSCI. In 2020, the S&P GSCI fell 24%, pulled down by the worst-performing energy commodities, as shown in Exhibit 1. Energy commodities make up over 60% of the index. The underperformance of livestock also negatively contributed, but not to the same degree.

(Click on image to enlarge)

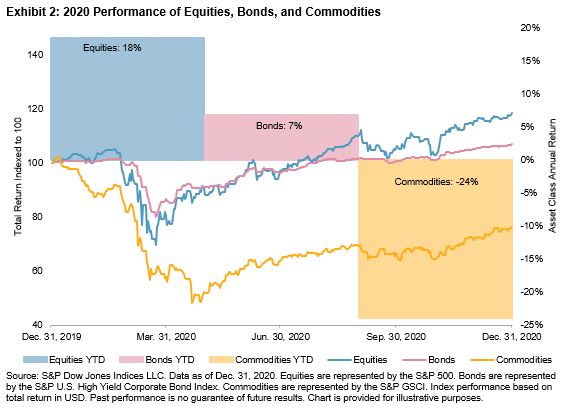

While other asset classes like equities and credit were able to jump back up quickly to their multi-year trends after the lows in March 2020, many commodities could not claw back out of the negative territory. This points to the unique property of commodities as a spot or real-time asset. Equities are a more anticipatory asset, looking ahead to the environment months or years into the future. Commodities tend to represent the current environment at a specific moment in time, represented by the nearby front-month futures contracts that make up the S&P GSCI. The current environment and outlook for commodities is uncertain; with increased concern about inflation, but no solid signs yet, we exited the recent disinflationary environment.

(Click on image to enlarge)

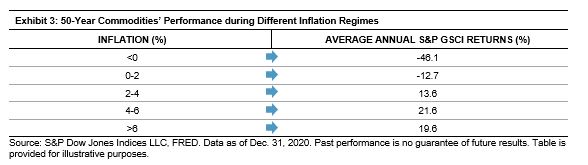

Historically, commodities have tended to do well during times of high inflation, as shown in Exhibit 3. We may be entering such an environment. Massive amounts of fiscal and monetary stimulus could lead to inflation. An outsized global economic recovery could inflate prices if demand explodes but production struggles to keep up. Higher costs to produce goods and rising wages could also be factors of inflation. After years without concern over inflation, market participants started adding inflation hedges to their portfolios in 2020.

(Click on image to enlarge)

The S&P GSCI seeks to offer market participants the chance to hedge against inflation, diversify a portfolio, or take a directional approach to the broad commodities market.

Disclaimer: Copyright © 2020 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. This material is reproduced with the prior written consent of S&P DJI. Please ...

more