The Fed was more hawkish than expected at its meeting which caused gold to sell off. However, interest rates moved lower, and the yield curve flattened. Both are positive developments for gold. Here are three gold miners worth buying on the dip: Pretium Resources (PVG), Newmont Corporation (NEM), and Wheaton Precious Metals (WPM).

After a brief period of outperformance vs. the major market averages, the precious metals complex has been hit hard again this week, with gold (GLD) down more than 5% for the week. This violent pullback is one of the worst we’ve seen in years, given its velocity. Fortunately, it’s provided a second opportunity to start positions in miners at very reasonable valuations. While the gold price falling $125/oz certainly doesn’t help margins for miners, it’s important to note that most miners are producing gold for less than $1,025/oz, still enjoying 40% plus margins at current gold prices. Let’s take a look at a few names that look compelling if this weakness continues:

The Gold Miners Index (GDX) is one way that investors can play the precious metals sector to gain leverage on gold. However, I prefer individual names since the index often has many laggards that can impede its overall performance, and it doesn’t pay a material dividend. Three names that look like standouts among their peers are Pretium Resources, Newmont Corporation, and Wheaton Precious Metals, with the latter two being clear leaders in their sub-sectors. All three of these miners differ in size and risk, but all three look like solid bets as sellers rush for the exits following the recent beatdown in the gold price. Let’s begin with WPM:

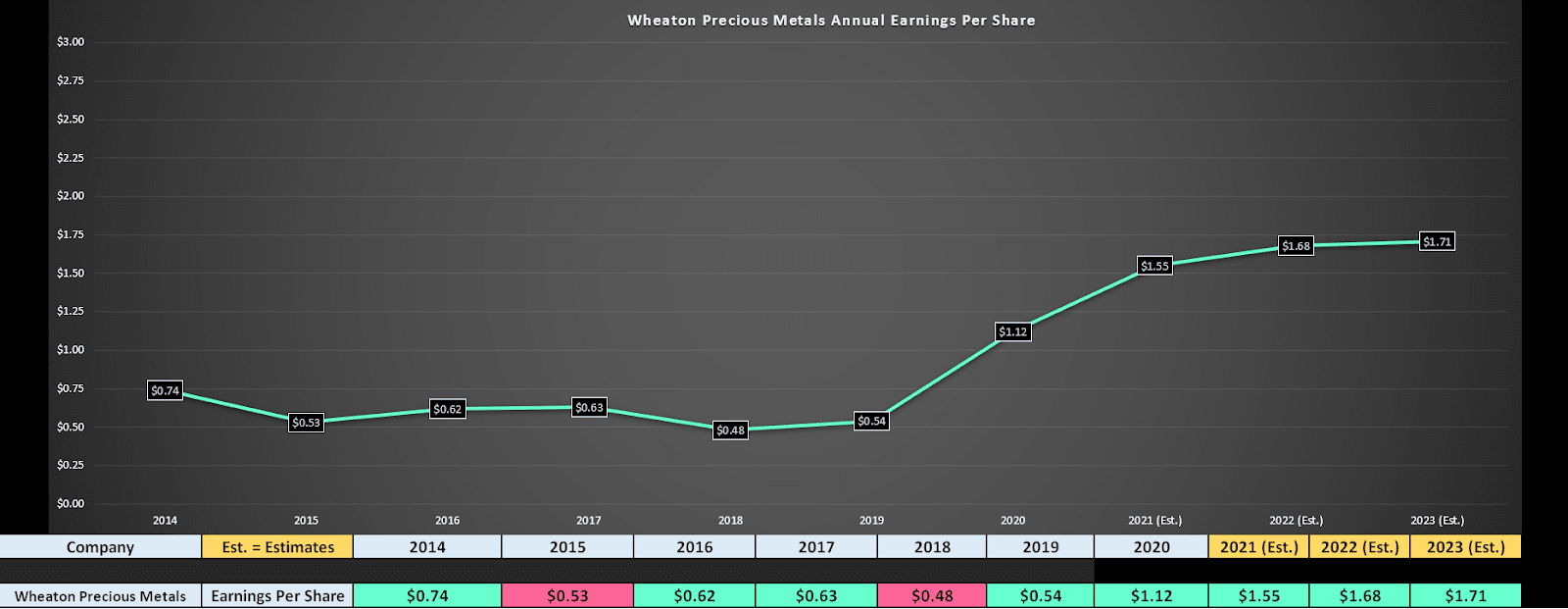

Wheaton Precious Metals is one of the largest royalty & streaming companies globally and is one of the lowest-risk ways to play the sector, given that the company has extremely high margins above 70%. Its business model of financing miners to build or expand their projects and then take a cut of their production is superior to most gold miners. This is because the company has diversified revenue across dozens of assets and significant upside as new royalties come online, or mines are extended past their initial expectations. The company just came off a strong quarter in Q1 from a financial standpoint with a record revenue of $324.1MM, with the company benefiting from a 13% increase in its gold sales price and a 53% increase in its silver sales price. This has set the company up for a year of significant annual earnings per share [EPS], especially as its mines ramp back up after what was a disrupted 2020 due to some temporary COVID-19 related shutdowns.

(Source: YCharts.com, Author’s Chart)

As shown in the chart above, WPM is set to increase annual EPS by more than 38% in FY2021 ($1.55 vs. $1.12), and this is after lapping triple-digit growth last year. At a current share price of $44.00, this leaves WPM trading at just 28x FY2021 earnings estimates and less than 26x FY2022 earnings estimates, a very reasonable valuation for a company with 70% plus margins and a low-risk business model. Currently, WPM’s peer Franco Nevada trades at more than 35x earnings, which is where larger precious metals royalty companies typically trade at fair value, with them appreciating to more than 40x during bull markets. If we use FY2022 annual EPS estimates and assign an earnings multiple of 35, WPM has significant upside with a fair value of $58.80, which assumes no further improvement in metals prices. Therefore, with the stock offering more than 30% upside to fair value, I would view any further weakness as a buying opportunity.

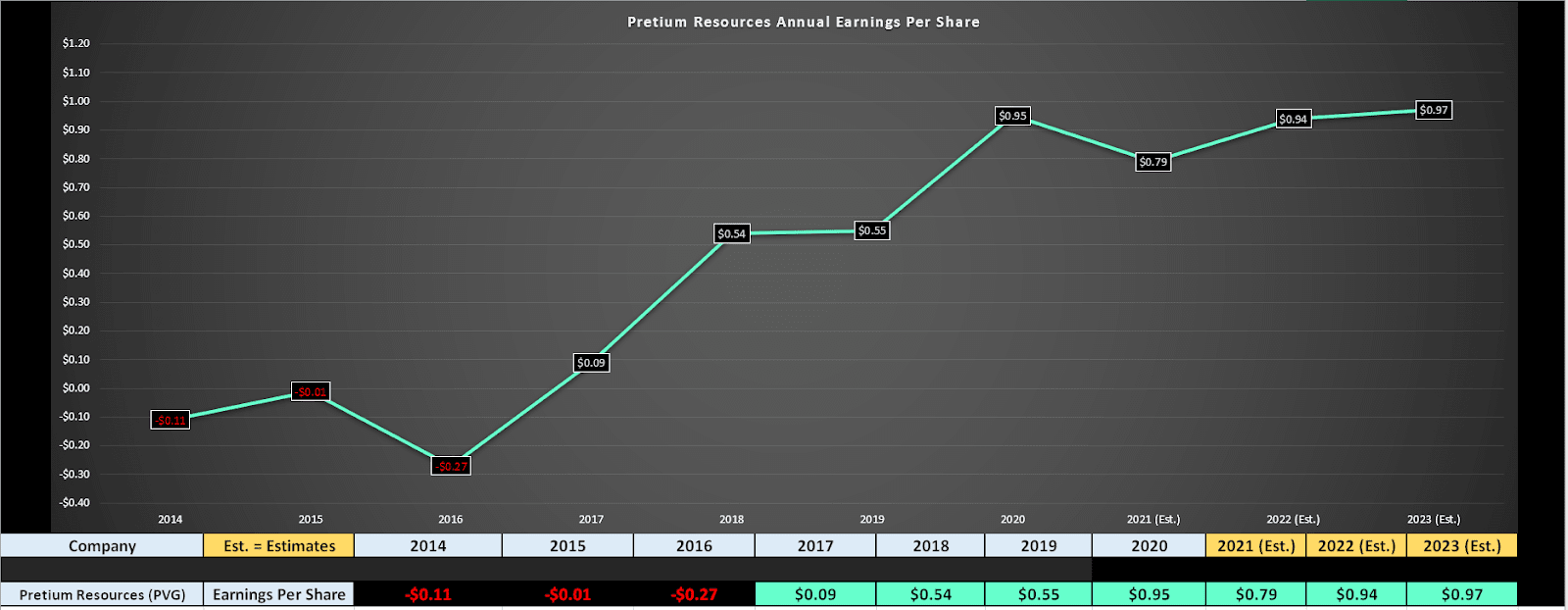

The second name on the list is Pretium Resources, a single-asset miner in Canada that is expected to produce just over 350,000 ounces of gold this year. The company released blockbuster drilling results this week, with four of its holes drilled, making the top-15 list for highest-grade intercepts in the sector over the past 18 months among all companies. The highlight hole was 19.5 meters of 306.6 grams per tonne gold and 15 meters of 561.6 grams per tonne, with these holes potentially adding another year of my life to the British Columbia Mine at higher grades. The important point about these results is that they lie less than 1 kilometer from the current mine infrastructure and come in at significantly higher grades than the current gold reserves held by PVG (~9.0 grams per tonne gold). So, assuming the company can prove up a resource here with further drilling, this could translate to a higher production rate once this area is developed.

(Source: YCharts.com, Author’s Chart)

Unfortunately, the stock picked the wrong week to release its news, and the stock has sold off sharply with the precious metals complex. However, at a current share price of $9.95, the stock is now trading at less than 11x FY2022 annual EPS estimates, which is a very reasonable valuation for a company with 45% margins even at current gold prices. Furthermore, assuming the company’s drill success continues, there’s no reason that Pretium couldn’t increase production to over 400,000 ounces going forward, and this would easily drive annual EPS to as high as $1.20 in FY2023/FY2024, depending on how long it takes to access this area. So, at barely 10x earnings, this looks like a low-risk area to start a position in the stock if it remains below $10.00.

The last name on the list is the sector juggernaut and the only gold miner in the S&P-500: Newmont. The benefit to owning Newmont is that it has more than a dozen mines and a more than 12-year reserve base, so investors have significant visibility into future earnings for the company and comfort that issues at any one mine won’t be magnified. NEM had a relatively soft quarter in Q1 with continued headwinds from COVID-19, but the company is set up for another strong year with annual EPS set to come in above $3.60. Looking ahead to the remainder of the year, NEM expects to see stronger operations as COVID-19 cases have dropped globally, and the company should also see its investments in innovation begin to pay off, with an autonomous haulage fleet purchased for its massive Boddington Mine in Australia. The ultimate goal is to implement these trucks at multiple mines, reducing the risk of labor inflation and increasing safety at its projects.

These plans, combined with lower costs as CAPEX comes down over the next few years, are expected to push NEM’s all-in sustaining cost margins up to $925/oz in FY2023, up from $730/oz last year. This would make NEM not only the largest producer globally but also one of the lowest-cost names. The other differentiator for NEM is that it pays one of the most generous dividends in the sector. The company currently pays $2.20 per share annually, with the potential for this to increase to $2.50 by year-end. This represents a yield of 3.50% at the current level, and at the higher level which isn’t unlikely, the yield climbs to nearly 4.00%.

(Source: YCharts.com, Author’s Chart)

As shown above, NEM is trading at just 17x FY2021 earnings estimates and closer to 16x FY2022 earnings estimates. For a company that’s diversified and has some of the largest mines globally and leads in innovation & technology, this is a very compelling valuation. The bonus, as noted, is that investors get a mix of growth and value here, with the company offering a 3.5% yield as well as a very reasonable valuation. Based on what I believe to be a fair earnings multiple of 20, I see a fair value for NEM closer to $79.60, or 25% above current levels.

There’s no question that the gold miners are out of vogue, with many high-flyers performing much better over the past year with inferior fundamentals, but the best time to buy, in my view, is when an asset class is hated, and the sentiment is poor. For the gold miners, this is the setup we’ve been presented with once again, with the group set to generate record-free cash flow this year and paying an average yield of 10%, with many names trading at double-digit free cash flow yields. For investors looking to get exposure, NEM and WPM look like two of the lowest-risk names to play the sector, with PVG offering leverage but with slightly higher risk.

Comments

Log in or sign up to join the conversation.