Market Analysis

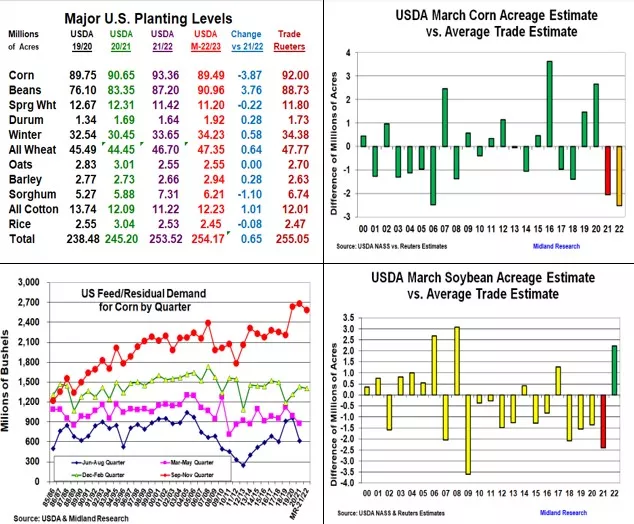

The USDA’s March US planting intentions again provide some fireworks while their quarterly stock levels were generally near expectations. With the market expecting lower corn plantings and larger soybean seedlings, 2022’s producer survey revealed even a larger drop in corn and a higher jump in soybean plantings than expectations. This year’s overall US wheat seedings were down from the trade’s estimate but remained 650,000 larger than 2021. Spring wheat was down while durum was up from 2022 levels. Prices initially rallied led by the corn, but soybeans' substantial 3.76 million jumps in acres vs 2021 tempered the CBOT with both beans and wheat ending sharply lower.

Corn’s 89.49 million survey level was 2.51 million below expectations & 3.87 million less than last year. This is the largest lower trade miss in records back 1989. 2.8 million of this decline occurred in the US Corn Belt. MN & ND had the highest declines of 600,000 & 500,000 acres while only MI & SD intentions were higher by 50,000 each. Higher fertilizer and other input costs were behind the survey’s results with soybeans generally picking up corn’s lower seedings.

Soybean’s hefty jump in US planting intentions was widespread. The W Midwest’s seedings may be up 1.3 million while the E Midwest reported a possible 1.22 million jump & the Mid-South’s plantings may rise 910,000 acres. Interestingly, the only major state with a lower seeding is ND, down 250,000. Even with an 88.73 million pre-report estimate, US soybean seedlings were 2.27 million higher than this level.

The USDA’s quarterly stocks were generally near the trade’s estimates. Soybean’s 1.93 billion March level was 20-30 million bu larger than the average, but this quarter’s 37 million lower residual matches soybeans moving into seed firms for processing. Corn’s 7.85 billion bu. stocks were only 27 million less than the trade’s estimate. This suggests last quarter’s feed demand was just 22 million less than last year. However, this week’s lower quarterly hog numbers keep us cautious about lower 2nd half feed demand. US wheat stocks were 20 million but below the trade average.

What’s Ahead:

The USDA’s 2022 planting intentions have dramatically changed the US corn & soybean planting ideas and their 2022/23 balance sheets. Weather in the Central US, the Black Sea, and Brazil’s Mato Grasso will all be important to CBOT prices in the next 45 days. The USDA will utilize these current plantings in their 2022/23 S&Ds, but no new-crop numbers until their May report. Hold sales for now.

Comments

Log in or sign up to join the conversation.