Image Source: Pixabay

Government borrowing and the national debt are barely getting a mention in the US election campaign, yet a failure to change trajectory risks further debt downgrades, more market volatility, and higher borrowing costs. This will pose economic headwinds, making it all the more challenging for the victor to achieve their manifesto goals.

Fiscal sustainability is being questioned

This year’s election is set against a backdrop where the government is borrowing the equivalent of 6% of GDP and the national debt totals $35tr. 24 years ago, the economy posted similar GDP growth rates to today and unemployment was also around the 4% mark, yet the US was running a fiscal surplus of 2% of GDP and debt stood at less than $6tr. The scale of deterioration in the US fiscal position is huge and failure to get to grips with the issue runs the risk of more debt downgrades, more market volatility, higher borrowing costs, and slower potential economic growth.

Looking ahead, the US’ fiscal position is vulnerable to both structural factors – e.g., an ageing population – and cyclical factors such as economic growth cooling, rising unemployment, and high borrowing costs. As Federal Reserve Chair Jerome Powell stated earlier this month, “the level of debt we have is completely sustainable but the path we are on is unsustainable”. So, what are the candidates saying about this and what do they plan to do?

Biden: more taxes, but more spending

President Joe Biden’s election tagline is “finish the job” and in March, he set out a plan to reduce the deficit by a cumulative $3tr over the next 10 years by “making the wealthy and big corporations pay their fair share and cutting wasteful spending on big pharma, big oil and special interests."

His economic policy mix includes the sunsetting of former president Trump’s 2017 Tax Cuts and Jobs Act (TCJA) income tax cuts, scheduled for 31 December 2025, plus implementing tax increases for businesses, high earners, and the super-rich – partially offset by more tax credits for some taxpayers. Spending activities will be focused on improving access and lowering costs related to healthcare, childcare, housing and education.

How ambitious Biden could be in a second term will be determined by how well the Democrats perform in Congressional elections. Should the Republicans retain control of the House of Representatives or win the Senate, major spending initiatives may be blocked and fiscal policy could end up being somewhat tighter assuming Trump's 2017 tax cuts do indeed sunset. This environment would likely mean the economy faces more headwinds, which would also help to slow inflation and give the Fed more scope to lower interest rates to a more neutral level more quickly.

Trump goes for growth, but likely accompanied by higher inflation and rates

Donald Trump’s position on the deficit has shifted since he first ran for president in 2016. Back then, the mantra was all about capping the debt and repaying money the country owes. In 2020 he blamed the Democrats for not helping pass spending cuts – but fast forward to today, and there is little mention of reining in the deficit. In fact, the 2024 GOP Platform document fails to mention the fiscal deficit or debt at all!

Should Trump win and Republicans sweep through Congress, the focus will be on a “second phase” of tax cuts in addition to an extension of the 2017 TCJA. This will involve sizeable tax cuts for corporations paid for by spending cuts/efficiency savings and tariffs placed on imported goods. Party officials are also of the view that tax cuts will more than pay for themselves by boosting the size of the economy and lifting revenues, even though the 2017 TCJA failed to achieve this.

Trade policy is the second major initiative. The imposition of 10% tariffs on all goods imports with 60% levies on Chinese-made products together with a four-year plan for phasing out Chinese imports of electronics, steel, and pharmaceuticals. These policies are designed to curb foreign competition, support US domestic manufacturing and employment with additional claims that this will boost national security. This will be accompanied by “de-regulation” aimed at promoting growth in relation to environmental, anti-trust, and energy.

Thirdly, there is the prospect of significant controls on net immigration involving more enforcement officers. Proposals also include the forced removal of undocumented workers. This could constrain labour force growth, and at the margin may add a little to wage pressures over the next four years.

Our sense is that this policy proposal mix from Trump could help to support domestic demand via the stimulus of tax cuts, but there are clear upside risks for inflation relative to Biden’s proposals. Tariffs and trade barriers will put up business costs, at least initially, while immigration controls may limit labor supply growth, posing additional challenges for corporate America. This stronger growth, and higher inflation environment is likely to mean monetary policy needs to be kept tighter than would otherwise be the case under Biden.

In this regard, we have already seen the Fed revise up its estimate of the neutral federal funds interest rate – believed to be neither expansionary nor contractionary for the economy – from 2.5% to 2.8%. We continue to see that as being too low, and under Trump’s policy mix we could see that “neutral rate” rise towards 3.25%. After all, if expansionary fiscal policy is providing more support for the economy, the Fed could justifiably feel that monetary policy needs to be tighter in order to achieve the 2% inflation target.

Should the Democrats retain control of the Senate, Trump will be forced to make concessions on key policy areas and his efforts to enact additional tax cuts and major immigration controls may be scuppered. Constrained by his ability to push his domestic priorities, Trump would likely focus on trade policy, where he has more autonomy. It would also coincide with a greater focus on foreign policy relating to Russia/Ukraine, China/Taiwan, and the Middle East/Israel as a means of exerting influence. This will have more significant economic implications for Europe, which we will address in another upcoming article.

Long-term challenges of the US budget

The legacy of huge fiscal transfers from the public sector to the private sector during the pandemic under the presidencies of both Trump and Biden has been the major factor responsible for the deterioration in government finances. That has abated, but even if the candidates were seriously motivated to shrink the deficit, there are major structural issues that make it difficult to get a real grip on the expenditure side of the equation.

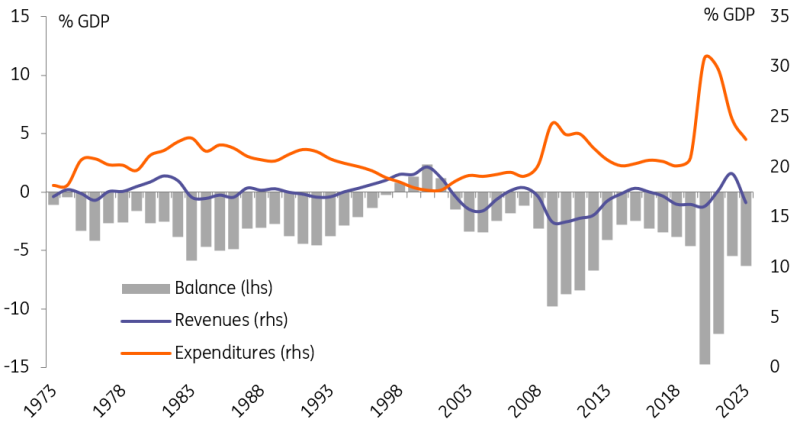

Government revenue, expenditure & budget balance (% of GDP)

Source: Congressional Budget Office, ING

Mandatory spending, or spending mandated by existing laws, represents nearly two-thirds of expenditure. It is predominantly healthcare and social security spending, largely determined by the number of recipients. It has been growing by 0.1-0.2pps as a share of GDP per year historically, driven by demographic trends.

In the past, the growing mandatory outlays were offset by shrinking discretionary spending (voted on in the annual appropriations process). The third and smallest component of government spending is interest expense. Having spiked by 0.5pps in 2023 due to higher interest rates, this reached 2.4% of GDP which is somewhat higher than the 50-year average of 2.0%.

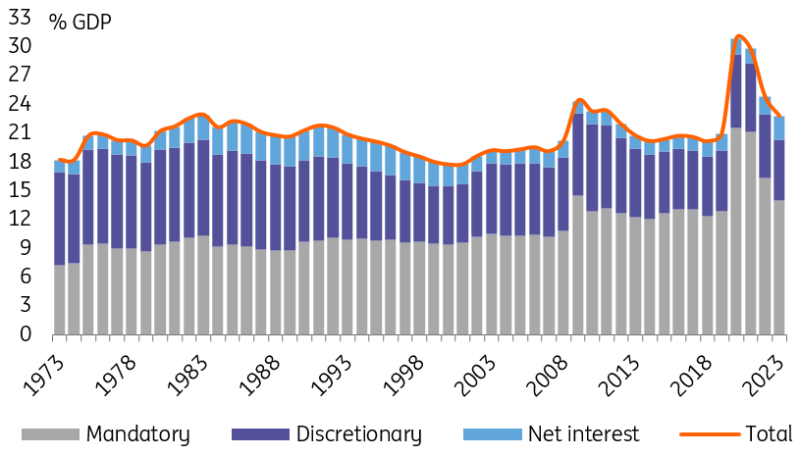

Components of government spending (% of GDP)

Source: Congressional Budget Office, ING

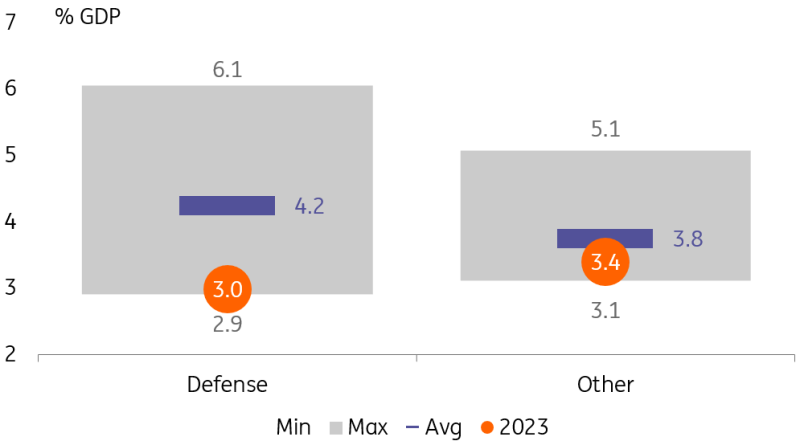

Digging deeper into the structure of discretionary spending, the chart below shows that it's already close to historical lows in relation to the size of the economy, especially on the defense side, which accounts for just under half of this component. That suggests limited room for reduction, especially given the higher demand for military equipment due to ongoing conflict in the Middle East and Eastern Europe. Non-defense discretionary spending includes federal education, transportation, housing programs, and homeland security amongst others. Cuts are possible, but as with defense, it would mean spending falls to the lowest share of the economy in 50 years.

Discretionary spending 1973-2023

Source: Congressional Budget Office, Macrobond

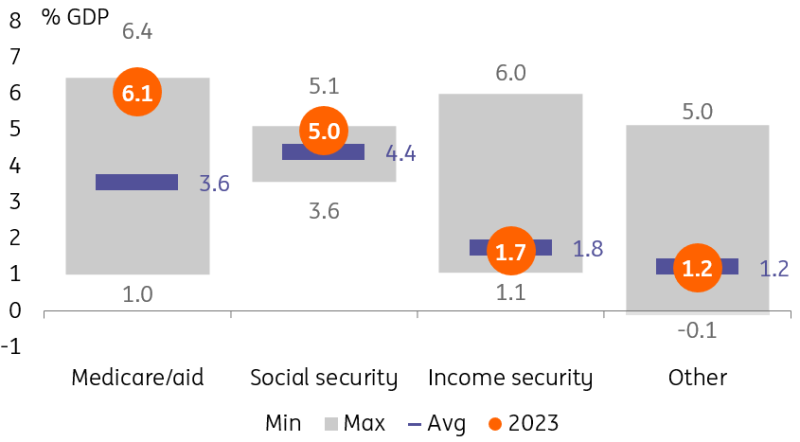

The components of mandatory spending tell the most important story. With the extra pandemic era support for households having ended, income security programs returned to normal in 2023, so there is little scope for further reduction and there is upside risk if unemployment rises. Meanwhile, the spending allocated for healthcare (Medicare/Medicaid) and social security is under structural upward pressure due to an ageing population.

Mandatory spending 1973-2023

Source: Congressional Budget Office, Macrobond

The conclusion is that there isn’t as much room to easily cut government spending as meaningfully as some campaign officials seem to appear to think.

Near-term outlook – CBO baseline

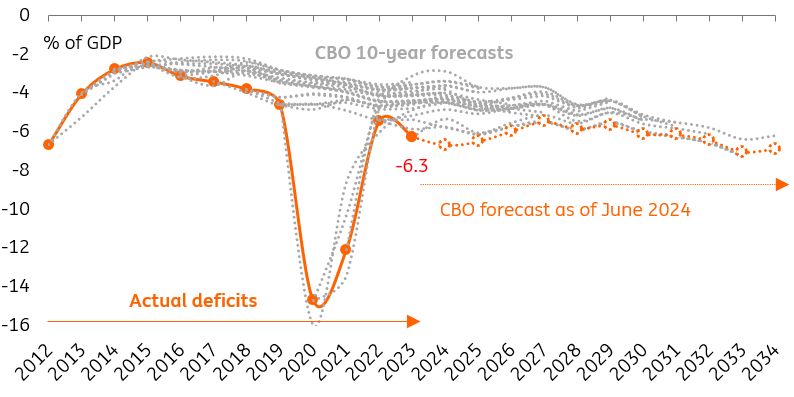

To set a benchmark of what these policies mean for the US fiscal position we look at the non-partisan Congressional Budget Office’s June projections of an average annual deficit of 6.3% of GDP over 2024-2034. This is 0.7pps wider than its February forecast, while public debt is projected to increase from 99% to 122% of GDP in the next 10 years.

US budget balance: actual and CBO 10-year projections

Source: Congressional Budget Office, ING

The CBO prediction is based on Trump’s TCJC tax reductions expiring with a solid economy seeing growth of around 1.8% on average, employment rising nine million over the period and incomes rising by five percentage points of GDP to 90%. It looks for expenditure to rise in the near term relating to international aid before demographically driven higher mandatory spending leads lifts government expenditure by 0.2 percentage points of GDP each year.

Implications of political scenarios

When judging where we stand with our projections versus those of the CBO, we have to look at both the direct fiscal policy decisions and then also our assumptions for economic conditions, including labor force growth, inflation, and interest rates.

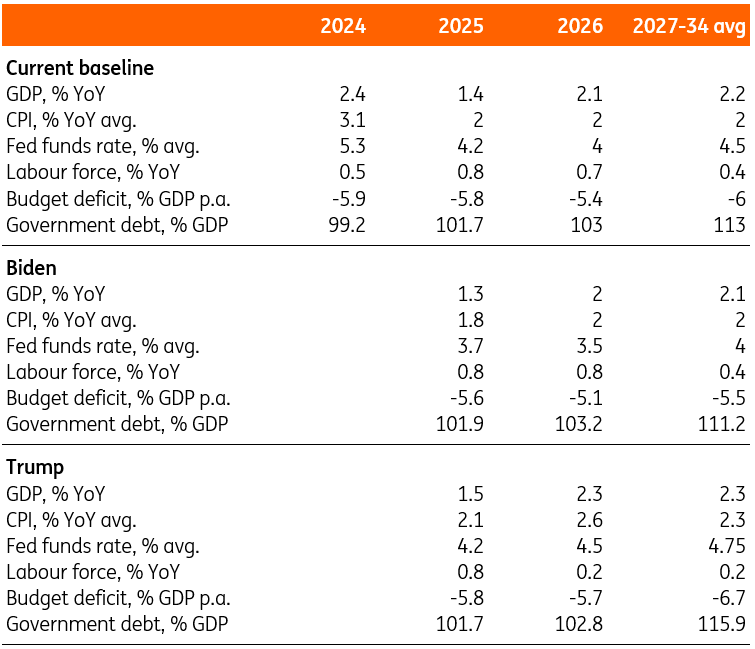

In terms of direct fiscal policy decisions, a Biden/Democratic administration is expected to let the 2017 tax reduction legislation lapse in the coming years, leading to a 0.5pp of GDP increase in the revenue collection in 2027 onwards, in line with the CBO baseline mentioned above. A Trump/Republican administration is more likely to extend the current tax subsidies, while its ability to limit spending growth will be constrained by the demographic trends dictating higher mandatory outlays.

The contrast in tax, trade, and immigration policy between Trump and Biden leads us to conclude that there will be stronger growth under a Trump presidency than Biden with higher inflation, thereby resulting in a stronger nominal GDP – the denominator in all the fiscal ratios.

The CBO’s recent sensitivity analysis suggests that the variation in the interest rate environment has potentially the biggest impact on the budget deficit scenarios. Each 10bp of deviation from the baseline results in around 0.1pps of GDP p.a. increase in the expected fiscal deficit over a 10-year period, due to higher expenses on debt servicing and other areas. In the near term we are expecting some sizeable falls in borrowing costs related to the long-anticipated Fed rate cutting cycle, and this contributes to lower fiscal deficits in 2025.

Our longer-term projections with a more inflationary environment under a Trump presidency could lead to a 75bp higher neutral Fed funds rate (3.25% versus the Fed’s previous 2.5% assumption) over the long run, which – assuming a proportional pass-through into the yield curve – could result in a 0.7-0.8pp GDP wider annual deficits compared to a Biden/Democrat administration.

Under both presidential candidates, the deficit will remain uncomfortably wide, with debt levels continuing to rise rapidly. However, the combination of direct decisions on tax policy and the macro conditions suggest that a Trump/Republican administration could lead to up to 1.2-1.3% GDP wider annual deficits starting in 2027 compared to a Biden/Democrat administration.

ING Forecasts under different scenarios (Full year average)

Source: ING

Implications for US Treasuries and markets

The US Treasury market is not currently being adversely impacted by extra supply being thrown at it from the higher deficit. The term premium implicit in the 10-year yield is close to zero, implicating little to no extra yield being paid to investors to encourage them to hold Treasuries. Simply put, the 10-year yield is being priced as an extrapolation of a rolling one-month T-bills exposure through the decade, with its path based off the fair value market discount for the Fed funds rate. A rolling 1-month T-bills exposure contains no price risk, while a 10-year Treasury holding comes with significant two-way price risk. Yet there is no compensation for that risk – which explains our argument that the market is not currently pricing in fiscal deficit pressure, at least not yet.

There are three reasons for this.

- First, we’re on the eve of a Fed rate cutting process. It’s not unusual for there to be a minimal term premium at this stage of the cycle, as the price risk is seen to be more biased to the upside, as typically long dated yields fall as the Fed cuts.

- Second, Treasury Secretary Janet Yellen has managed to curb the effect of the extra issuance by morphing the more significant increases towards shorter maturities, and away from longer maturities (in particular, away from 10 years and longer). The closer maturity issuances are to the Fed funds rate, less is the capacity for significant deviation from it.

- Third, there is a risk-on market theme out there with equities at record highs, implying the market believes there is little to worry about. That offers a comfort blanket of tranquility – but one that can easily be taken away.

Going forward, a lack of market concern on the size of the deficit can easily pivot to it being top of the list of worries. The transmission mechanism here is a few poor bond auctions that become a trend, requiring the build of a material new issue concession that gets built into structurally higher absolute yields. That could happen slowly, or it could be more abruptly. Our base is for a slow creep. But it’s an impactful one. We see the 10-year yield heading for 5% as a base case in 2025 in consequence. That sounds aggressive, as we barely and briefly touched 5% as the funds rate was rising in 2023 before falling away. But this time, we’re likely to get to that area in a more structural manner, where it would take either a deep recession or a systemic break for it to be coaxed back down.

In fact, a 5% 10-year yield call is a conservative one all things considered. It’s just a 100bp curve to a Fed funds rate that’s been cut to 4%. Under a Trump administration and on the assumption of a higher deficit than under a Biden administration, that 5% call easily becomes a 5% handle, meaning “5-point-something”. And it’s not inconceivable that that could round up to 6%. That said, we’re cognisant that a level like that sits above a generic BBB rate corporate yield curve today and any visit of 6%, if we got there, would therefore likely be fleeting. It would also be damaging for leveraged players of all guises, heightening recession and corporate default risk. That said, just because it’s damaging does not mean we can’t get there. A Biden administration could be better, but not by much. Remember we are currently in one.

While the fiscal deficit difference between the two candidates favours a Biden policy mix (lower than a Trump deficit), it’s not big enough to be materially impactful. Simplistically, we have a baseline view for a 5% 10-year yield and a 100bp curve from the funds rate out, which we feel is quite conservative given the size of the deficit, and broadly agnostic to the election outcome. If it’s a Trump administration, yields are likely to be higher and the curve steeper, but probably on a delta of no more than 50bp for the 10-year yield and the curve.

Market pressure to eventually refocus politicians’ minds

In the current environment, where markets are calm, politicians see little threat from the current trajectory of the US’ fiscal position. But that will quickly change if ratings agencies and markets start to see it as an issue. If markets become dysfunctional, it will force governments to take more rapid and painful action. That may not happen in the next four years – but as a minimum, the higher, steeper yield curve we expect will put up costs for households and businesses and prove a headwind for the economy more broadly.

More By This Author:

Rates Spark: Pricing Of ECB Cuts Facing LimitsFX Daily: Inflation Divergence Widens In G10

US Retailers Receive A Summer Boost

Comments

Log in or sign up to join the conversation.