Market Reaction

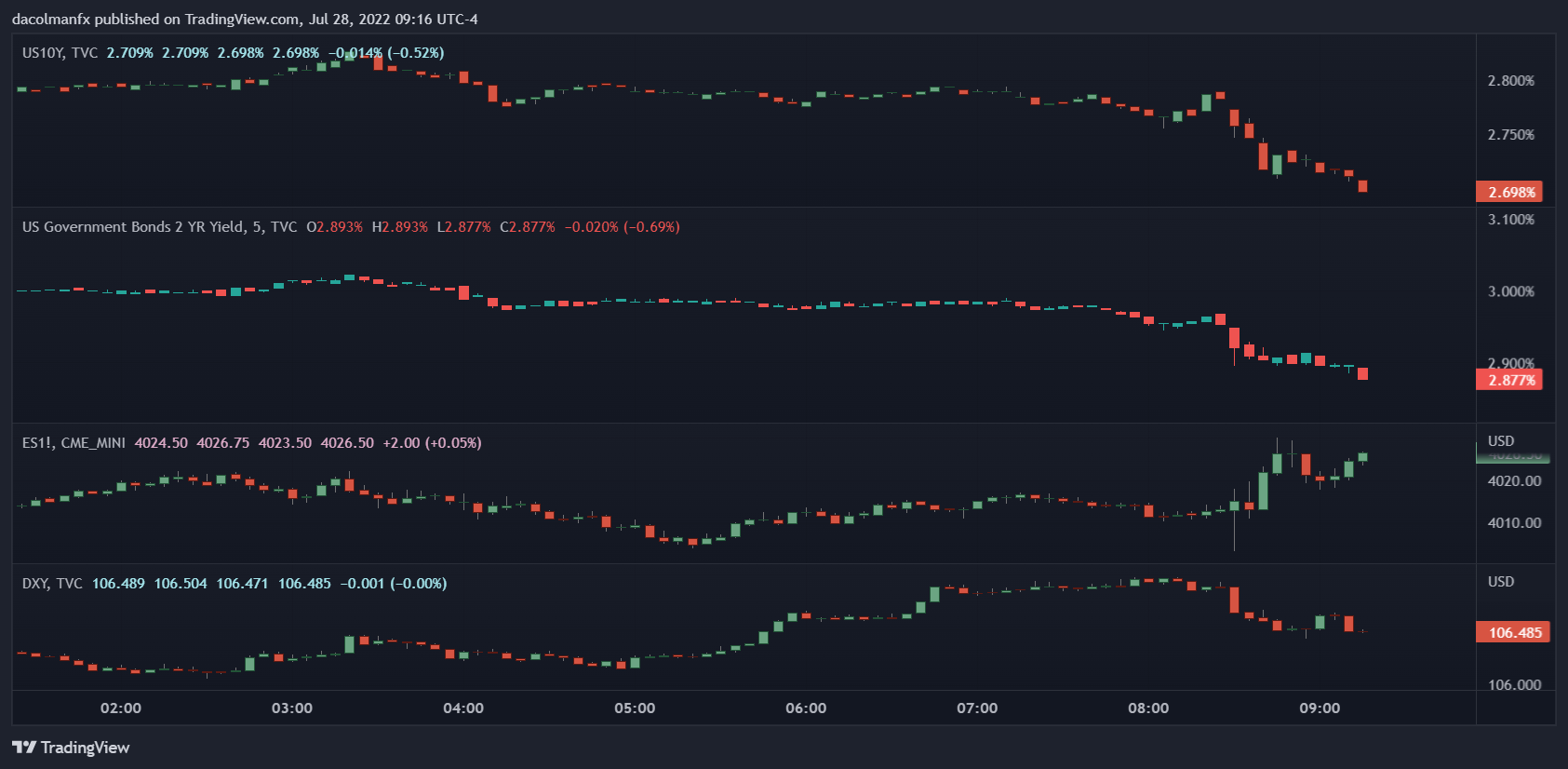

U.S. equity futures whiplashed but remained in negative territory after the U.S. GDP report was released. Meanwhile, Treasury yields declined across the curve on bets that rapidly weakening economic activity will prompt the Fed to embrace a less aggressive hiking cycle. Elsewhere, the U.S. dollar (DXY) trimmed its advance but held onto some of its early morning gains.

Rising risks of an economic downturn will likely lead to a central bank policy pivot later this year, provided inflation begins to cool meaningfully in the coming months. Against this backdrop, the U.S. dollar will have difficulties making fresh highs in the near term, signaling it may have peaked in July.

U.S. Treasury Yields, S&P 500 Futures, And DXY Chart

(Click on image to enlarge)

Source: TradingView

The U.S. economy failed to rebound and posted another contraction in the second quarter due to rapid cooling of household consumption and a steep drop in investment, a sign that the outlook continues to deteriorate amid mounting headwinds, including four-decade high inflation, and tightening financial conditions. According to the Commerce Department, gross domestic product, the broadest measure of goods and services produced by a nation, shrank 0.9% on an annualized basis, following a 1.6% drop during the first three months of the year. Analysts polled by Bloomberg were expecting a 0.4% increase in real GDP.

While two consecutive quarters of negative growth are informally considered a technical recession, the National Bureau of Economic Research (NBER) has a broader description. For the government agency in charge of officially declaring the beginning and end of economic downturns, a recession involves a significant decline in activity that is spread across the economy and lasts more than a few months. By this definition, the country may not yet be in one, especially given the strength of the labor market.

Looking under the hood for drivers, personal consumption expenditures rose by a modest 1.0% after a 1.8% increase in the previous quarter, indicating that consumer health is worsening hit by falling real income and weakening balance sheets amid rampant price pressures. To avoid a significant slump in output, consumption must stabilize in the coming months, bearing in mind that this variable represents approximately 70% of GDP.

Elsewhere, gross private domestic investment plummeted 13.5% partly in response to declining inventories and a 14% collapse in residential investment resulting from higher interest rates. With mortgage rates expected to remain high, the housing market is likely to cool further, preventing construction activity from staging a meaningful recovery. In this environment, residential investment will stay subdued.

On a brighter note, the external sector added 1.43 percentage points to economic growth over the past three months, as exports outpaced imports significantly, helping offset weakness in the investment component.

Last but not least, final sales to private domestic buyers, a measure of underlying demand that excludes trade, inventories, and government spending, stagnated after a 2.0% increase in the first quarter, suggesting that the macro outlook is becoming a little gloomier.

Although backward-looking, the disappointing GDP data is likely to reinforce fears that the U.S. economy is headed for a hard landing. However, there is a silver lining to the bad news. Deteriorating macroeconomic conditions may induce the Fed to adopt a less hawkish stance later this year, provided inflation begins to moderate. A monetary policy pivot, in turn, may help prevent a significant downturn, paving the way for an activity to stabilize and recover.

More By This Author:

AUD/USD Forecast: Can Aussie Get Up Above 0.70 After Retail Sales Miss?S&P 500 Rallies to Six-Week-Highs, US Dollar Sinks to Support on FOMC

Rand Dollar News: USD/ZAR Falls Below 17.00 Ahead of Fed Decision Day

Comments

Log in or sign up to join the conversation.