Photo by regularguy.eth on Unsplash

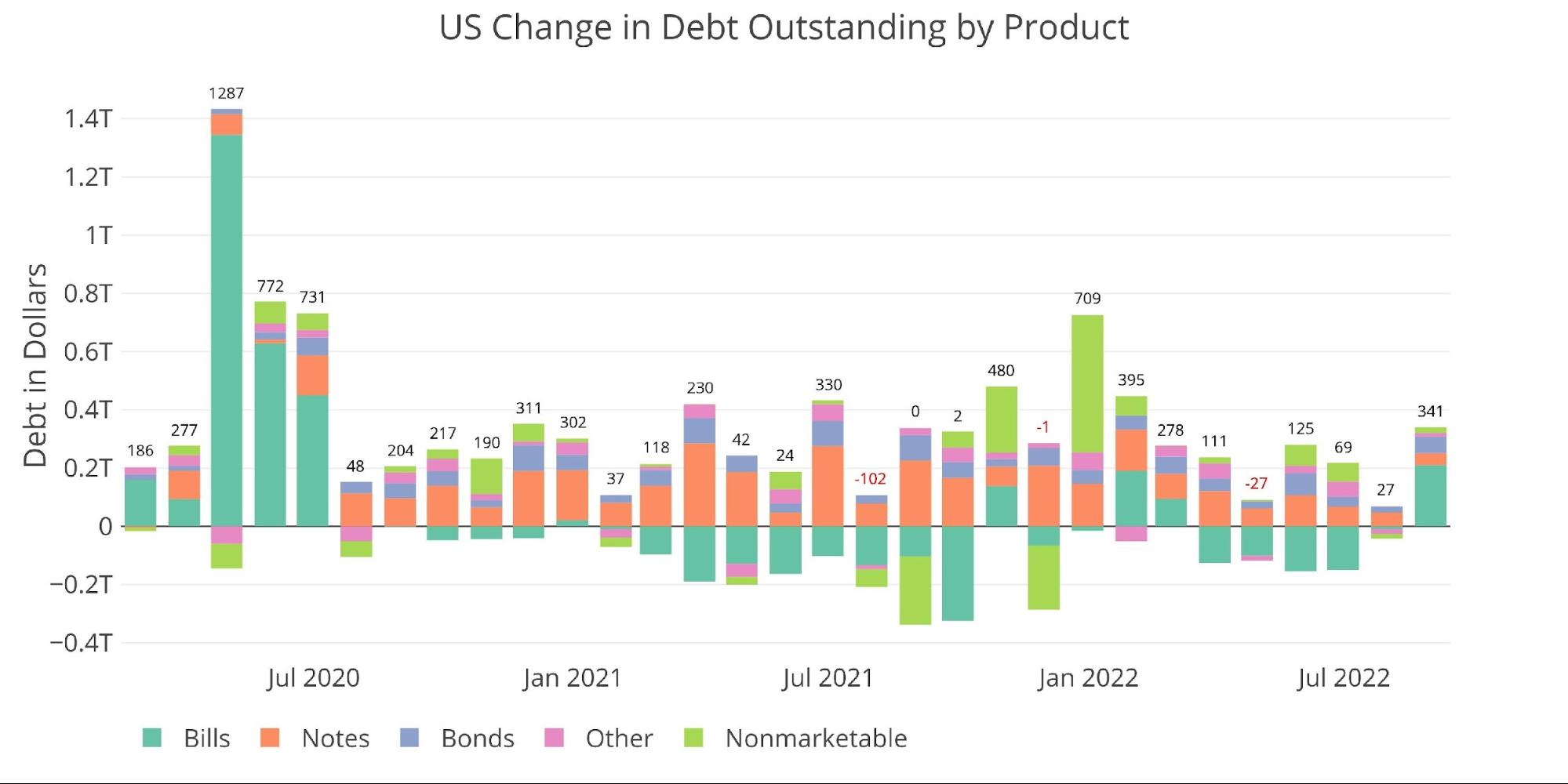

The Treasury added $341B of debt in August. This was the largest increase in the debt since January and is more than 10 times larger than the increase in July. Another major occurrence was the increase in short-term debt. The Treasury increased Bills by $210B, the largest increase since June 2020. This is a move that runs counter to the recent months where the Treasury has been actively decreasing short-term holdings.

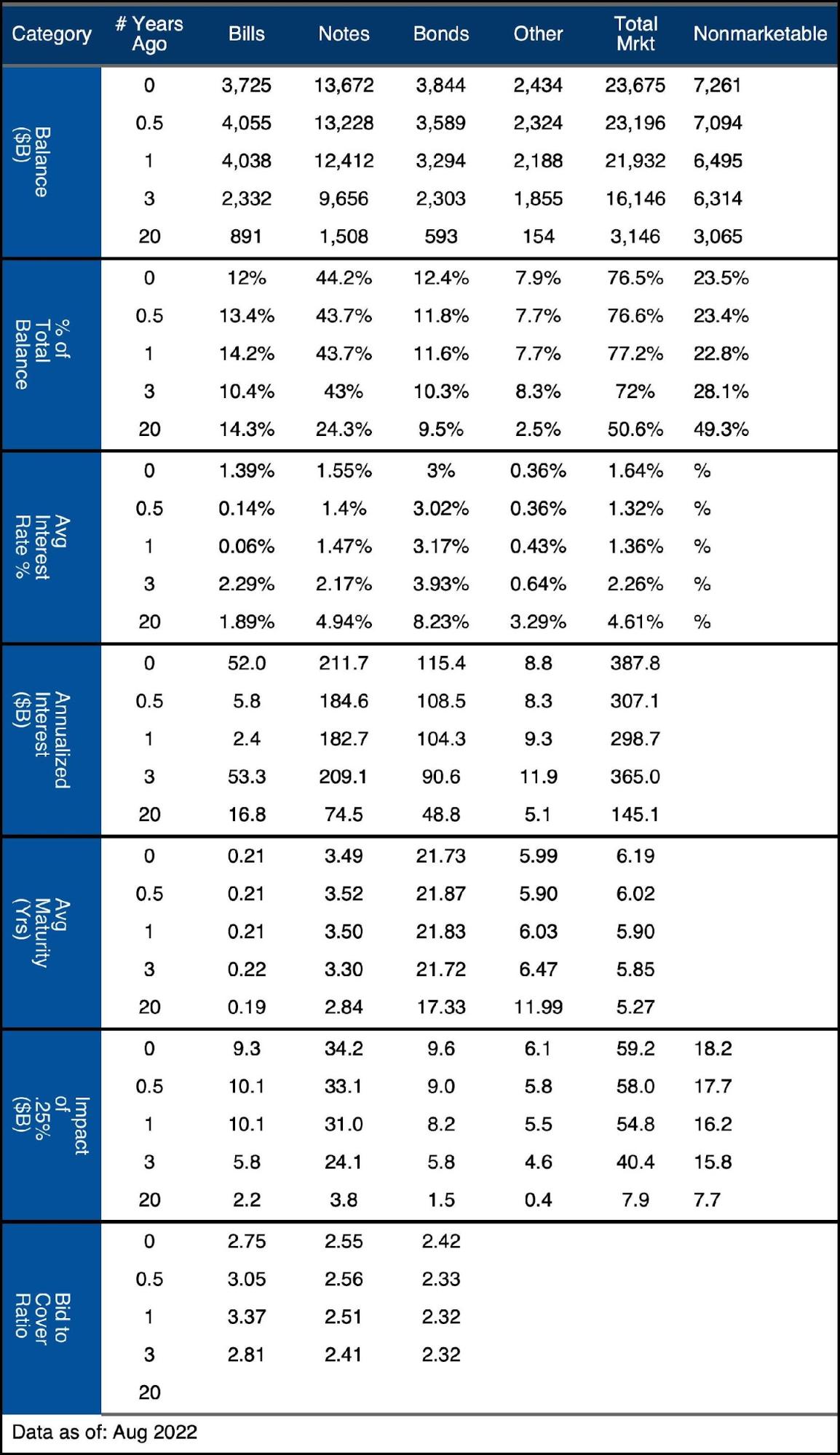

Note: Non-Marketable consists almost entirely of debt the government owes to itself (e.g., debt owed to Social Security or public retirement)

Figure: 1 Month Over Month change in Debt

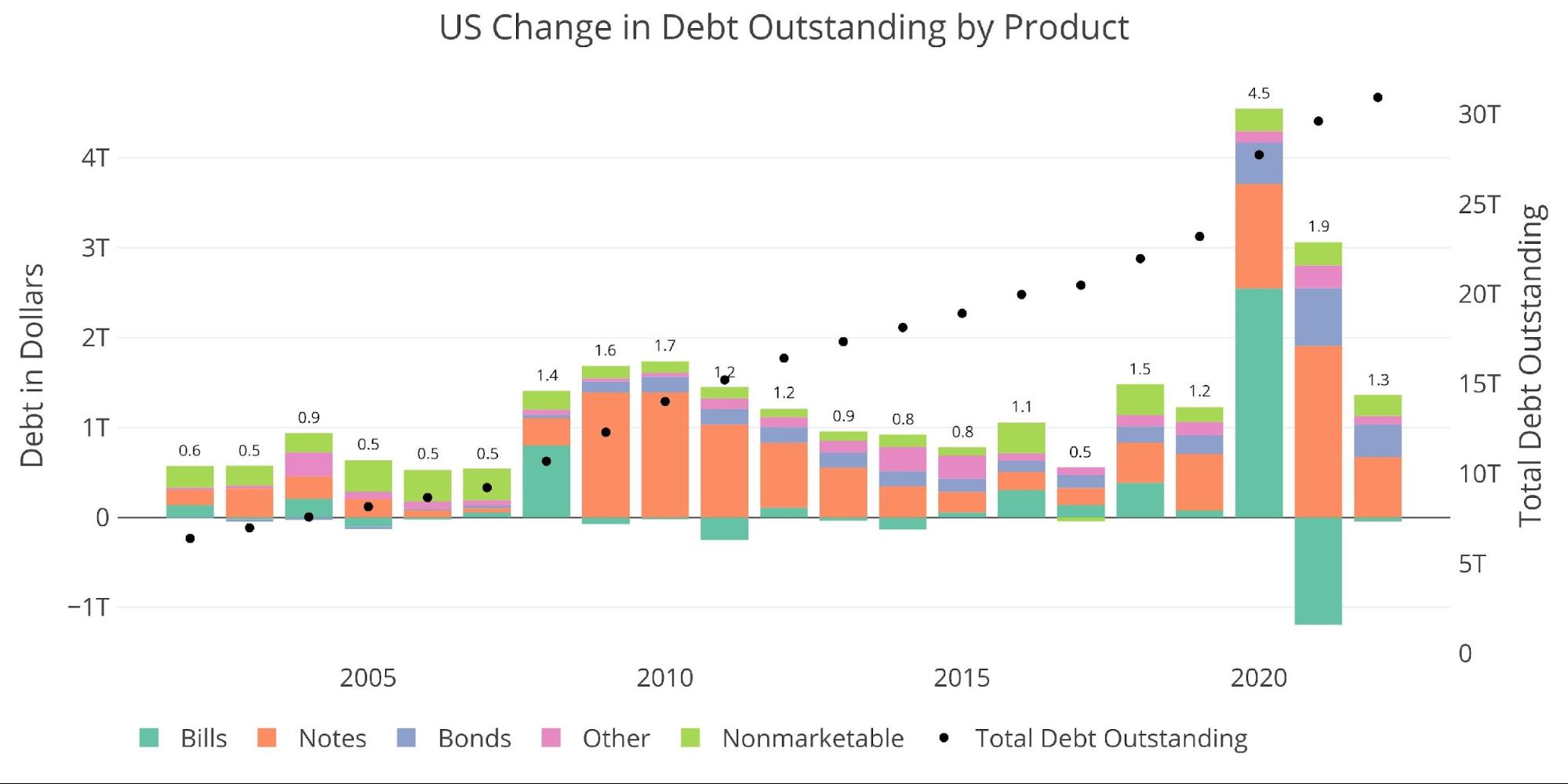

The recent surge in debt issuance pushes total US debt to $30.9T, up $1.3T so far this year.

Figure: 2 Year Over Year change in Debt

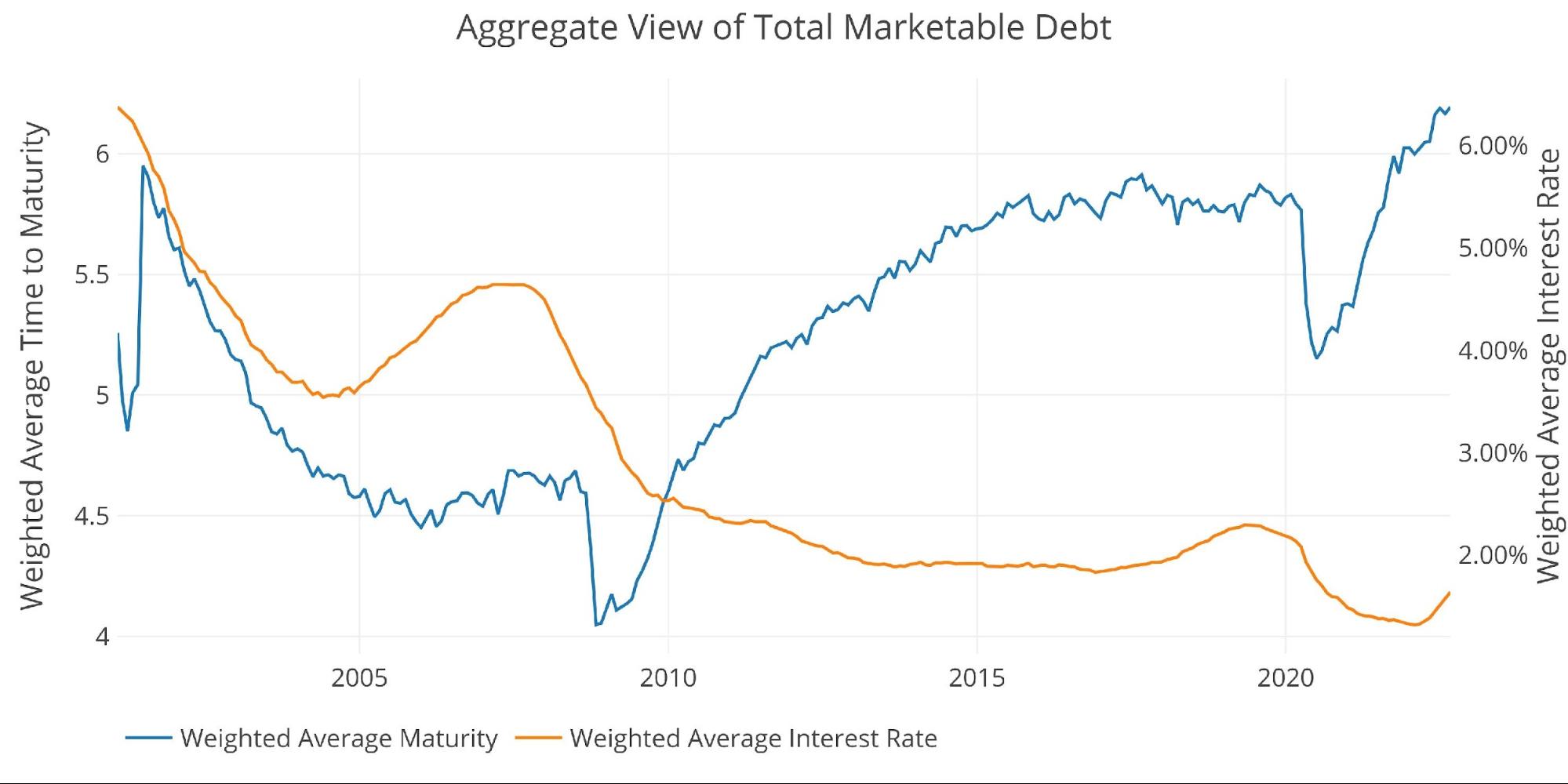

The recent conversion of short-term debt to long-term debt can be seen below as the Treasury has extended the average maturity of the debt to record highs. The current average maturity is 6.19 years, up from 5.76 just before Covid hit. The average maturity was at 5.15 at the depths of debt issuance in 2020, which was primarily short-term in nature.

Unfortunately, this has not prevented the interest on the debt from creeping up. The Fed hiking cycle has brought the weighted average interest rate up from 1.32% to 1.64%. 32bps may not sound like much, but on a $30.9T balance, that comes out to $99B! Furthermore, the rate increased by 9bps in the most recent month alone.

Figure: 3 Weighted Averages

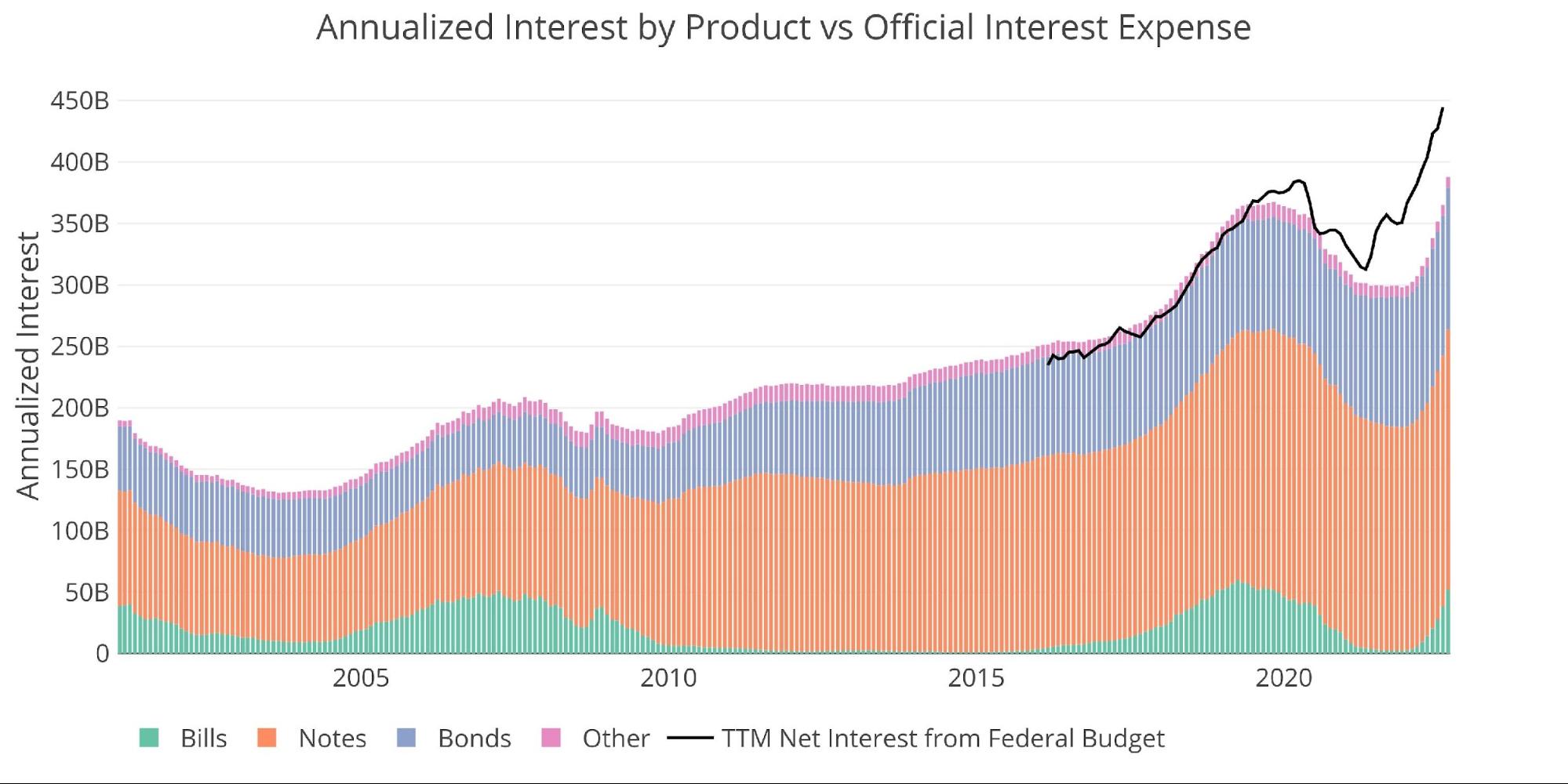

The chart below shows the impact of the higher interest rates. Interest on the marketable debt has reached a new all-time high of $388B. Even more concerning is the pace of the increase. In the last month alone, annualized interest increased by $22B! This pace of increase is completely unsustainable for the US Treasury!

The black line shows the interest as calculated by the Federal budget due out next week (below is through July). This will include other interest charges beyond Marketable debt such as the newly popular I-Bonds, which is doling out interest above 9%!

Figure: 4 Net Interest Expense

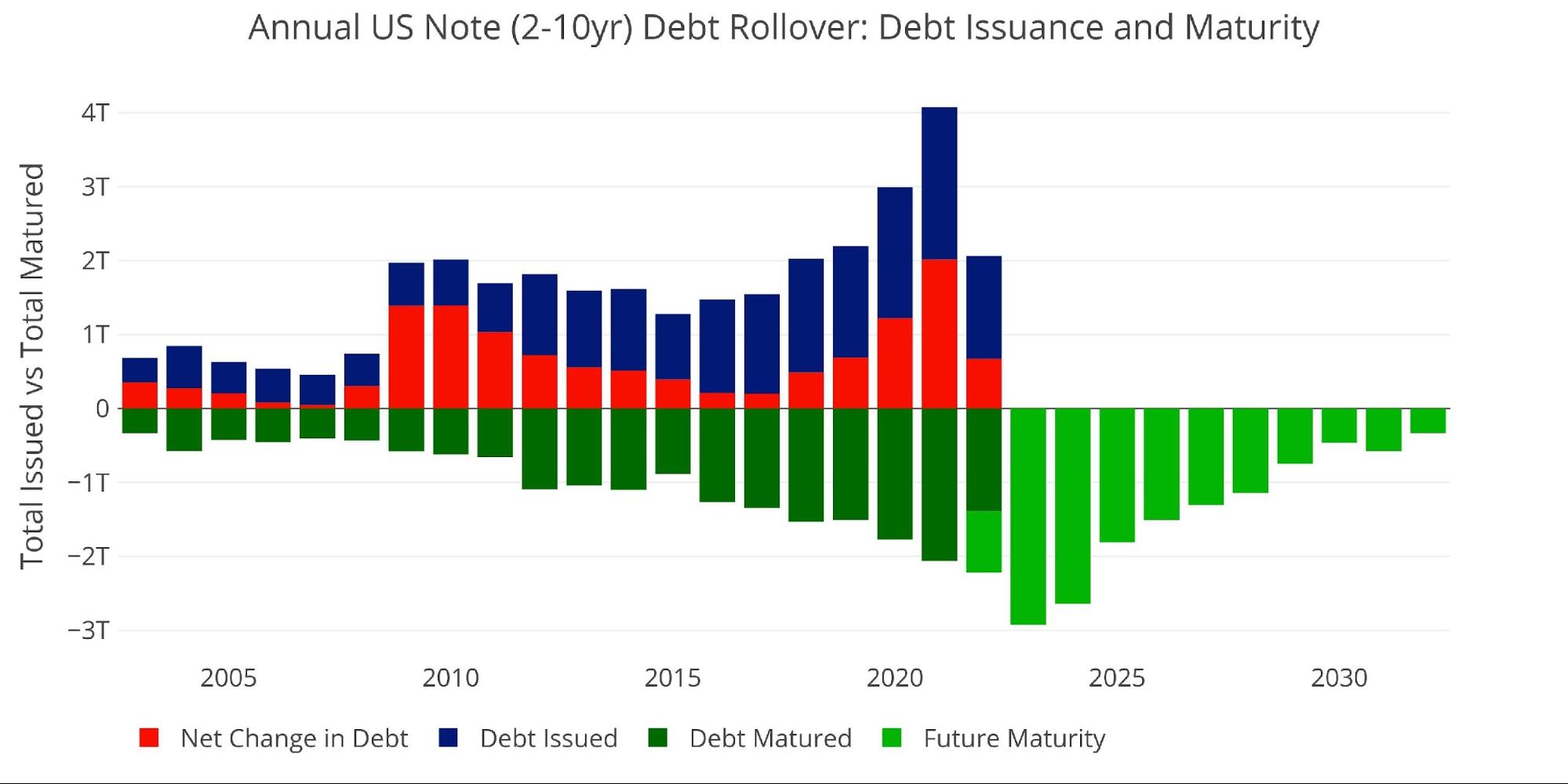

Treasury Notes (1-10 years)

Despite the lengthened maturity, the Treasury is not that well protected from a rapid increase in short-term rates. While Bills present the biggest immediate risk, Notes are relatively short-term with an average maturity of 3.49 years, and account for 44.2% of the $31T balance. The rollover schedule can be seen below. Over $6T is set to roll over by December 2024! Can you imagine the impact if the Fed has to keep rates elevated over that time? The Treasury could owe an extra $150B+ just on this portion of the debt.

Figure: 5 Treasury Note Rollover

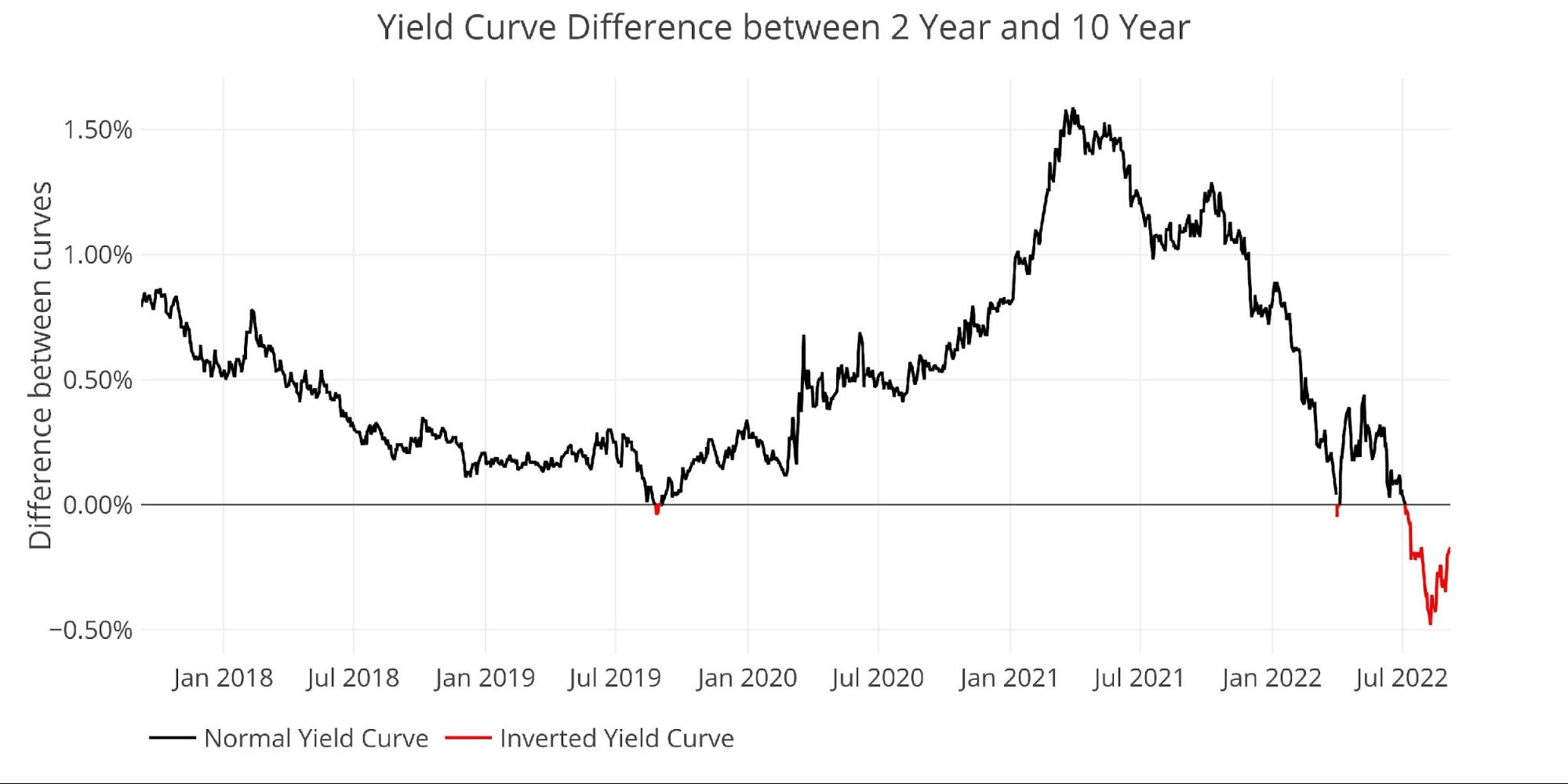

The Yield Curve

The Treasury is still benefiting from quite an inverted yield curve. This helps lengthen the maturity of the debt as it becomes cheaper to borrow on the long end rather than the short end. While they failed to take advantage of that this past month, with short-term debt seeing the largest increase across instruments, the Treasury has certainly taken advantage of it over the last several months.

The yield curve remains inverted but is less so right now. At one point, the inversion reached -48bps but has since come back to -17bps. This is one of the clearest signs the US economy is in or heading toward a recession. If a recession hits, the budget deficits could explode higher rather quickly if tax revenues dry up.

Figure: 6 Tracking Yield Curve Inversion

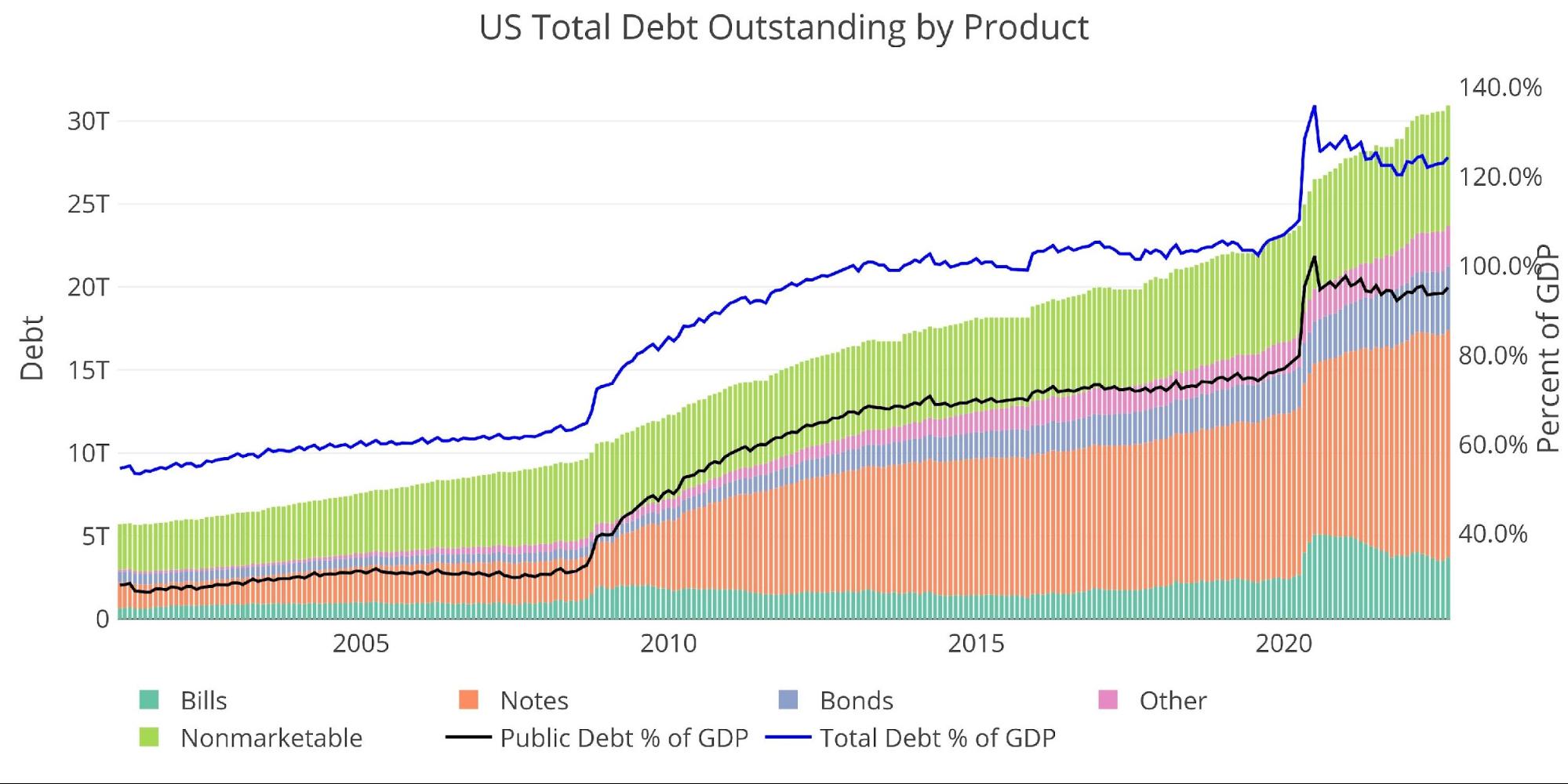

Historical Perspective

While total debt now approaches $31T, not all of it poses a risk to the Treasury. There is $7T+ of Non-Marketable securities which are debt instruments that cannot be resold and the government typically owes itself (e.g., Social Security).

Figure: 7 Total Debt Outstanding

Unfortunately, the reprieve offered by Non-Marketable securities has been fully used up. Pre-financial crisis, non-marketable debt was more than 50% of the total. That number has fallen to 23.5%. In recent months, the Treasury has increased issuance of Non-Marketable but it’s not enough to make up the ground it has lost.

Figure: 8 Total Debt Outstanding

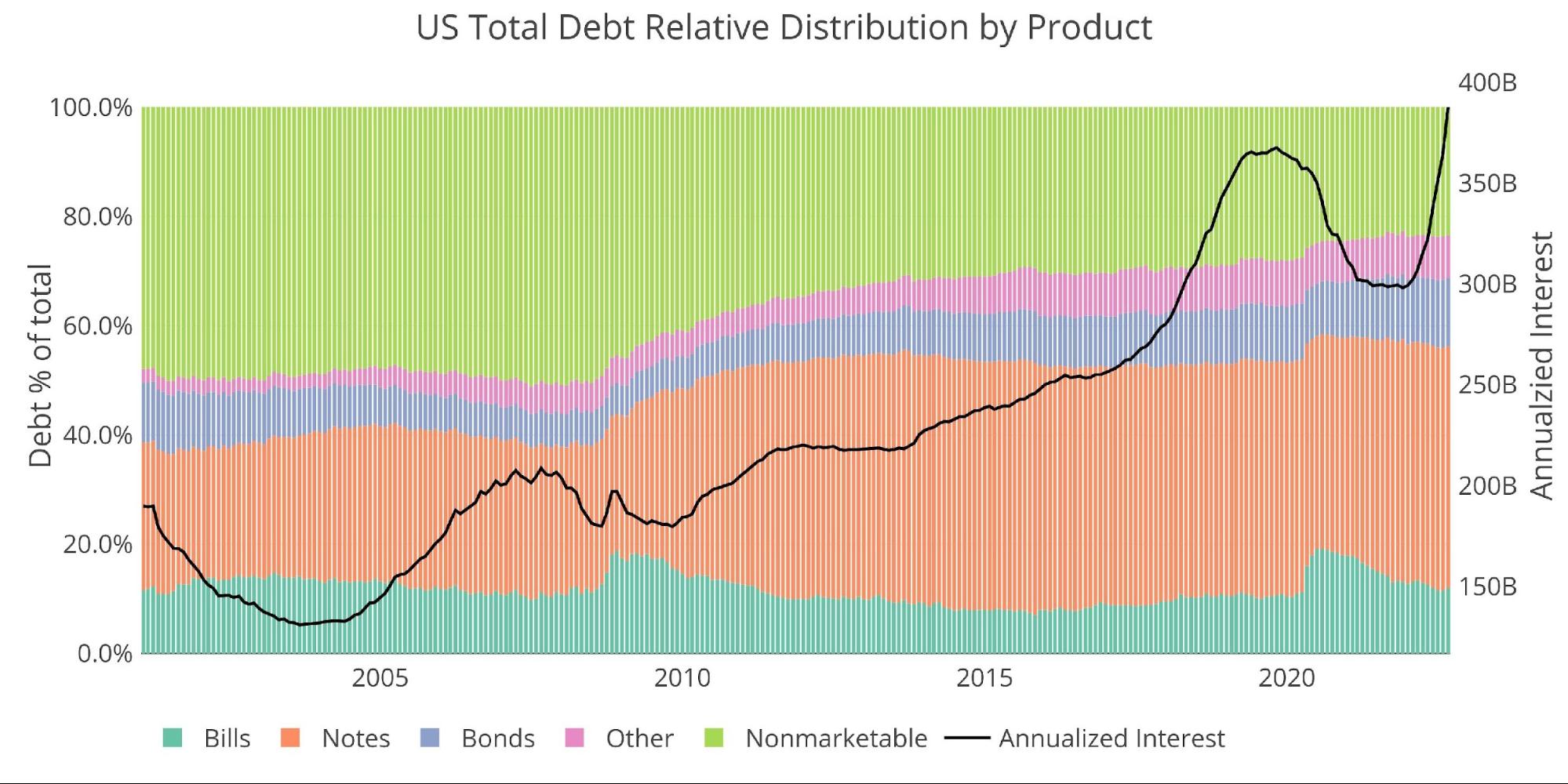

Historical Debt Issuance Analysis

As shown above, recent years have seen a lot of changes to the structure of the debt. Even though the Treasury has extended the maturity of the debt, it no longer benefits from the free debt in Non-Marketable securities. Furthermore, the debt is so large that even though the short-term debt has shrunk as a % of the total, it is still a massive aggregate number ($3.7T).

Figure: 9 Debt Details over 20 years

It can take time to digest all the data above. Below are some main takeaways:

-

- Annualized interest has increased from $299B to $388B in 12 months

-

- Over the same period, average maturity has increased from 5.9 to 6.19 years

- Over 20 years, annualized interest is up more than double from $145B

-

- The average interest rate on Bills and Notes is 1.39% and 1.55%. If the Fed increases rates by another 75bps to 3%, then this means the interest on both instruments will double upon rolling over.

-

- This will be catastrophic.

- This will be catastrophic.

-

- Annualized interest has increased from $299B to $388B in 12 months

What it means for Gold and Silver

The massive surge in interest costs is the clearest reminder that Powell must have a fast inflation fight. He cannot keep rates elevated for long or the Treasury could enter a debt spiral. Rates will have to come back down soon. Even with the extended maturity of the debt, there is simply too much of it to withstand higher rates for a long.

The Fed is clearly willing to risk recession to battle inflation. And why not? If inflation remains elevated and rates rise or even just stay where they are the US Treasury is toast. If Notes rollover at 3-4% over the next 2 years, total interest on the debt could easily exceed $750B. This would equate to additional spending of $450B in a span of three years. Interest becomes the largest item in the Federal budget by far.

This cannot happen. The Fed needs to get rates back down as soon as possible but also needs inflation to be more subdued. They have an extremely short runway and no margin for error. The fate of the dollar and the credibility of the US government are at stake. One or both could fall in short order. Gold and silver will be the best hedge against either, or possibly both scenarios.

Data Source: https://www.treasurydirect.gov/govt/reports/pd/mspd/mspd.htm

More By This Author:

Trade Deficit Still Historically High Despite Fall Since March

The Fed Is About to Start Losing Money - What Does That Mean?

Central Banks Continue To Have An Appetite For Gold

Comments

Log in or sign up to join the conversation.