Three Things – Weekend Reading: Friday, Sept 27

Image Source: Pexels

Here are some things I think I am thinking about this weekend:

1) High Yield Savings Accounts are Bad.

In the aftermath of the Fed’s rate cut “high yield” savings accounts are notifying their customers about their own decline in rates. Accounts like this or Certificates of Deposits are very popular and I am sorry to be overly critical, but I just hate these things. I don’t hate them as much as low-interest or zero-interest savings and deposit accounts, but I still hate them because I view them as very high-fee products on risk-free assets. This is light years away from charging 1% on a stock mutual fund in my opinion because the cash equivalent world is risk-free. If you came up with some sort of risk-adjusted expense ratio the fees (or embedded costs) on cash equivalents would be stratospheric when compared to high-fee mutual funds. And while investors spend huge amounts of time criticizing high-fee active funds we virtually never hear about the huge costs of risk-free cash accounts.

My general view is that if you own a cash equivalent you should reap the benefits of cash equivalents. So, when the Federal government is paying 5% in interest on cash I don’t believe banks should be the only ones to benefit from this. In fact, I think banks should be operating purely as intermediaries here who give that cash rate to their customers. But instead of doing this most banks pay absurdly low interest or rates that aren’t as good as the Fed Funds Rate.

In the case of a High Yield Savings account the bank is likely earning the FFR or higher on their own assets and they give you a little cut of the action. So, for instance, if the bank is offering 4.25% in “high yield” savings they’re likely earning the full 5% from the Fed or by buying T-Bills, and then they’re giving you a little cut of the action. This is an almost entirely risk-free transaction and some financial firms make absurd amounts of money doing this because most people don’t know how this works. They just know that 4.25% sounds like a nice figure and it’s better than 0% deposits. But this isn’t even the biggest problem with accounts like this. Not only are you getting a worse rate than what T-Bills offer, but you’re doing it in an account that doesn’t get favorable tax treatment. So, while T-Bills shelter you from state and local taxes your HYSA exposes you to full taxability.

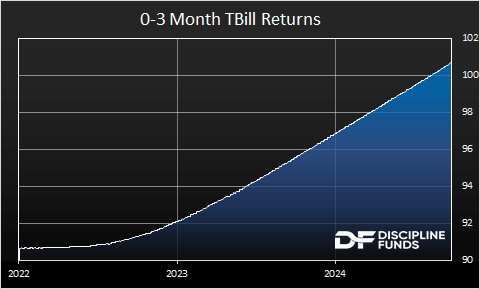

One common response to this is that you have principal risk or liquidity risk with T-Bills. First, there are plenty of low-cost Money Market Funds that offer you same-day cash sweep. But it’s also worth noting that short-term T-Bills expose you to virtually no interest rate risk. Here’s a chart of actual 0-3 month T-Bill performance over the last 3 years as the Fed raised rates. As you can see there is no real principal risk here. So these concerns are totally overblown.

At the same time, I get it. For most people, it’s probably not worth shuffling small sums of money around and opening new accounts just to earn a little more interest per year. But for people (or entities) with significant cash needs, this is a very big issue. HYSAs are terrible accounts for anyone with substantial cash and liquidity needs. Don’t use them.

2) Gambling is Bad.

I talk a lot about financial discipline here and one of the most disciplined things an investor can do is avoid negative sum games. A smart investor understands the difference between positive sum games and negative sum games. Investing is a positive sum game in which you’re allocating capital to entities that are very likely to generate profits over time and distribute some of those profits to you. The growth is what we call “endogenous” because it is not a closed system, but one that can expand in perpetuity. Gambling, on the other hand, is typically a closed system in which the participants allocate capital in a negative sum game. There is a pool of assets of which the returns rely on the outcome of a fixed event such as a sporting event. It’s a negative sum because the pool is a closed system with typically high fees so the average participant earns a negative return in part because the house is taking a cut of the closed pool.

I used to gamble a lot for fun. I’d play blackjack and bet on sports. And about 10 years ago I stopped cold turkey. I just woke up one day and said “I refuse to play negative sum games”. That might be because I am turning into a boring old man, but it’s also because I’ve become much more financially disciplined in the last 10 years. And financial discipline includes avoiding (or at least minimizing) negative sum games because we know, mathematically, that these are bad monetary outlays in the long run. As a result of this, I am missing out on what looks to be a golden era for online gambling. It’s everywhere! You can hardly turn on the TV these days without seeing ads for it. It’s even on the screen during live events and they’re trying to convince you to bet on events within the event. It’s like a virus infecting the casual sports viewer trying to lure them into this negative sum game. These ads are usually framed as an enjoyable and fun endeavor, but what’s the real impact of all this, and is it just healthy good old fun?

Well, we now have a decent amount of research on this topic since it was legalized a few years ago and the results are terrible. According to three important research papers (here, here, and here) online gambling:

- Diverts savings from positive-sum to negative-sum endeavors.

- Increases odds of bankruptcy by 25%+

- Increases domestic violence by 10%.

Now, I am not a big fan of banning things outright unless they pose a clear and significant danger to society. I don’t think you should be allowed to own a grenade launcher for instance because, despite being fun (yes, I’ve shot one), they’re obviously designed for mass destruction and mass destruction alone. Gambling, in small quantities, could just be a harmless way to spend some time. There are lots of things in life that are dangerous in large quantities but are largely harmless in small quantities. Alcohol, fast food, skipping leg day, etc. But gambling is one of those things that looks a lot more like cigarettes in that we know it’s a dangerous negative sum endeavor that is dangerous in large quantities but is also highly addictive. So I am less forgiving with my stance on gambling. To me, it’s a very slippery slope and while I don’t think we should ban it I do think we need to do more to constrain the advertising and messaging around it. Like cigarettes, I’d like to see restrictions on advertising, and to the extent they are advertised, I think the warnings need to be clear. This is a bad thing to do that, even in small quantities, can be addictive and result in perilous large quantities.

None of this is as bad as the lottery of course and it’s a real shame that our government benefits so much from something that we all know is a tax on the people who can least afford to pay those taxes.

3) Videos Are Good!

I’m going to start recording videos again and I’d love to get some feedback on what kind of videos readers might be interested in. We started the Three Minute Money videos over a year ago, but then some friendly lawyer informed me that someone else had copyrighted the term. Whoops. And then I discovered that making three-minute videos about dense financial topics is, um, extremely hard. Maybe I ramble too much or something, but it was just way too much effort for videos that are so short. So, I am thinking about bringing back a more long-form video type, probably in the 10-minute range. If you have topics or a format that you would like to watch I’d love to get some feedback. I really enjoyed making the videos, but just need a format that is more conducive to the relatively complex topics that I like to focus on.

Stay disciplined!

More By This Author:

Three Things – Weekend Reading: Saturday, Sept. 21Three Things – The Fed Goes 50!!!!!

25 Or 50?

Disclaimer Cipher Research Ltd. is not a licensed broker, broker dealer, market maker, investment banker, investment advisor, analyst, or underwriter and is not affiliated with any. There is no ...

more