The Ups And Downs Of Inflation Expectations

- Breakevens soar to new highs as the bond market rout continues.

- Inflation for longer was the theme last week, with the 5y5y swap shooting up.

- While survey data suggests we might not be at peak inflation, the Fed should ultimately rule the day given its very hawkish stance.

Stocks and bonds are both down about 10% year-to-date, using the S&P 500 total return and the US aggregate bond market as proxies. Risk parity has gone 'poof.' While April is historically a bullish month, there have been days of indiscriminate selling across asset classes recently.

Commodities were a spot to hang out, but that too got hammered last week – the Invesco DB Commodity Index Tracking Fund (DBC) dropped more than 4% from its closing peak on Monday.

Hawks Circling, Bond Volatility Up

The catalyst was, of course, the Fed and its ever-evolving hawkish tone. With Chair Powell and other FOMC members making no qualms about hiking rates 50 bps at several upcoming meetings, with perhaps a 75 bps hike spiced in at the June gathering, the bond market has been skittish, to say the least.

Implied volatility on long-term Treasuries has spiked, while the ICE BofA MOVE volatility index continues to run at historically elevated levels. Our Weekly Macro Themes report takes a fresh look at where Treasuries are headed from here.

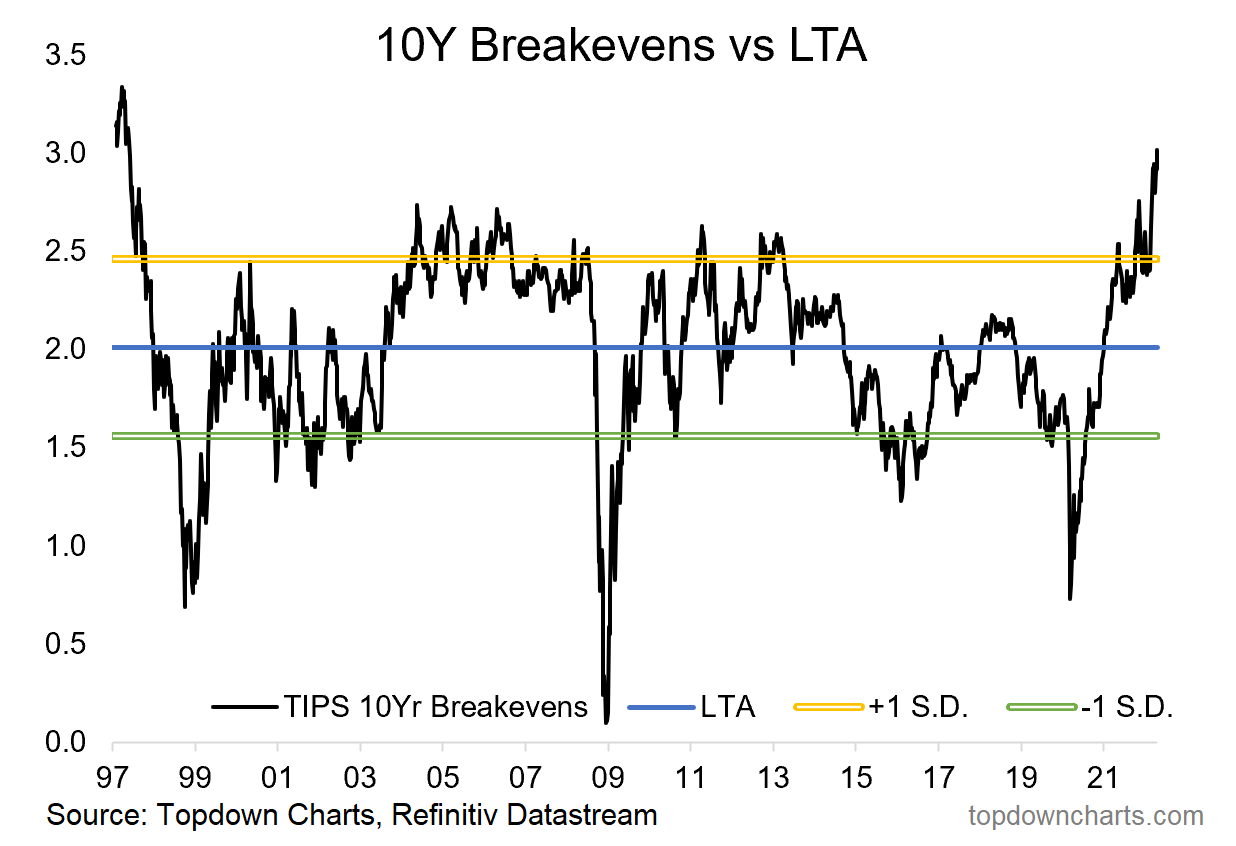

Breakevens Reach New Highs

It’s not just interest rate-sensitive fixed income that has been the star of the story. Inflation swaps have shot higher. US 10-year breakevens, as measured by the yield difference between TIPS and same-term Treasuries, rose above 3% for the first time since the late 1990's. Moreover, the latter half of that period – as measured by the 5y5y breakeven – spiked to 2.7% at the high on Thursday before settling just shy of 2.6% by the week’s close.

Featured Chart: Inflation Expectations Take a Leg Up

Surveys Say More Inflation Upside

We think that breakevens could increase further. The basis for this assertion comes from consumer and business survey data. Also consider that inflation fears only continue to mount, and upside inflation changes have surprised most traders. Consider that so many of the recent US CPI prints have verified hotter than analyst consensus expectations.

Conservatism Bias at Play?

What’s more, charts of market-based inflation expectations keep moving up and to the right across geographies. It appears the new reality of “higher for longer” consumer price changes is seeping into the psyche rather than hitting all at once. So there are certainly factors suggesting room to run on inflation swaps from here.

Powell Aims to 'Whip It Good'

But here’s the thing – inflation expectations are high relative to the average of the last two decades. The Fed is also hard at work to whip down the rate of consumer price increases. The second piece of our assertion is that the Fed’s goal to crush inflation at seemingly all costs will be enough to temper breakevens later in the year.

Bottom Line: We see a bit more upside in TIPS breakevens, but current levels are stretching versus historical norms. Policy tightening will ultimately dampen inflation expectations.