October Report - Navingating Through Uncharted Economic Waters

Image Source: Pexels

We are navigating through an unknown economic environment. Central banks are experimenting with controlling inflation versus causing recessions. Economists are trying to compare today's macro trends to those of the late 60’s, early 70’s. The truth is that they don’t know the outcome, as today’s labor markets are very different from the past.

As the powers-to-be play out this experiment, the safety of our funds should be our priority. Be defensive. Have a plan.

Dollar Up, Everything Else Down

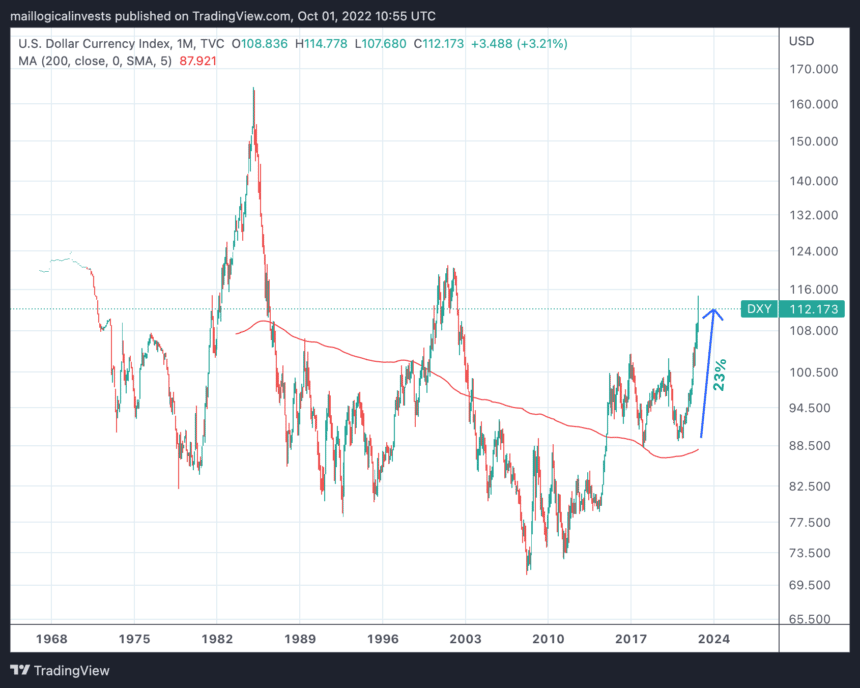

The US Dollar Index is up 17.6% year-to-date. That is quite a large change. It is also part of the reason why gold and commodity prices are falling, as they are priced in US dollars. The question now becomes how high can the US Dollar Index go? If we were to enter a longer recession, this level could persist.

US Dollar Index, monthly prices, 1968-present.

As you can see from the chart, this only happened in the 1980’s. When the US dollar rises substantially, equity/bond/gold correlations fail and all asset prices fall in tandem.

Treasuries

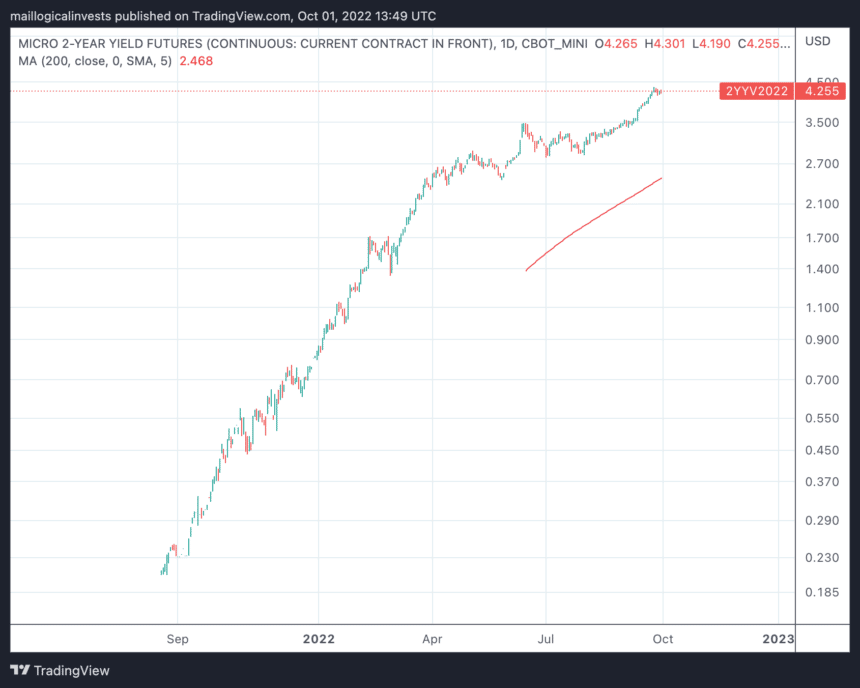

Just a few months ago, it was inconceivable to receive 4% interest, risk-free via a one or two-year Treasury. Below is a chart of the 2-year Treasury yield. At the beginning of the year, it was at 0.8%. It is now at 4.2%, a 400% rise.

CBOT, 2-year yield future, 2022.

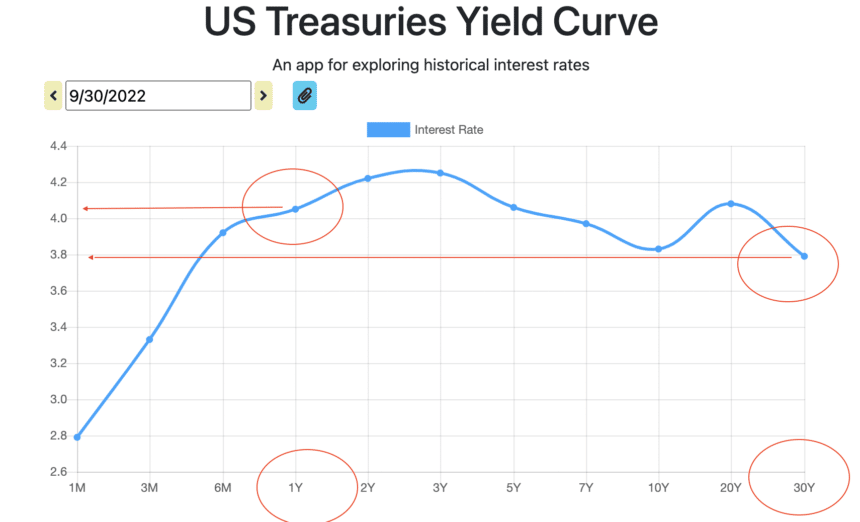

The long-dated Treasuries have been slower to rise. The yield curve has once again inverted, with 1- and 2-year Treasuries yielding more than the 30-year one, currently at 3.8%.

The inversion, coupled with the current high yield for a short-term paper, could signify further equity weakness as money can be parked for one year at a 4% interest.

The S&P 500

The Fed’s last two bold hikes of 0.75% each show that it has prioritized fighting inflation over crashing the market. And hence the S&P 500 lost 9% just this month and sits at -23% year-to-date.

As we mentioned in the last newsletter, a recession is expected at least in Europe as consumers and businesses face much higher energy costs. This may have been priced in to a certain degree in equity prices, but it could possibly get worse. This, coupled with recent developments in Italy, Russia, and Iran, could cause further pain.

As we mentioned in the past, a possible scenario is that the Fed may overshoot both ways. It may be overacting to inflation fears by raising rates aggressively. This could cause markets to fall and slow down inflation (given that the labor market does not follow the inflationary pressures). Once the Fed sees that it has slowed down inflation, it may try to recover the markets by easing a bit, and so on and so forth.

Performances

More By This Author:

The Logical-Invest Newsletter For August 2022

The Logical-Invest Newsletter For July 2022

The Logical-Invest Newsletter For June 2022

Disclaimer: Logical-Invest.com is not a registered investment advisor and does not provide professional financial investment advice specific to your life situation. Logical Invest is solely an ...

more