Real Interest Rates Turn Positive, But It’s Negative For Gold

The recipe for happiness is to see the bright side of even negative situations. Positive interest rates are rather bad news for gold. Here’s why.

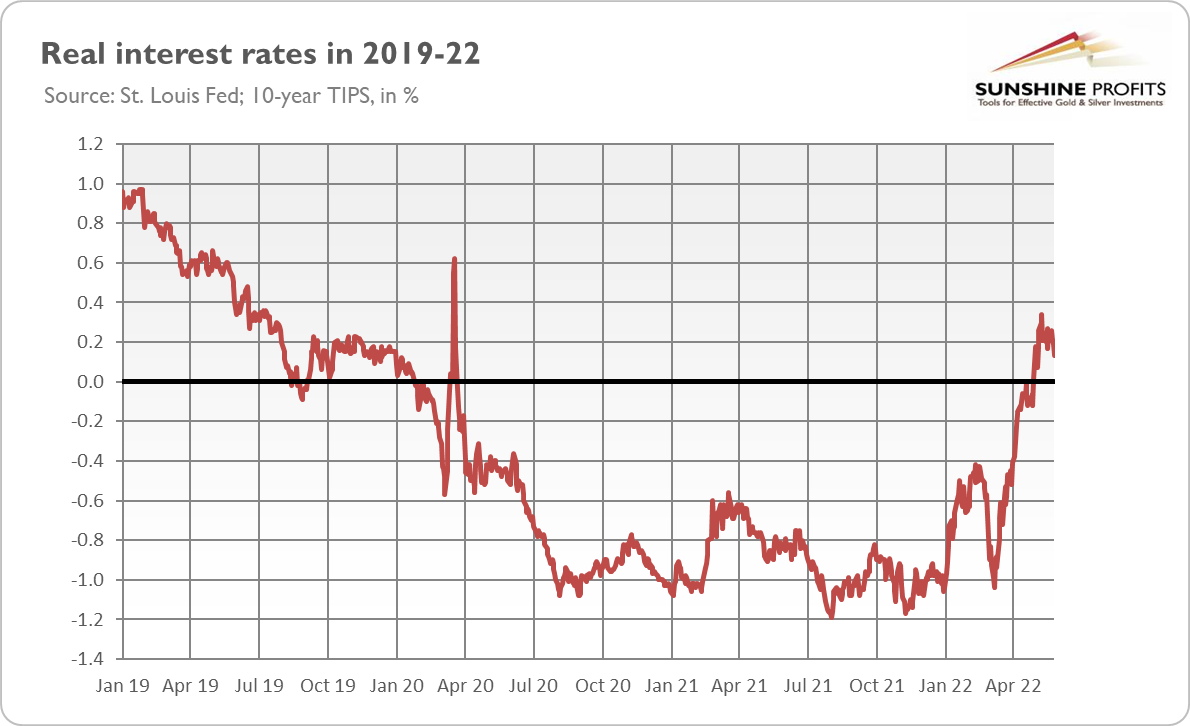

This is a huge change, perhaps a game-changer! What do I mean? The chart below – which is one of the most important charts about the current US economy and the gold market – tells the whole story.

Do you see what I see? The US real interest rates – measured here by 10-year inflation-indexed Treasury yields – have finally returned above zero. It means that the real interest rates are no longer negative. This is a big story!

Why? Because gold performs much better during periods of negative real interest rates than positive ones. This is because gold is a non-interest-bearing asset, so the higher interest rates, the higher the opportunity cost of holding gold, and vice versa. In other words, when real rates are negative, owning the yellow metal is more attractive, but when rates are positive, holding gold becomes less alluring.

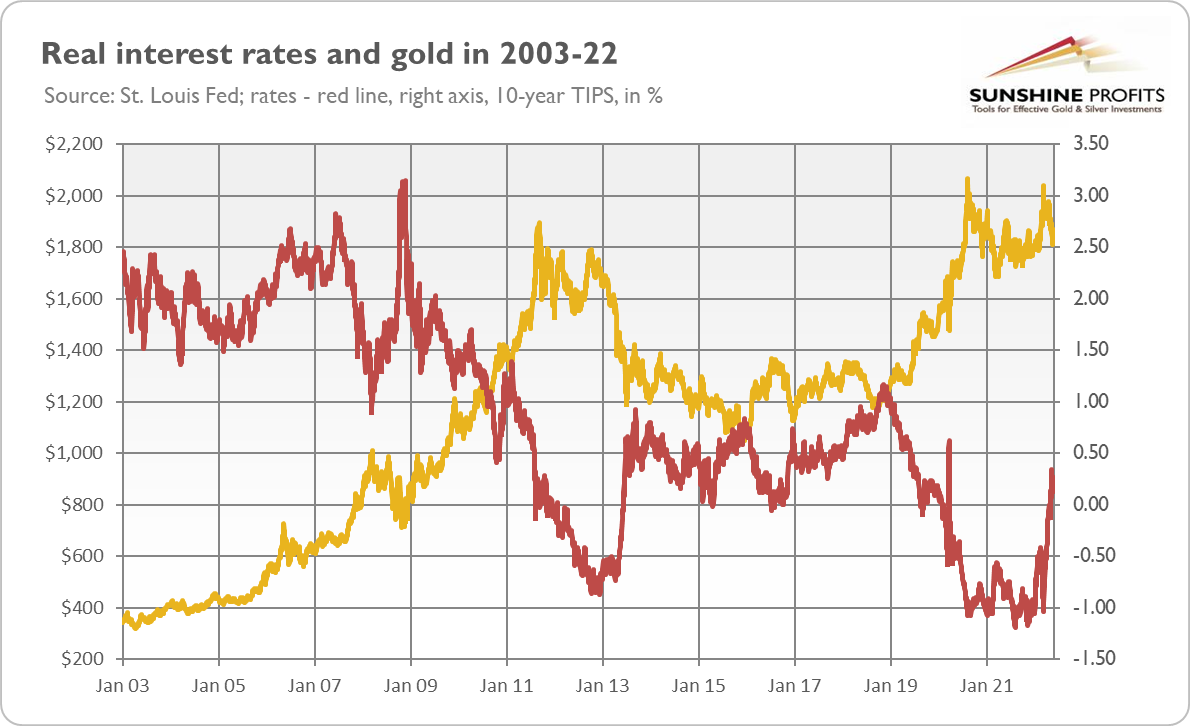

To be sure, the real interest rates remain very low, and at levels close to zero, they don’t have to strongly hit the yellow metal. However, gold is usually strongly correlated to the real interest rates (please see the chart below), so their further rise could be detrimental to gold.

Indeed, if history is any guide, dark clouds may lie ahead for gold. The previous case of normalization of interest rates in 2012-2013 pushed the yellow metal into the bear market. The surge in the real interest rates from -0.87% to 0.92% was accompanied by a plunge in gold prices by 18.2%, from around $1,700 to around $1,390, and even lower later.

This time, the real interest rates have soared from around -1.0% to around 0.25% by the end of May. So far, gold’s response was rather limited, i.e., it declined from $2,039 to $1,810, or 11%. However, if we see further increases in the real rates, gold may continue its downward move. Given how high inflation is, the upswing in real interest rates has much further to go, and this is also what some Fed officials suggest. For example, Fed Governor Christopher Waller said at the end of May:

If inflation doesn't go away, that (...) rate is going a lot higher, and soon (…). We are not going to sit there and wait six months (...). I am advocating 50 on the table every meeting until we see substantial reductions in inflation. Until we get that, I don’t see the point of stopping.

However, every cloud has a silver lining. A large part of the upward move in the real interest rates is probably already behind us. I think that the bond yields may increase further, as both inflation and the Fed didn’t say the last word, but the move should be limited. The key difference between 2012-2013 and now is that the taper tantrum was accompanied by moderation of inflation and expectations of an acceleration in economic growth. Now, the Fed’s tightening cycle is occurring amid high inflation but also collapsing economic growth expectations and a slowdown in GDP growth. This is also what markets are betting on right now. They dialed back interest rate expectations, assuming that the worsening economic data might force the Fed to adopt a less aggressive stance.

Moreover, the level of both private and public debt is much higher, which makes the economy more sensitive to interest rate hikes. Positive real interest rates imply the end of the era of ultra-low rates and ultra-easy money. All debtors, including the Treasury, will now have to pay more in interest. The tightening of financial conditions could put many borrowers in trouble. Hence, the macroeconomic environment is more supportive of gold prices than a decade ago.

Indeed, so far we’ve had high inflation accompanied by fast economic growth. However, as I warned many times, the impressive pace of growth resulted simply from the rebound from a deep recession, and it was impossible to maintain. Hence, we are moving closer to stagflation, gold’s favorite macroeconomic conditions. Stagnation has been so far the missing part of the equation, which is why gold didn’t react positively to high inflation, but this may change in the future. In 2022, America should keep its head above water, but 2023 may be a truly challenging year – which bodes well, at least for gold.

However, it may take some time before the new rally in gold starts. Prices should remain in a downward (or sideways) trend until the real interest rates reach a peak, as they did in 2008 (or at the end of 2018). They’ve retreated recently, as investors are focusing more on the risk of recession and less on inflation, but upward move in interest rates can resume after a while, especially if inflation is again above market expectations.

Disclaimer: All essays, research and information found on the Website represent the analyses and opinions of Mr. Radomski and Sunshine Profits' associates only. As such, it may prove wrong ...

more