The Bank of England holds the keys to the next gilt rally, if it can convince markets that a more dovish path is the right choice. The USD curve re-steepening on pivot hopes has run out of steam, expect limited appetite to trade such a momentous policy change until next week’s Federal Open Market Committee meeting.

Gilts hope for a more prudent fiscal tone

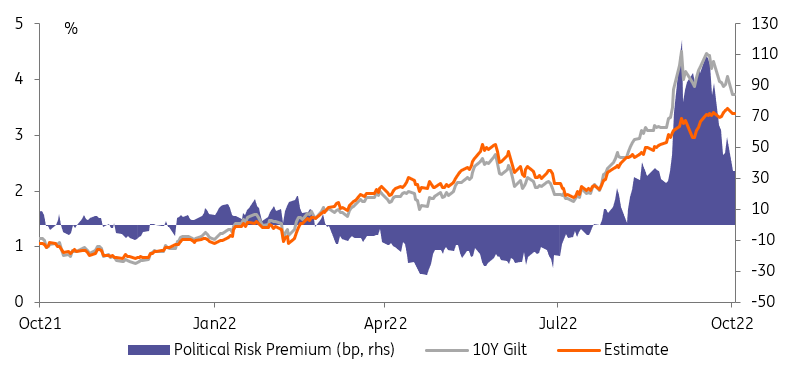

Rishi Sunak’s appointment as prime minister was greeted by a relief rally in gilts yesterday. We think this is justified by a lower political risk premia. The market hope is that Sunak, a former chancellor of the exchequer and architect of tax rises that were subsequently reversed by the ill-fated mini-budget, will err on the side of fiscal caution. In practice, this would mean keeping Jeremy Hunt as chancellor, no attempt to delay the budget statement due on 31 October, and no attempt to steer away from the fiscal consolidation that is now widely expected. We should get a pretty good idea of at least the first two after Sunak's speech today.

The ball is now firmly in the BoE’s camp

Provided all these assumptions hold, the ball is now firmly in the BoE’s camp. The swap curve is still pricing a terminal rate around 5% which in turn is limiting 10Y gilt yields’ ability to rally much further below 4%. Dave Broadbent, and then Catherine Mann, have signalled this is excessive. Chief Economist Huw Pill is scheduled to speak today. Him throwing his weight behind this view would help chip away at market pricing, but there is a long way to go. Meanwhile, the political risk premium in gilts is being eroded further. They outperformed 10Y Treasuries more than 30bp yesterday, and 10Y Bunds by more than 20bp.

Realistically, a further drop in rates at both ends of the curve is possible. Some of the jump in BoE hike expectations in September is explained by the view some took that the Bank would have to hike rates to defend the pound. The stabilization in the pound in itself could be the basis for some re-pricing lower in rates. On the other hand, we note that the BoE has struggled to convince markets of its less hawkish view than what is priced in the curve pretty much since the start of this hiking cycle around a year ago. This means a reversion lower will need a catalyst. Another wave of fiscal consolidation in next Monday’s budget could achieve this.

Sunak's appointment as PM further reduces the political risk premium baked in gilts

Image Source: Refinitiv, ING

Fed pivot hopes run out of fuel

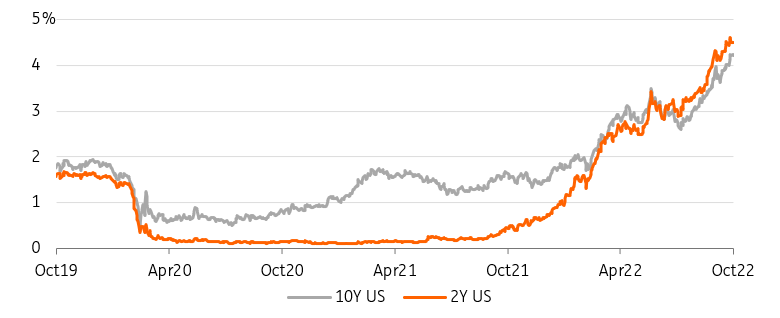

Fed pivot hopes seem to have taken a breather after being fanned by an article in the Wall Street Journal on Friday. We base this statement on the fact that the Treasury 2s10s curve failed to continue steepening yesterday. We think monitoring the slope of the curve is the cleanest way to check for hopes of a less hawkish Fed, alongside front-end rates of course.

This is because the impact on the long-end risks is harder to read. On the one hand, a less hawkish Fed would a positive for bonds regardless of their maturity. Remember that it will also be under pressure to stop quantitative tightening as soon as the economy is in a recession, or earlier if a financial stability accident occurs. On the other, if markets aren’t fully convinced that the inflation spike is behind us, then they will price a higher, not lower, path for policy rates in the long-run, in reaction to more elevated inflation expectations in the future.

Recent weeks have shown that duration risk should not be underestimated

If anything markets are likely to get mixed signals, at best, until the November FOMC meeting. This is hardly a case for battered investors to boost their Treasury exposure just yet, especially since recent weeks have shown that duration risk should not be underestimated. A drop in US consumer confidence today could provide more heft to the dovish argument but we think this would benefit the front-end the most.

A dis-inversion of the US Treasury curve should greet a less hawkish Fed

Image Source: Refinitiv, ING

Today’s events and market view

European data releases today centre on Germany’s Ifo survey and UK’s CBI orders and selling price. On the former, a further dip is expected after Germany’s PMI manufacturing missed expectations yesterday, and after the Zew current situation also disappointed. More broadly, the eurozone seems to be entering into the thick of its winter recession, which so far has failed to show in euro rates. On the latter, it is hard to overstate the importance of the selling price component in the middle of an inflation spike.

Staying on the topic of UK inflation, it will be interesting to hear whether BoE Chief Economist Huw Pill shares some of his colleagues’ assessment that the swap curve is pricing too much tightening (see above). Mario Centeno of the European Central Bank, and Christopher Waller of the Fed, are the two other central bank speakers listed today.

Germany is due to sell €4bn in 5Y debt amid a growing focus on deteriorating auction statistics. Greece is also scheduled to sell floating rates notes. The UK will also auction 17Y linkers, and the US Treasury will auction 2Y notes.

Did the national gasoline price rebound in September/October dent sentiment? We’ll find out today with US consumer confidence statistics. House prices and the Richmond Fed index complete the picture.

More By This Author:

Asia Morning Bites - Mon, 24 Oct.

EUR & ECB crib sheet: Hawks can’t lend their wings to the euro

China: President Xi Has More Say On Economic Policy

Comments

Log in or sign up to join the conversation.