Image source: Pixabay

Markets are awaiting Tuesday’s US CPI release which should give confirmation that the disinflation trend continues. But that's not enough, as a consensus month-on-month outcome would still be a tad too hot for comfort. Looking further ahead, foreign buyers aren't absorbing large UST supply, putting upward pressure on term premium.

US CPI inflation will fall, but Treasury yields are still at risk of rising

We're a bit troubled about Tuesday’s CPI report. On the one hand, year-on-year rates will fall, with practical certainty. That's because of a base effect. For January 2023 there was a 0.5% increase on the month, so anything less than this will bring the year-on-year inflation rate down, for both headline and core.

So why are we troubled? It's the size of the month-on-month increases. Headline is expected at 0.2% and core at 0.3% MoM. The 0.2% reading is just about okay, especially if it is rounded up to 0.2%. But the 0.3% on core is not okay. That annualizes to 4%, which is clearly too high. And it's been at 0.3% MoM for the past two months, and if repeated it would be three of the last four months. Again, that annualizes to 4%.

If we get the anticipated 0.3%, we doubt there can be a positive reaction. At the other extreme, a 0.4% outcome would be a huge negative surprise, one that would likely cause the probability for a May cut to move comfortably south of 50%. That would throw the easing inflation story up in the air, bringing the US Treasury yield with them. But this is unlikely, as the tendency has been for inflation to dip as opposed to spike.

We assume a consensus outcome for inflation, and given that, we'd expect to see the 10yr Treasury yield creeping towards 4.25%. For the market to conjure up a positive reaction to the inevitable fall in year-on-year rates, there needs to be a 0.2% MoM outcome for core.

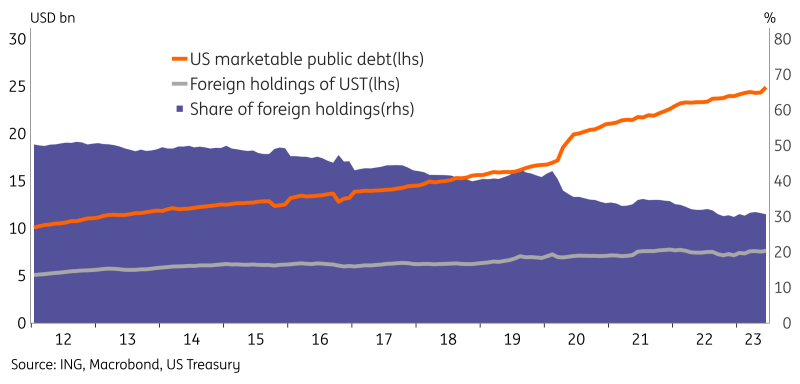

Foreign UST appetite not enough to absorb issuance

The ECB's Lane spoke about financial flows and shared data that showed renewed interest by foreign investors in eurozone debt securities. Lane notes that foreign investors were a significant seller of eurozone government debt securities in 2021-2022, which matches the period of significant ECB balance sheet expansion. The trend reversed in 2023 when the ECB started unwinding its balance sheet and foreigners became net buyers again. With high debt issuance and a shrinking ECB balance sheet, the growing interest of foreign buyers is welcomed to keep long-end euro yields from rising too much.

In the US the amount of government debt to absorb in the coming years is even larger and foreign investors do not seem to come to the rescue. Looking at US foreign holding statistics in the figure below, we see that foreign holdings are diminishing as a share of total USTs. The significant issuance during the pandemic was not matched by an uptake from foreigners. Instead, as Lane also argued, in the eurozone the central bank was the big buyer. Looking at the downward trend of relative foreign holdings, it seems unlikely that foreign buyers have enough appetite to absorb the increase of USTs from the Fed and the Treasury in the coming years. Low demand from foreign buyers for USTs will have an upward effect on term premia, leading to structurally steeper curves.

Foreign UST holdings as share of public debt in decline

Tuesday's key data and events

The main driver of markets will be the US CPI numbers for January. In the shadow of this, we have Germany's ZEW survey in the eurozone. The UK's data-heavy week will kick off with employment figures on Tuesday, followed later this week by CPI and GDP data.

We have Italian 3y, 6y and 20y auctions totaling EUR 8.5bn, a GBP 1.5bn 9y Gilt Linker, and a EUR 5bn German Bobl auction.

More By This Author:

Gold Monthly: Assessing Fed Policy And Geopolitical RisksThe Commodities Feed: Oil Trades Softer

Monitoring Turkey: Strengthening The Higher For Longer Signal

Comments

Log in or sign up to join the conversation.