Image Source: Pexels

Powell’s spin on the latest economic data matters less than the data itself. Don’t expect much clarity on 50bp hikes or the terminal rates but note that the hawkish re-pricing is helpful. At the ECB, data dependence is mainly on wage dependence and consumer inflation expectations.

Don’t expect Powell to rule anything out

Jerome Powell’s Congressional testimony is today’s main event. It is nearly certain that the Fed chairman’s tone will reflect better economic data since January and more specifically inflation. Both make his disinflation optimism at the February meeting look misplaced. What markets would like to know is something more specific. Firstly, how high will the Federal Open Market Committee revise its estimate of the terminal rates in this cycle? Secondly, is the Fed going to revert to 50bp hike increments in March after a downshift to 25bp in February?

On both counts, we think markets will be disappointed. There is still one jobs and one inflation report before the next Fed meeting so it wouldn’t make sense for the Fed to give up some optionality by guiding markets on one outcome or the other. Even if our hunch is that reverting to 50bp hikes is still the minority outcome compared to a longer string of 25bp hikes at the coming meetings, it is fair to say that the recent hawkish re-pricing is helpful in the fight against inflation. This is one more reason for Powell not to take anything off the table.

Central bank commentary should lose its importance compared to the economic data guiding it

The last point to make is that the Fed’s professed data dependence means central bank commentary should lose its importance compared to the economic data guiding it. The caveat is of course that this supposes market participants are understanding the Fed’s reaction function correctly. Given the shift in tone from late 2022 to early 2023, we wouldn’t blame investors for being confused. Given recent data, whatever Powell says, we wouldn’t be surprised if markets conclude that erring on the hawkish side is the correct strategy. Even if we find dollar rates high, we doubt today’s speech will prove the catalyst of a reversal of the February Treasury sell-off.

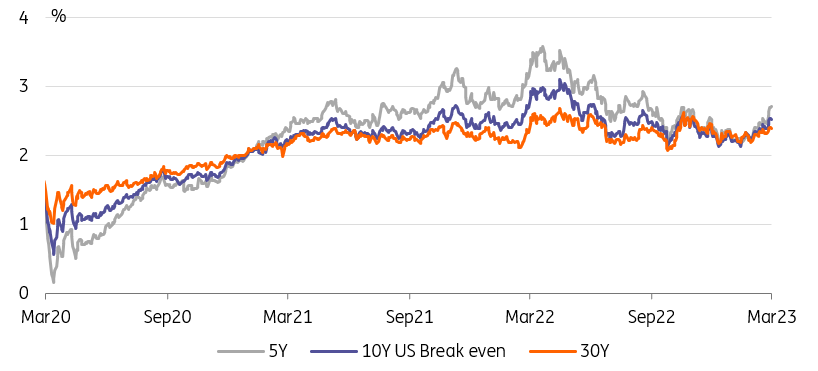

Don't expect Powell to rule anything out as inflation break-evens are rising again

Image Source: Refinitiv, ING

ECB: Data dependence is wage dependence

As the self-imposed European Central Bank’s pre-meeting quiet period is due to start on Thursday, we’re likely to see more unscheduled attempts to skew expectations. There is clearly a range of opinions between the doves (eg, Mario Centeno yesterday) and hawks (Robert Holzmann). On the dovish side, the focus seems to increasingly be on celebrating the drop in headline inflation forecast owing to the fall in energy prices, while the hawks flagged the acceleration of core inflation to push for further 50bp hikes beyond the one already signaled in March.

ECB has struggled to kick its forward guidance habit

Despite the stated data dependence aim, the ECB has struggled to kick its forward guidance habit. This is to say that we do not rule out further attempts to guide markets toward certain outcomes at the May and later meetings. One key variable going forward, as chief economist Philip Lane highlighted in a speech yesterday, will be wages. A jump in inflation expectations was another risk he stressed, which means today’s ECB survey of consumer expectations should receive a great deal of attention. Meanwhile, market-based inflation compensation is on a tear. Barring a sudden turn of events, these risks are going to keep EUR rates high. In fact, we would expect them to narrow the gap with their US peers.

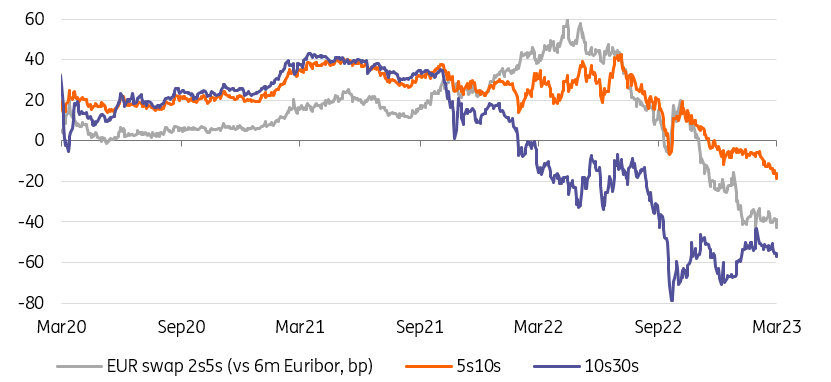

The EUR curve is power-flattening, with core inflation keeping the ECB hawkish

Image Source: Refinitiv, ING

Today’s events and market view

An upside surprise in German factory orders in January on better foreign demand should further slow the bond rally.

Today’s economic calendar is relatively thin with only Spain’s industrial production in the morning and the US wholesale inventories in the afternoon. The ECB’s survey of consumer expectations, including questions on inflation, will probably gather more attention.

Instead, the focus in European hours will be on supply. The European Union mandated banks for the launch of a long 10Y benchmark. This will be alongside auctions from Austria (10Y/30Y) and Germany (10Y Linker).

Away from the eurozone, bonds supply will be short in maturity, with a 2Y gilt and 3Y T-note auctions in the UK and US respectively.

Last but not least, Fed Chair Powell is on the docket for the first day of his two days of testimony before Congress. Dollar rates are close to the top of their range for this year but we doubt Powell's intervention is what will make them come down.

More By This Author:

FX Daily: Dollar Can Hold Gains On Limited Powell PushbackFebruary Us Jobs Report Preview – Was January A Fluke?

Eurozone Retail Sales Tick Up Less Than Expected In January

Comments

Log in or sign up to join the conversation.