Image Source: Pexels

The US and European economic trajectories are diverging. Yields have followed, albeit more modestly. In both cases the result is ever flatter curves, helped by seasonal factors.

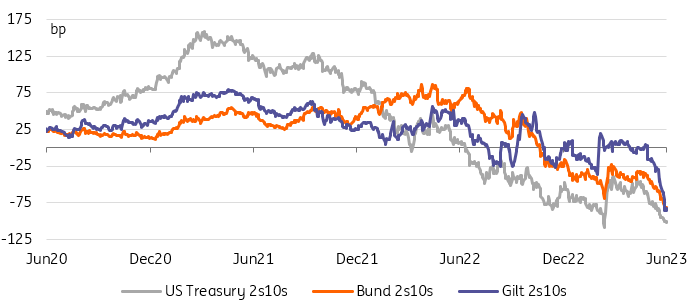

Yield differentials widen, but all curves flatten

It is hard to completely dismiss technical factors when finding an explanation for the continued flattening of yield curves heading into the summer market lull. Expectations of calmer market conditions in the summer don’t always come true but worse liquidity make investors wary of keeping positions that carry negatively, for fear of being unable to exit them should markets move against them. We think this is an important factor adding a tailwind to the curve flattening. We think steepeners have been a popular trade in recent months as investors foresee the end of central banks’ hiking cycles. The problem is, these are costly to hold. For instance, a euro swap 2s10s steepener costs over 6bp per quarter in carry. Its US dollar equivalent cost over 17bp.

A euro swap 2s10s steepener costs over 6bp per quarter in carry. Its US dollar equivalent cost over 17bp

Of course, it helps that curve flattening is the rational reaction to a world where the economic outlook is worsening, look for instance at Europe or at the disappointing recovery in China. Add to that central banks adding another layer of hawkish paint at the European Central Bank‘s (ECB) Sintra conference which continues today, and you have the perfect recipe for a flatter curve. This thesis get an important reality check over the coming days in the eurozone, in the form of the June inflation data. Italy is the only country to publish its own today, but markets may well be tempted to extrapolate its finding to other countries until they publish their own.

One country that seems impervious to the overall gloom is the US. Perhaps due to its lower reliance on global demand for growth, or perhaps due to the resilience of its domestic job market. The result is the same. Markets increasingly believe the Fed will hike at least once more in this cycle. If US curve developments are highly correlated to its foreign peers, albeit for slightly more upbeat reasons, its curve has shifted upwards relative to its European peers. Despite arguably encouraging progress relative to Europe on the inflation front, euro-dollar yield differentials have widened. This yield divergence coincides with the divergence in economic surprise indices, albeit to a less spectacular extent.

EU gloom and US glee both result in flatter curves, helped by carry

Image Source: Refinitiv, ING

Today’s events and market view

Italy is the first Eurozone member state to release its June inflation today. It will be followed by Germany and Spain tomorrow, and France and the eurozone on Friday. ECB monthly monetary aggregate data, including M3 growth, and Italian industrial production complete the list.

US data is relatively thin today, with only mortgage applications and inventories to look out for.

This will leave plenty of time for investors to scrutinise central banker comments with an all-star line-up comprising Fed, ECB, Bank of Japan and Bank of England governors.

TLTRO and eurozone financial system nerds will also look at the 3m LTRO allotment which settles tomorrow, a day after today's June TLTRO repayments. Yesterday, settling with the repayments, the central bank allotted €18bn at the weekly main refinancing operations facility, the most since 2017. Presumably, some lenders find its 4% interest rate the most attractive option, or maybe the only available, to finance the repayment of TLTRO funds.

Italy accounts for today’s euro sovereign bond supply with 2Y debt, followed in the afternoon by the US Treasury selling 2Y FRN and 7Y T-notes.

More By This Author:

FX Daily: How “Contagious” Are Sintra’s Hawks?The Commodities Feed: Supply Risks Vs Demand Concerns

Italy: Confidence Data Points To A Mixed Economic Outlook

Comments

Log in or sign up to join the conversation.