Rates Spark: An Unhappy Medium

Current rates levels reflect an unhappy medium between the two scenarios. Geopolitical tensions may dominate other drivers in the near term but, sooner or later, bonds will have to contend with the looming monetary policy tightening.

An unstable equilibrium between two very different scenarios

US markets return from a holiday-lengthened weekend to a more fraught geopolitical situation than when they left on Friday. The escalation of tensions on the ground was initially balanced in investors’ minds by frantic diplomatic efforts to avoid more military action. Overnight, the prospect of Russian troops entering eastern Ukraine has brought with it the prospect of sanctions and cast doubts on the next diplomatic steps. It is fair to say that recent events have undermined the market’s confidence in its ability to guess what the endgame will be.

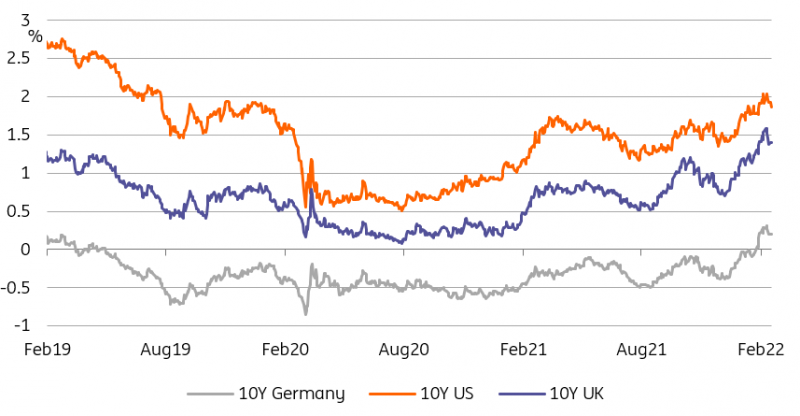

The reaction of government bonds to geopolitical tensions has been muted so far

Image Source: Refinitiv, ING

De-escalation would give way to a return of inflation concerns and central bank tightening

10Y US Treasuries and Bund currently hover respectively around 16bp and 9bp below their roughly 3-year highs. At first glance, this does not suggest that the market assigns a high probability of a significant deterioration in the situation in Ukraine, but one has to consider that current levels reflect an unstable path between two very different scenarios. In the more optimistic one, de-escalation would give way to a return of inflation concern and central bank tightening, something that would justify much higher yields.

Why government bonds have not rallied more

We have no insight to offer on near-term geopolitical developments, but we side with the fundamental picture in the medium term. For now, the appeal of government bonds as safe havens probably justifies, if not a further drop in yields, at least a pause in their rise. Interestingly, however, not all reallocation flows need to bring sovereign yields down. For instance, an investor deciding to swap low-rated debt for government bonds in the same currency could have a neutral impact on government yields (but not on spreads).

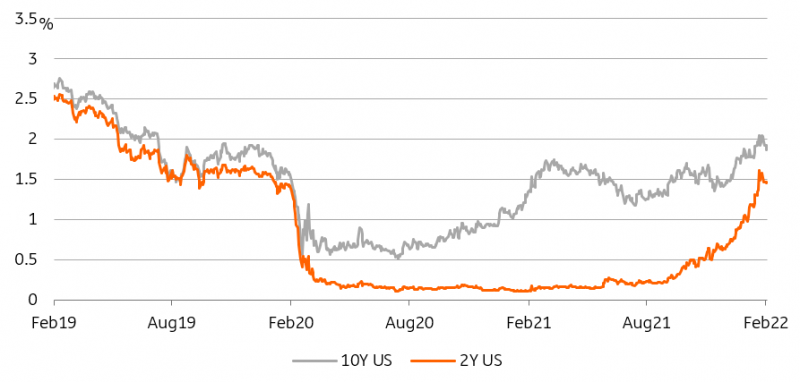

10Y rates are a better conduit for safe-haven flow than shorter maturities

Image Source: Refinitiv, ING

We expect to see long-term yields drop faster

This does not apply to all de-risking but explains that there has not been a more dramatic drop in government yields as credit spreads widen. The value of government bonds as a macro hedge against geopolitical risk is also called into question by the rising trend in interest rates. In this respect, front-end bonds may appear too risky to investors, and thus we expect to see long-term yields drop faster until and unless markets are given credible evidence of de-escalation.

Today’s events and market view

Today’s IFO is expected to confirm the upbeat assessment of yesterday’s PMI. Any anecdotal detail on prices would be of particular relevance to the way markets price future ECB action. This being said, there is more than even chance that investors’ focus remains firmly on geopolitical tensions.

In the US, house prices, PMIs, and Richmond Fed index will be the main releases. The US Treasury will auction 2Y T-notes.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more