Heading Into Jackson Hole With Record Duration Risk

One look at the markets today, with the S&P 500 making a new all-time high and Europe enjoying a 10-day stretch of consecutive records -- the longest since 1999 -- and it is abundantly clear that complacency reigns. But not everyone is convinced that they should put their entire retirement account in deep out-of-the-money S&P call options.

One is Goldman Sachs (GS), which last weekend warned that "the ante will be upped when taper begins," leading to an adverse market outcome. Another is Bank of America (BAC) whose chief equity strategist Savita Subramanian published a note warning that the duration risk heading into Jackson Hole, where the taper announcement is likely to be made, is at an all-time high.

So while there is good news -- with forward S&P 500 EPS tracking +27% year-to-date and the 10-year yield dropping 40 bps since March’s peak, thus pushing the ratio of S&P dividend yield vs. the 10-year yield back up to 0.95x, its highest level since February and back in-line with the post-GFC average -- risks still loom ahead.

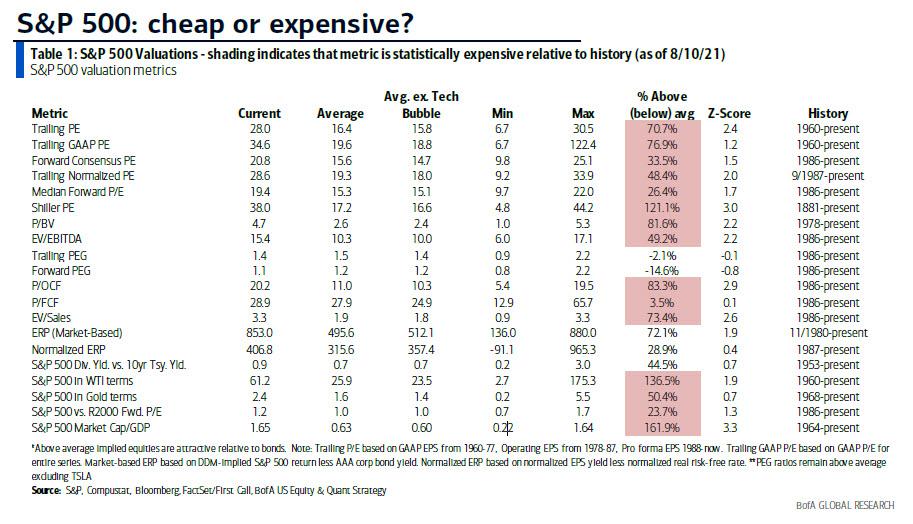

For one, earnings growth is sharply moderating in 2H amid inflation and a slowing economy, plus "record equity duration pointing to painful downside if rates move even modestly higher." In fact, as Subramanian admits, "the market today is statistically expensive on almost every measure of the 20 metrics we track, except on growth and relative to bonds."

So back to the Taper: how does BofA quantify the risk from the upcoming Fed slowdown in TSY and RMBS purchases? As Subramanian notes, more Fed officials are urging tapering, and implied volatility picked up after Friday’s strong jobs report as investors await commentary from the Jackson Hole conference (Aug. 26-28) and FOMC meeting (Sept. 22).

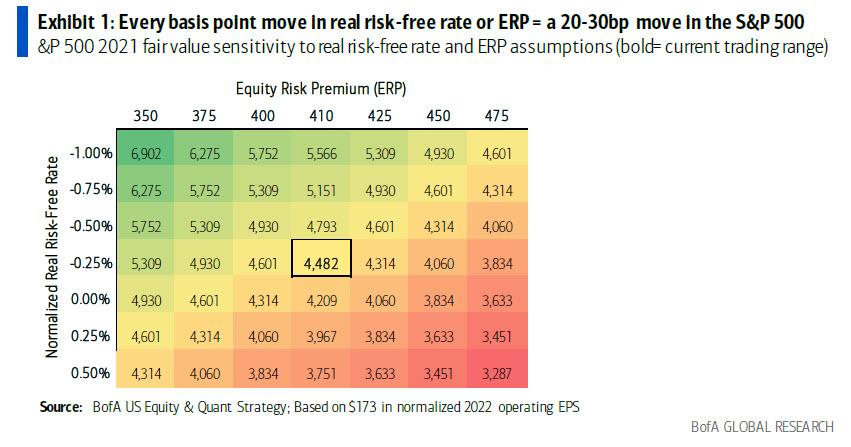

In this context, the bank's Fair Value stress test suggests that every 1 bp change in real risk-free rate or ERP would translate to a 20-30 bp move in the S&P 500.

So unlike other banks who have rushed to hike their S&P forecasts as the market has ground higher, BofA remains a lone bear, and its house view of 1.9% on the 10-year yield by year-end (up +55 bps from today) would translate into a ~15% price drop in the S&P 500.

While that may not sound huge, considering the amount of margin leverage and negative gamma in the system, a 15% drop would likely feel like a major crash to most margined market participants.

Disclosure: Copyright ©2009-2021 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies ...

more