Image Source: Pixabay

The worst year for bonds since at least 1975 has prompted plenty of investors to abandon the asset class. However, of those who are sticking around, a great number are swapping from mutual funds to exchange-traded funds (ETFs) in execution of loss-harvesting tax strategies.

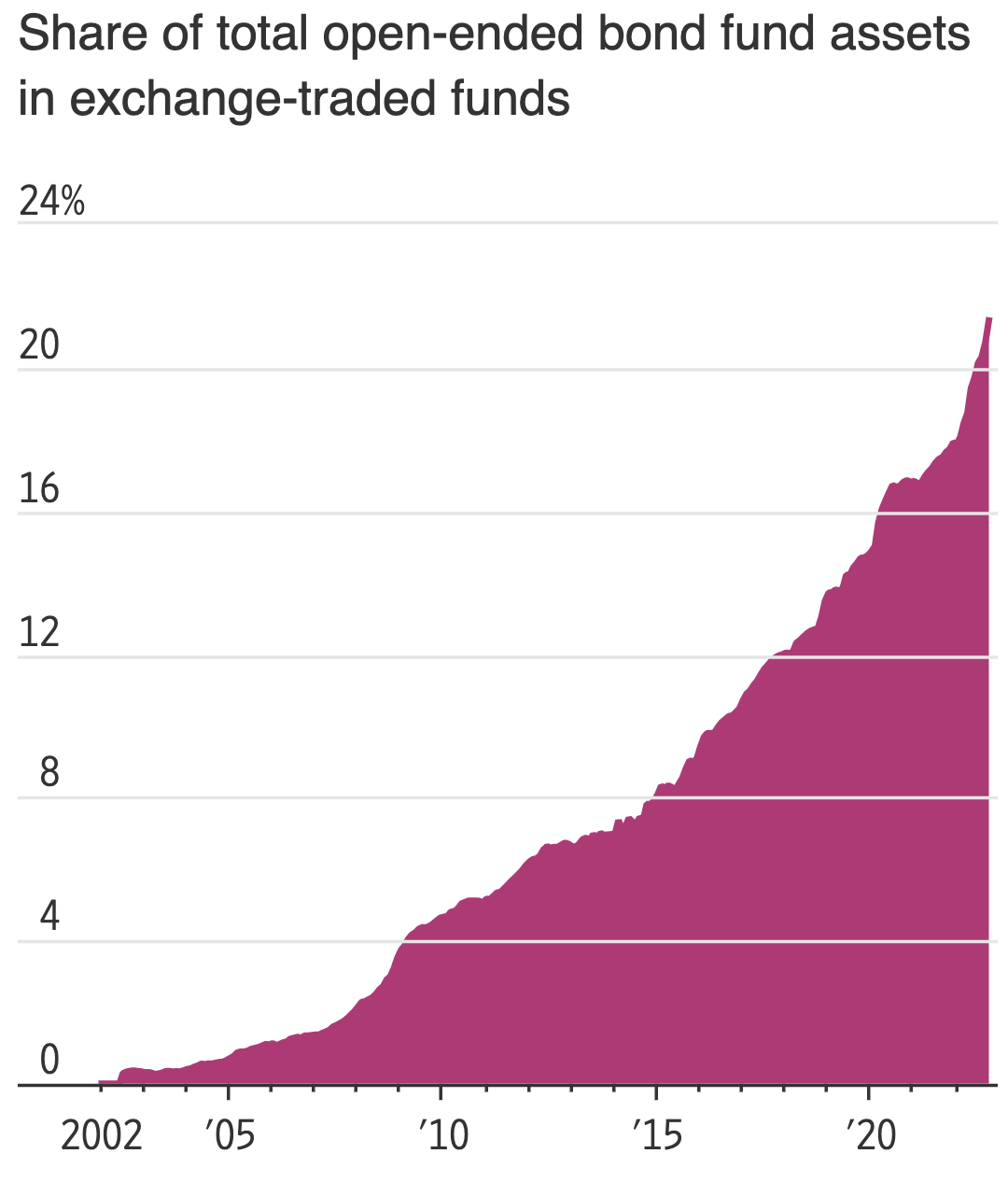

Amid this mass wave of so-called "wrapper-swapping" -- reallocating from a mutual fund to an ETF in the same broad asset class -- ETFs now comprise a record-high 21% of bond fund assets, according to a new report from The Wall Street Journal. That's around double the share ETFs had six years ago.

Through Oct. 31, 2022. Wall Street Journal chart sourced from Strategas and Investment Company Institute

The bond market beatdown has "set off the acceleration of wrapper-swapping that we have seen in equities for a while," ETF strategist Todd Sohn of Strategas tells the Journal. "Now we’re finally getting it in bonds.”

Many investors have been stunned by bond funds' failure to buffer portfolio returns in a rough year for equities. While the S&P 500 is down 17%, Bloomberg's aggregate U.S. bond index is off 11%.

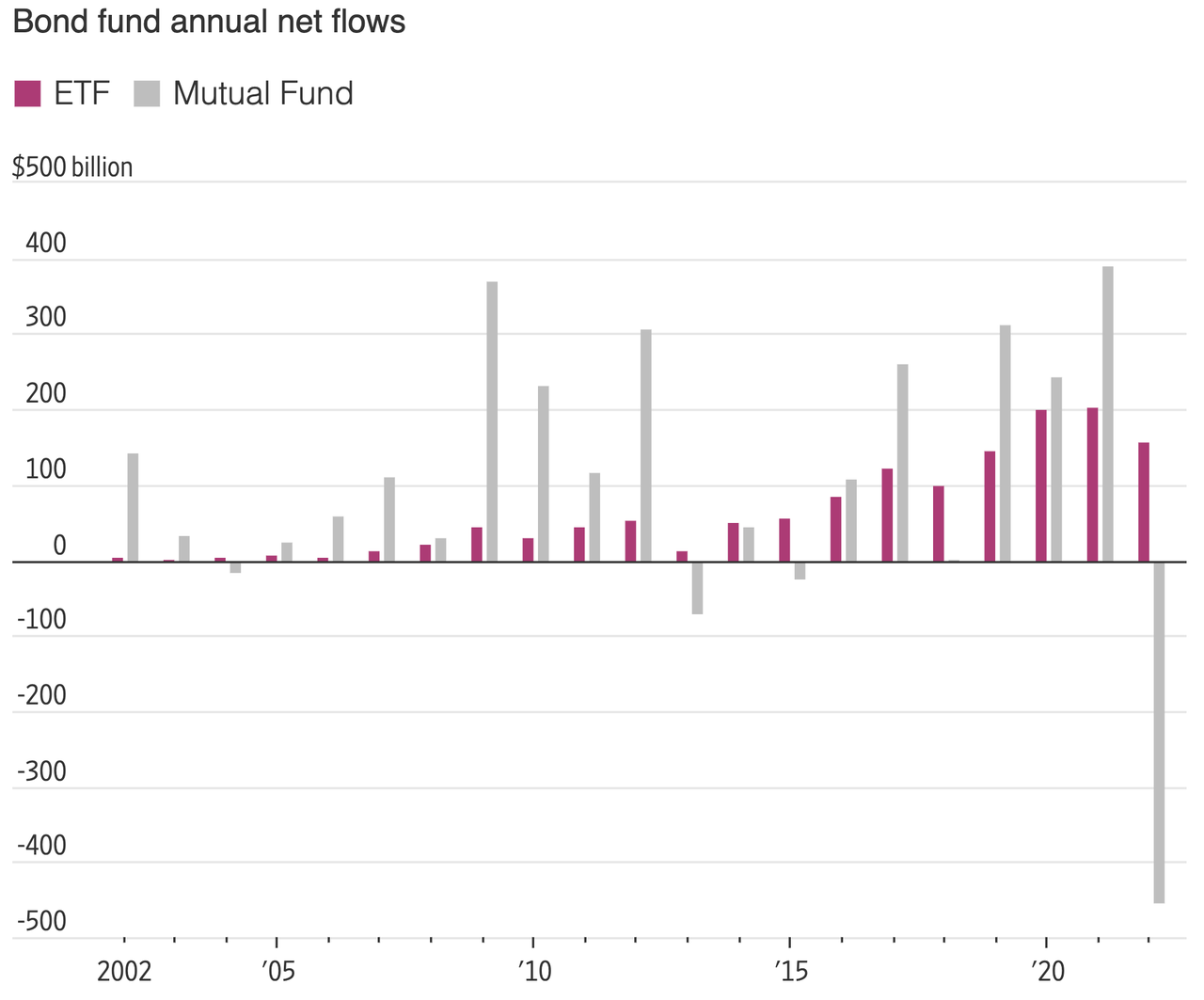

Bond mutual funds have seen net redemptions of a whopping $454 billion this year, but bond ETFs have drawn a net $157 billion -- by far a record swap.

Through Oct. 31, 2022. Wall Street Journal chart sourced from Strategas and Investment Company Institute

As investors wrapper-swap, many are shifting their bond allocation to emphasize U.S. Treasury debt, jettisoning stakes in riskier bond asset classes as worries over the country's economic health mount. Almost 60% of bond inflows at iShares have gone into Treasury funds.

Taxes are a big driver of the trend. By redeeming losing bond positions held outside of 401(k)s, IRA, and other tax-sheltered accounts, investors can realize capital losses and improve the bottom line on their upcoming 2022 tax filings.

Before you swap wrappers, beware of IRS "wash sale" rules, which disallow the recognition of capital losses if the investor replaces it with a "substantially identical" investment during a window that extends from 30 days before the sale through 30 days after.

Caution is required even when swapping from a mutual fund to an ETF -- as there are no clear IRS rules on what constitutes "substantially identical."

The more your choice of ETF differs from the mutual fund you sold, the better your chance of passing IRS muster. For example, selling Vanguard Total Bond Market Index Fund and swapping into the Vanguard Total Bond Market ETF within 30 days is almost certainly asking for trouble.

More By This Author:

Store Credit Cards Hit 30% Interest Rates As Consumer Balances RiseMicrosoft Slides After FTC Blocks Activision Deal, Drags Market Lower

Feds Probing Bankman-Fried's Manipulation Of Terra USD, Luna... Which Eventually Crushed FTX

Comments

Log in or sign up to join the conversation.