Bank Run, Or Run From The Banks?

Our nation’s economic conditions have been influenced negatively by a viral lockdown of overall industry such that many of its component parts are in dire financial straits, and a large portion of the labor force is not earning an adequate income.

This has easily understandable consequences to our overall national economic fabric. For example, as individuals have less or even no earned income - it implies reduced spending on their behalf, which for a consumer–based economy has notably negative consequences. Also when a lockdown occurs people cannot and do not spend as much money – so our consumer driven economy is debilitated.

Lower consumer spending also means reduced revenues and profits for manufacturers, distributors and marketers. Lower income for both individuals and companies necessarily means lower taxes collected by local and national governments, usually weakening their capabilities for stimulative fiscal policies.

Lower consumer incomes also mean that credit card, auto and mortgage loan defaults will rise – as indeed they have risen over the last several years and are likely to rise further. The inability of consumers to pay rent will cause owners of rental properties to default on their mortgages. Lower corporate profits suggests that available bank company credit lines will be tightened, and corporate bond defaults necessarily rise. Local, state, and national governments collecting fewer dollars in taxes suggests that their borrowing has to increase, heightening the concern also over such more significant bond defaults. None of this is rocket science. Corroborating this with pithy charts or tables is now unnecessary and unproductive – as such data has been ignored by investors for a decade or more, while the Federal Reserve has been flooding the country with newly created, inflationary money. Individuals, companies, and governments believe that they will always be bailed out by Fed money easing policies! But quite the opposite is the truth: debt and Fed money printing is now destroying both money and the economy.

Bank runs

Bank runs used to relate to banks having made imprudent or risky loans, which does not have enough cash income to service the demand of its clients. When rumor or fact of such a potential event became known within the bank customer base or its community, customers ran to the bank to take out their deposits in cash. Indeed, such intensified demand for dollars on any bank, solvent or not, could within a fractional reserve system cause it to fail.

Having briefly described our current economic scenario, one could reasonably ask when is the next run on any single or all banks in the FED system going to start? The FED has made it known that they will provide all necessary liquidity to any exposed bank, signaling to depositors that no real bank run failures will be allowed. But is this really true? Perhaps it is only half-true and half deception. If a bank is neither collecting interest on its consumer or commercial loans, nor is able to retrieve its principal because of consumer or corporate bankruptcy, no amount of liquidity produced by the FED can keep the bank viable, as trust in its operations and management is destroyed. It is possible for the FED to bail out a couple of banks – but it is not possible to float the whole failing inordinately extended debt system. In fact, a broader view beyond America’s borders suggests that the whole world is drowning in debt and the banking system is beyond reprieve.

Interestingly, the banking system’s current interest and embrace of digital currencies is driven in part to create a system which can immediately “summon up” whatever amount of “currency” is required just by a few taps on a keyboard – not the actual paper cash that depositors have demanded in a traditional bank run. Therefore, once the banking system evolves from paper currency to digital money, a traditional bank run is no longer possible. In addition, regulations have been enacted which classify bank customer deposits as junior liabilities for banks, which allows banks to seize customer accounts in the event of a bank capital emergency. These conditions now make a traditional bank run impossible, and instead expose the bank customers to financial loss. This uncomfortable truth makes appeasing statements by bank regulators deceptive.

Run from the banks

The depressed condition of virus-affected commercial loans defaulting on a large enough scale will cause bank failures. Be mindful that inadequate capital at banks will allow them, based on current banking law, to seize customer funds. If a bank’s existence is not related to unwise lending practices, speculation, and excessive leverage, but that risk has been offloaded to the customer - it is wise for the customer to run, not walk, as far and fast as possible from the banks custodial service role. Sadly today, all banks are deficient in regards to protecting depositors, and customers should consider taking their money to safer havens.

It is already visible that alert bank customers have been exactly doing that. One sign of common people’s perceptive and self-protective vision is that they are borrowing funds or refinancing to low interest rate mortgages. Intuitively, they understand that it is better to borrow money for the purchase of hard assets such as real estate, than to leave money on deposit at a bank essentially earning zero interest which is exposed to loss of purchasing power or a failing bank bail-in. They also understand that as more money is conjured out of thin air, their real loan value is being reduced by continuing inflation. So borrowing fake fiat money to buy real assets is an insightful and wise financial self-preservation strategy.

This is also the underlying logic for people to buy and hold precious metals such as silver and gold coins. Despite decades of stealth government suppression and manufactured flash crashes of gold and silver markets, precious metals have protected and preserved the savings of people against the loss of debt issuance and money-printing based loss in the currency’s purchasing value. Today, many people no longer believe or trust in the government to protect their money, so they will not turn in gold coins to a bank or government agency as they did in 1933.

Another perceived but volatile haven to protect against the loss in value of depreciating fiat currencies is to buy cryptocurrencies such as Bitcoin. Despite dramatic volatility of market price, Bitcoin has thus far created profit or even wealth for its buyers when compared to the dollar’s (or a multitude of foreign currencies) declining purchasing value, or confiscation potential from failing banks. As Bitcoin has declined about 40% from its recent high, the U.S. Dollar has declined 98% since the founding of the Federal Reserve.

In order to scare the public away from cryptocurrencies and to enhance the public’s commitment to government paper currencies, banks or government agencies will likely cause the volatility of cryptos to grow and prices to fall, so as to shake the public’s growing confidence in cryptocoins as a store of value. Therefore, any near term crashes in the crypto currency market could be related to some agency of your friendly government which wants to keep people from adopting democratizing and decentralizing assets – just as it has happened in the gold and silver markets for decades. With the crypto asset market’s small size, and 100X leverage provided by derivative contracts, this is not difficult to achieve, so expect some crypto market turbulence over the next several years.

Sanctions, and cryptocoins

The world has moved somewhat from applying exclusively kinetic weapons and force to threatening economic competitors, and destruction of its perceived enemies to using less lethal but highly effective monetary weapons. Note America’s weaponizing and use of the global SWIFT monetary transfer system to its geopolitical advantage by mandating penalties to banks or businesses, or denying SWIFT’s use for trade payment to uncooperative countries or those seeking an independent course of action. For example, U.S. sanctions blocking countries from using the SWIFT system have made it nearly impossible for Iran to sell, trade, pay for or receive funds for oil or other product sales, collapsing its currency and impoverishing the country. See: Iran: Public Image Versus Historical Reality Part 2. Iran: The Last Century to the Present.

The United States should want dollars to be used as widely as possible in international trade to maintain its dollar use dominance, but sanctions on Iran, Russia, and other countries are creating negative drivers to dollar usage. Using the SWIFT system as a financial weapon may have desirable short-term geopolitical results for the U.S.; longer term it simply encourages the diminishing future international use of the dollar resulting in substantially reducing its purchasing value domestically.

Sanctions on Russia have prompted them to create their own money transfer system, giving them instead the option to unilaterally terminate its relationship with SWIFT. Russia’s ability to exit from the SWIFT system has an important unstated message to the world. Russia, China, and Iran now feel economically and militarily strong enough such that they can leave the SWIFT system unilaterally because they have a system they can use among themselves - which excludes the use of the U.S. dollar. In other words, Russia instead of being exposed to US sanctions related to the SWIFT system is now taking actions which show that it can make independent decisive action on the world financial stage. For information on Russia since the collapse of the Soviet Union See: Russia – Without the Propaganda –Part 2: The Rise of Putin.

Many countries of the world have been embracing blockchain and cryptocurrencies more fervently than the United States. The US banking industry, the FED, and regulators don’t view cryptos the same way as foreign countries because its adoption diminishes America’s hold on the current financial system and world hegemony. Indeed, cryptos are a clear and present danger to the established banking system and US currency-based dominance of the global finance. Accordingly, there is a challenging balance to maintain between necessary or permissive-enough regulations in the U.S. to be adopted, which will allow blockchain and cryptocurrencies to develop domestically, such that foreign countries do not maintain a regulatory-incentivized development advantage – as they also try to maintain its established legacy order and power of banks and the FED.

Cryptocurrencies can also be perceived as a monetary weapon - one that competes with traditional fiat currencies. Therefore, governments and legacy banks feel the need to control or destroy these decentralized platforms. However, technology is disrupting all pre-existing business systems, and the banking system cannot escape the disruption either. The nation’s malls are collapsing as shoppers switch from mall sales to on-line sales, and as some preppers migrate from gold as anti-inflationary haven to buying Bitcoin as the new and possibly improved haven asset. In this disruptive tech environment banks cannot escape the disruption, and many will disappear.

In addition, the effect of sanctions will evaporate altogether when the world exclusively uses central bank digital currencies (CBDC) for payment or settlement, and cryptocurrencies continue to gain adoption. This is because CBDC and cryptocurrency payments are peer to peer and decentralized, without any centralized bank intermediary which could be controlled by a single country. Overall, it has the potential to bring forth to our world the democracy that the United States has been claiming it was seeking to establish by military means around the world for the last sixty years. It seems that country sovereignty and nationalism can be enhanced by blockchain and cryptos - contrary to what may be the case for citizens within the boundaries of a specific country.

Inflation?

According to the Mises Institute, the year-over-year growth in the money supply as of January 2021 was 38.6%. Additional proposed infrastructure spending is planned by the current administration this year. What happens to the value of the dollar if there is another comparable emission of debt and new dollars in 2021? How will this affect the value of financial markets, gold and cryptocurrencies? How will it affect statistical reporting for money and price inflation?

The Consumer’s Price Index (CPI) has been our most accepted national measure for increasing prices. But, who determined that it was correct to include certain expense items in a government agency’s computation of the CPI, and to exclude others? Who benefits from this particular definition of price inflation and its calculation? Realistically, cost inflation is the effect of the issuance (inflation) of new or additional currency into our economic system. Arguably, cost inflation should measure all increasing prices to which a consumer is subject to. If consumers buy homes or invest in stocks, then these costs should be reflected in an honest calculation of price inflation. But, they are not. So is the CPI actually not deceptive about the true level of cost inflation?

Are CPI government statisticians expecting people to never buy a home, nor ever to purchase financial assets? Not including such items in the calculation of the CPI hides the full price inflation from the persistent issuance of currency within a fractional reserve banking system. This exclusion is particularly egregious since money creation has largely ended up in the financial market rather than in the economy, increasing the gap in income and assets between the already rich owners of financial assets and everyone else. This driver of financial inequality may one day soon give rise to civil unrest and revenge violence.

For a number of years the FED has had an announced policy to increase price inflation. How long could rising price inflation persist, as the public has been assured by the FED very recently that it will be transitory? Well it could be as short-lived as when President Nixon stated in 1971 that “we are temporarily closing the gold window”. An event which confirms the quip that “nothing is as permanent as a temporary government program”.

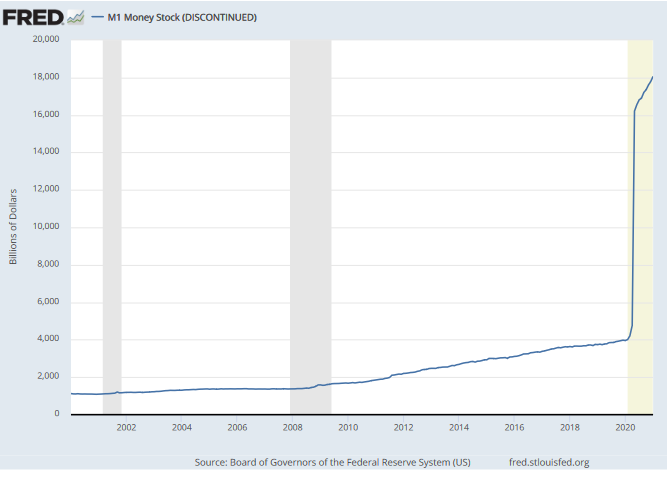

In addition to the understating of an actual level of price inflation, agencies have been discontinuing the reporting of important economic data. The most recent and astounding denial of financial information has come from the FED’s discontinuance of reporting M1, the most basic measure of currency in circulation. The fact that this drastic step had to be taken, so that the public observers of FED money printing malfeasance could no longer be tracked and reported on a consistent basis, shows just how desperate the FED has become. Our economy has been increasingly manipulated with drastic actions by the FED ever since the financial crisis of 2008! If over this time period the economy could not normalize – it really means that it is never going to recover fully – and we will first have to experience its actual demise. It is only after a crash, a new monetary system, with diminished military geopolitical goals, and limited social entitlements that the nation’s economy will be able to rise again.

Here is the important chart which shows that the original M1 measure of money stock has been discontinued. It also demonstrates that money growth has been on a tear. If we take the years 2000-2020, the growth of money has compounded at about 15.1% - a highly inflationary rate for so long a time period. And if we look at the growth of money stock from 2020, which reflects the 38.6% rate cited previously - that growth is simply destructive to an economy and its currency!

According to the FRED’s website, it states “In late February and early March of 2020, the Fed cut its policy interest rate dramatically to help ease credit conditions during the COVID-19 crisis. The resulting acceleration in the supply of M1 can be understood largely as banks accommodating an increase in people’s demand for money.” Should that be interpreted as a walk, jog, or run on the banks?

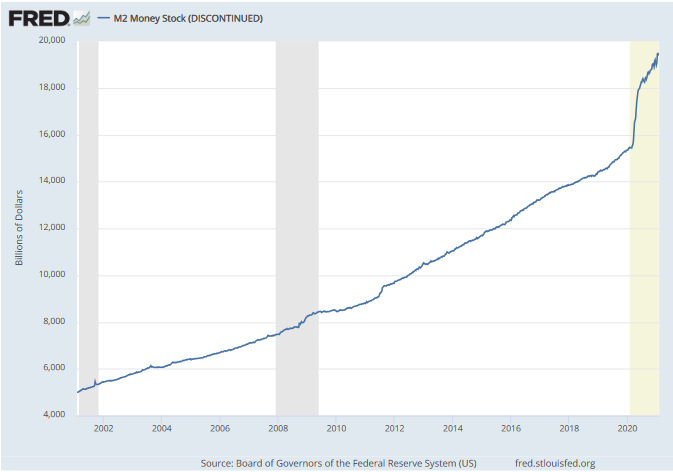

Another measure of the money supply adds savings deposits to M1, which is known as M2. From the graph shown for M2, and data, we can calculate the growth rate of M2 for the 2000-2021 period at 6.6%, also a very high rate or growth – far in excess of the 2% inflation that the FED has announced to seek.

Unfunded government spending is continually accelerating the collapse of our dollar’s value. As a result, anyone depending on it for sustaining one’s quality of life will be disappointed – the quality of life will fall proportionately to the loss in the value of that currency. Increasingly, it is not that people don’t have savings or money, it is that currency has diminished value. Indeed, the value of people’s fiat savings will simply drop, likely forcing them to sell other real assets for sustenance. This is not a constructive basis for a recovery or a dynamic world leader economy.

Protection from Leviathan and central banks

By using crypto currency such as Bitcoin, which cannot be eroded away by corrupting government policies or FED money expansion, people can protect themselves from currency debauchment. While cryptocurrencies such as Bitcoin (BITCOMP) or Ethereum (ETH-X), due to their volatility appear risky, at some point soon it will be more risky to be out of the crypto market than to be in it. Also, continued expansion of debt and money creation is one sure and important driver of rising crypto prices.

Our government never advised us to buy gold (as even Communist controlled China did for its citizens), and they will not advise you to buy cryptocurrencies. Understand that no government will protect your assets, and you yourself must become informed enough and be responsible for such value protection. You must determine now how a run on the banks or a run from the banks is likely to affect your savings.

Could Americans become victims of hyperinflation? Let us first have a common understanding of hyperinflation – it is the rise of prices by at least 50% per month. That means that by the end of one year of hyperinflation prices would have risen by 86 times! So it is likely that we will not experience hyperinflation. However, at a less elevated rate of 10% per month, prices by the end of a year would have risen by nearly three (2.9) times. Given the 15.1% growth in M1 since 2000, or the 6.6% growth rate in M2 in the 2000-2021 period (take your pick), an 8% monthly rate of seems more reasonable – yet it would rise prices by 2.3 times by the end of one year. That would still be enough to destroy America’s economy and its currency – and its global leadership.

Expect government, and the banking system including global central banks of the world to fight hard to establish rules that will maintain their money issue dominance over its citizens. Neither institution will give in to system that they cannot control. However, technological disruption will make most banks irrelevant and thereby force and accomplish the change. Since cryptos allow everyone to be their own banker, the sum of world humanity could thus be emancipated – freeing people from the centralized banking powers in urban areas while also providing a payment system in rural areas where branch banking never existed. That is truly empowering.

Lies

History provides many examples that lead one to question the veracity of any announcement of a government official. Just consider this intentionally short list of proclamations: The constitutional definition of money being “nothing but gold or silver” (or even a gold-backed currency) long ago became a lie. When the Federal Income Tax Act was passed in 1914, the tax rate was set a 1%. Looking at it just a few short years later, it too became a lie. Our government officials stated that we needed to stop the global expansion of Communism – as a result wars in Korea, Vietnam and many other smaller and weaker countries followed. But we actually needed to stop socialism and communism in our own country – all that war expense, destruction and suffering was unnecessary. Many years later FED Chairman Bernanke said that the problems in the 2008 sub-prime mortgage market were transitory and not a danger to the economy. One could debate even today whether the economy ever recovered from that crisis. Now similar comments from the FED are intended to assure the citizenry. Are these statements true, or at least intended to be true, or are they “necessary lies”? In a moment of truth, during the Eurozone debt crisis Mr. Jean-Claude Juncker, the European Commission president stated “When it becomes serious, you have to lie.”

Necessary lies are those which government and central bank representatives must convey to the public via the media, arguably for citizen good. That is, no public official can or will tell us the truth on the economy or war campaign, if stating it would start chaos or incite public mayhem or riot. Lies are also necessary to maintain social or geopolitical programs that are nor supported by the public. Accordingly, we should not condemn these officials for lying to us, but simply understand that the rules by which they must operate makes willingness to lie convincingly to the public a condition of employment.

There are many erudite and credible men and women who have commented on the faulty actions of central bank and government policies in the past. One such person is George Gilder, who should require no introduction, as he is one of the leading economic and technological thinkers of the past forty years. In his book entitled “Life After Google” published in 2018 he observes: “The U.S. Federal Reserve’s inflation “target” is currently 2 percent a year, a program of massive ultimate devaluation. As socialism advances in many countries, debauching their currencies, people incrementally flee to the one global and relatively secure haven accessible through the Internet. Traditionally the haven currency was the U.S. dollar, but since early 2018 –from Greece to Venezuela, from Argentina to Zimbabwe – the haven has increasingly been bitcoin.” So this is a global movement, rather than domestic, in an adoption of the new noninflationary blockchain crypto currencies. As the technology is still developing and will evolve over the next decades, it is impossible to know which or how many different cryptocurrencies will flourish. It is certain that governments and central banks will try to snuff out such independent value creation – by any means. Mr. Gilder’s insight is invaluable as he observes: “Political idealists project visions of liberation onto it; establishment elites heap contempt and scorn on to it”. So who will you believe as telling the truth?

The internet was originally designed to be a decentralized forum, which was quickly captured by large commercial interests centralizing the access to that space. The more recent development of blockchain-based trustless computer platforms by libertarian minded systems analysts and coders, which allow value to be transferred directly peer to peer without the necessity of a third party participant such as a fee charging bank - liberalizes and empowers globally all participants of this decentralized system.

Central banks and their captured governments have been at the core of centralization regarding control of money and even society for well over a century. Its activities have been private and not subject to government audit, yet its trail of money issue, inflation, financial suppression are fully available for the public to see, and which people have personally experienced. Now central banks are ready to adopt digital currencies, which because of low transaction costs can improve banking profits greatly, even as fees to customers can be reduced. But bank digital currencies are subject to full control by the issuer, capturing privacy and freedom of action of all citizens. As this gigantic technological development battle between liberty-minded innovators and established centralization-loving leviathans takes place, are you expecting to see a run on banks, or are you running from the banks?

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and ...

more

Transitory Inflation? More like permanent intentional inflation to save their banker friends. Bitcoin better than gold??? That is the biggest lie ever told, I think. Bitcoin price is as unstable as it's claimed actual value, which does not exist, except in the minds of the holders.