Introduction

On February 19, 2020, the US stock markets were soaring amidst an 11-year bull run with the S&P 500 reaching 3,386. After the pandemic effects started to surface, the market made the fastest swing to bear market territory in the history plunging a record 34% in just a shade of five weeks. Post the low reached on March 23 which coincided with the Fed's announcement of the massive expansion plan which sent the equities soaring a massive 17.6% in the three days following the announcement. Following the initial bang, the stock indices have recovered rather magnificently with NASDAQ reaching all-time highs and currently, S&P is just a shade below its February High. Given the country is facing the greatest pandemic and the worst economic contraction in over a century, are the markets really in a bubble, filled with euphoria and decoupled from reality?

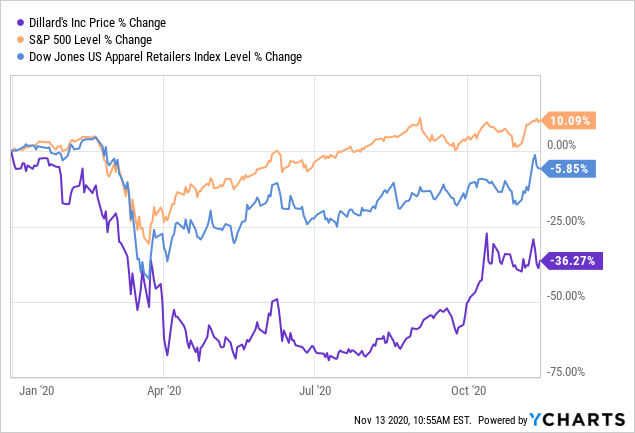

Data by YCharts

Do not fight the FED

The Fed and Treasury, which are known for being lagging, had acted rather too swiftly and dramatically pumping trillions with Powell's reassuring the market that 'We will not run out of ammunition'. The Fed said it will continue to buy securities for as 'long as it takes' with little concern shown towards any ballooning deficit as the Fed has clearly stated their goals on propelling the COVID-induced economy under a shutdown. Along with this, the lower interest rates primarily create cheap liquidity which eventually propels asset prices when invested in that. Apart from that, the Fed announced that the interest rates are not going to see a rise until 2022 which means the continuation of cheap liquidity as well as lower yields which means it would offer less competition to the stock markets. As the popular saying goes, "There is no Alternative to Stock (TINA)".

Flattening the Curve

Investors had been increasingly taking solace in the declining number of positive cases and deaths, after the massive outbreak which many feared would lead to massive shortages of hospital beds and PPE and an immediate 'second wave' as the reopening begins, which was not the case. In retrospect, except for a few states, the curve has likely flattened and people are able to come out and increasingly spend which was shown in the consumer spending data in May. To top it that, the US added 2.5 mn jobs with the unemployment rate falling to 13.3% in May, which is although still at a record high, reinforces the view that the worst is likely over. Along with that, markets are increasingly optimistic about the vaccine and the possible treatments. The stock market is also increasingly skewed towards the heavyweight tech-stocks among the likes of GOOGL, FB, AMZN, which has posted estimate beating results and are at their all-time highs further catapulting the indices higher.

Bears' Take

A vaccine is made out of a complex manufacturing process and the likelihood of getting a vaccine by the end of this year looks grim. Even after the potential candidate proves its clinical benefits and assuming a fast-track approval and usage for the same, manufacturing and distribution is a long drawn-out process. Also, a looming second wave emerges as many states have begun reporting surging infections leading to businesses closing down which would mean the economic recovery may not be that 'swoosh'. The impact of potentially shift in business models for travel and retail industry as well as on office buildings and other commercial real estates could be catastrophic. Along with that, the economic recovery could be longer with several bankruptcies, millions of jobs potentially lost and a large number of small businesses never reopening. The effects of the stimulus by the PPP program could eventually wane out leading to lower consumer discretionary spending.

Conclusion

The panic selling which began at the outbreak of the virus was majorly averted by the Fed and Treasury and put us back on the road to recovery. However, does that hold the justification for the massive 38% jump from the lows to February highs when the economy was humming and the COVID outbreak yet to come? The strong rally was led primarily by the Fed and Treasury injections bringing optimism that it will bring a swifter 'swoosh' recovery with 2022 earnings even higher than the 2019 earnings. While we do not agree with the stock pundits calling a bubble and we believe a bounce from March lows was warranted at some point in time, however, at the current prices, we believe all the positive expectations are priced in and we do not see a favorable risk-reward for investors at these levels.

Comments

Log in or sign up to join the conversation.