If Don Corleone had all the judges and the politicians in New York, then he must share them, or let us others use them. He must let us draw the water from the well. Certainly he can present a bill for such services; after all… we are not Communists.

– Don Barzini, “The Godfather” (1972)

I catch a lot of grief for all of the Godfather references I make, but for men of a certain age it remains the most powerful cinematic if not cultural touchstone we’ve got. It’s also just really good narrative art.

This dinner of the Five Families is the heart of the Godfather story arc. It’s where Vito realizes the scope and power of the plot against him (“It was Barzini all along!”), and where he sets in motion a strategy of revenge and redemption that plays out over a decade through his son, Michael.

Vito Corleone played a mean metagame, the big picture game-of-games that can define a life. Vito was a clever coyote who, unlike most clever coyotes, didn’t allow himself to be blinded by the passion of whatever immediate game was thrust upon him, but was able to excel in the long game. In this case, the really long game.

What drove Vito in his metagame play? What was his motivation?

“I worked my whole life, I don’t apologize, to take care of my family. And I refused to be a fool dancing on a string held by all of those big shots.”

Same.

I was at a dinner of about 20 Epsilon Theory pack members down in Houston last month. I’ve been doing a couple of these meet-up dinners of late, and I intend to do a lot more over the next 12 months. I got a question at this dinner that I had never been asked before, a question that – like Vito’s dinner with the other Dons – forced me to crystallize my metagame.

Hey, Ben, I think what you’re saying about society and politics and finding your pack is really important, and you say it really well. Why are you wasting your time talking so much about markets and investing? Why aren’t you writing full-time about what’s truly important?

It’s a question that I’ve thought about a ton, but never talked about publicly. So here goes.

My goal in all things, but especially my metagame, is to act non-myopically and in a way that treats others as autonomous ends in themselves. It should be your goal in all things, too. You know the drill … Clear Eyes, Full Hearts, Can’t Lose.

Acting with a full heart means two things: acting for Identity and acting for Cooperation.

Or as Socrates would have said, Know Thyself, and as Jesus would have said, Do Unto Others As You Would Have Them Do Unto You.

See, there’s really nothing new under the sun. Everything we write in Epsilon Theory has been written before – and better – by teachers who lived hundreds or even thousands of years ago. All you’re getting here is old wine in a new bottle. It’s just really, really great wine. And a half-decent bottle with Godfather quotes or farm animal stories on the label. You could do worse.

What’s my Identity?

I am a solver of puzzles and a player of games. This is who I have always been, from my first childhood memories. This is my motivation. This is my intrinsic spark and reward. This is my Aristotelian entelechy, to use a ten-dollar phrase. This is my I AM, to use the Epsilon Theory lingo.

The market is the biggest puzzle there ever was. That’s why I can’t stay away.

So in keeping with my Identity and our metagame at Epsilon Theory, today I want to share with you a puzzle that I think Rusty and I are solving. Not solved, because a) that’s impossible in a three-body problem like the market, and b) it’s still early days in the Narrative Machine research program. But we’ve completed enough testing and research to have convinced ourselves at least that we are onto something cool and important.

This is the market puzzle that we introduced in March with this article.

It’s our effort to apply our narrative research to an actual, honest-to-god practical investment question – can you measure the structure of financial media narratives in a way that gives a useful signal for underweighting or overweighting big market structures like S&P 500 sector ETFs?

At the conclusion of that note, after laying out our research thesis and the way we were operationalizing our tests, I wrote this:

So I’m not going to talk about results until I can do it without telling a story, until I can show you results that speak for themselves. It’s like the difference between qualitatively interpreted narrative maps and algebraic calculations on the underlying data matrix … the difference between what we THINK and what we can MEASURE.

I know, I know … kind of a tease. But today I think we have results that DO speak for themselves, so that’s what I’m going to let them do.

First a recap on our test procedures, although I’m going to keep this really brief because you can read more in “The Epsilon Strategy”.

In addition to measuring the Sentiment of each article within a batch of financial news articles (something everyone does and we think is better thought of as a conditioner of narrative than as a structural component of narrative), we also measure the “weight” of one narrative structure relative to all the other narratives within a universe of media – what we call Attention – and the “center of gravity” of a narrative structure relative to itself over time – what we call Cohesion.

These are massive data matrices that we are evaluating, so the narrative map visualizations that we often publish in Epsilon Theory notes should be thought of as tremendous simplifications (2-D flattenings of many-D matrices) of the measurements we’re taking here. Still, I’ll incorporate some visualizations where I can.

For example, on the left is a 2-D visualization of the Attention score of the Utilities sector in December 2014. Every faint dot (also called a node) in the graph is a financial media article talking about the S&P 500 in some way, shape or form. There are thousands of these nodes, of course, clustered by all the different topics that drove stock market narrative that month. The dark nodes, few and far between, scattered among several different clusters, are the articles that are about the Utilities sector.

On the right is a 2-D visualization of the same data query and the same data sources for January 2015. What’s pretty clear even in this inherently truncated visualization is that the narrative Attention paid to the Utilities sector – the amount of media drum-beating about the Utilities sector – is much higher in January than in December.

We think this is a short signal for February 2015, by the way.

To be clear, we have ZERO insight into the fundamentals of the Utilities sector going into February 2015. We are NOT actually reading any of these media articles, and we really DON’T CARE what everyone’s opinion about the Utilities sector might be. All we know is that the financial media is shouting at investors to focus their attention on the Utilities sector in January 2015 … or at least shouting in a relative sense to how they were talking about Utilities in the prior month … and we believe that all this shouting has an effect on investor behavior. We believe that investors probably plowed into the Utilities sector in January 2015, so we want to be short (or underweight) this overbought sector in February 2015.

We came up with eight testable hypotheses like this, based on states of the narrative-world as measured by Attention, Cohesion, and Sentiment, and we ran a five year backtest on each hypothesized strategy for its signals in overweighting or underweighting S&P 500 sectors on a monthly basis. Importantly, we came up with the hypotheses before we did any backtesting or simulations, and we did zero tweaking or retesting after we did any backtesting or simulations. These sector rotation strategies are deductively derived, based on our professional intuition of investor behavior and our professional knowledge of how the Common Knowledge Game works.

Also importantly, these are slow-twitch strategies, where we take our measurements at the end of each tested month to generate a signal for the following month. All of the financial media articles are publicly available. There’s no massaging of the data or change in the search queries over time. There’s no discretionary input. We are testing on the Select Sector SPDR ETFs, each of which have no appreciable liquidity constraints, and we take into account ETF fees in our performance simulations. We do not take into account trading costs, although we would expect these to be minimal.

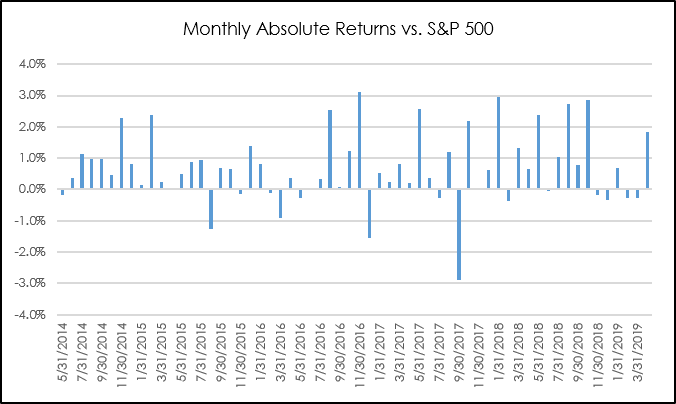

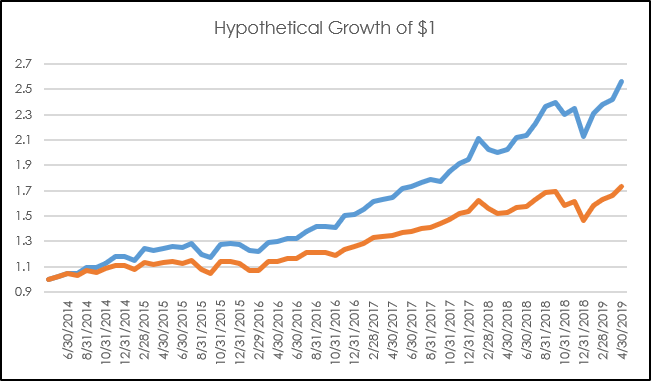

Of the eight hypothesized narrative-driven sector rotation strategies, we found that six of them “worked”, meaning that in our backtest simulations they generated excess returns over the S&P 500 and had an information ratio > 0.6 (again, I’m going to let our findings speak for themselves, so if you need a primer on “information ratio” and some of the other terminology here, that’s on you). We then took a simple, non-optimized equal weighting of each of the six working strategies to create an unconstrained “Beta-1” portfolio strategy, meaning that we let the individual strategies do whatever they signaled as far as underweighting or overweighting the individual sectors relative to their baseline S&P 500 sector weights, and then we added whatever vanilla S&P 500 index long or short exposure was required to make a fixed portfolio net exposure of 100% long. So if you’re keeping track of these things, the unconstrained Beta-1 portfolio of strategies averaged about 12 separate sector signals per month, an average gross exposure of around 200%, and is the rough equivalent of a 150/50 strategy.

Now before I show you the results of the portfolio simulation, I want to say the following really clearly. I’m not saying this as boilerplate, and I’m not saying this in tiny text or in ALL CAPS, both of which are signals for you to stop paying attention. These are simulated, backtested returns. You could not have invested in these strategies. You cannot today invest in these strategies. Even if you did, there is no guarantee your results would reflect those of the backtests I’m going to show you. We have treated all of this as a research puzzle we are trying to solve, and so should you.

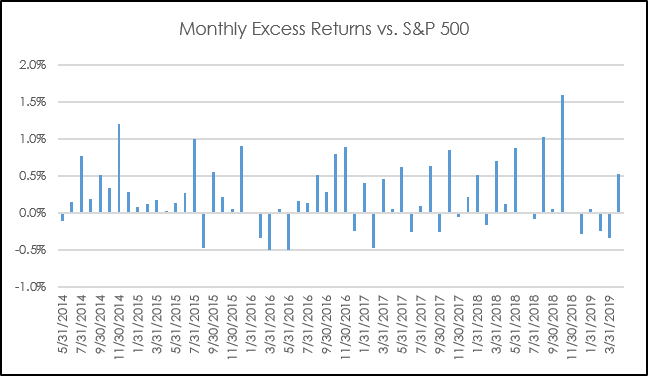

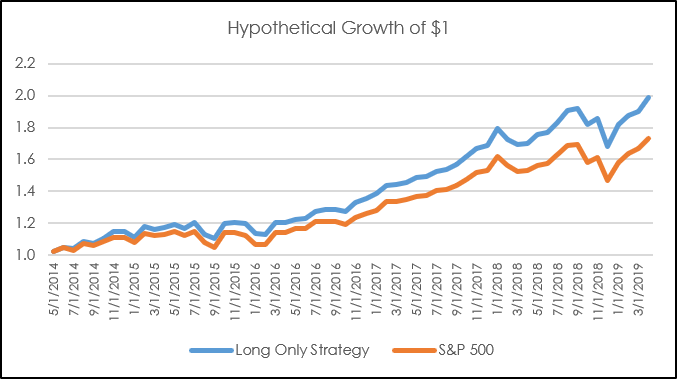

We understand that many investors are not allowed to be short anything, even an S&P sector ETF, so we also modeled a constrained long-only portfolio of strategies, where we cap all underweights at zero exposure, creating a 100% gross exposure, 100% net exposure portfolio strategy, with no shorting of any sector ETF. As you would expect, the performance statistics are muted compared to the unconstrained version, but still quite powerful.

Crucially, these excess returns are uncorrelated to all major factor categories – Momentum, Value, Low Vol, and Quality.

So there you have it.

We think we are identifying a novel and predictive signal of investor behavior from our systematic measurement of narrative structure in publicly available financial media.

Now, savvy readers will note that I started this note by talking about metagames and Identity, but cut that discussion short to get into the meat of this investment research puzzle that I think we are solving. Savvy reader will ask themselves if there’s another shoe to drop here. Savvy readers would be right.

What’s my metagame?

Let’s start with this blanket statement: I will do anything for my pack. I’ll be the patsy. I’ll make unreasonable sacrifices. I’ll give away the store if that’s what’s required. But here’s the thing – my pack would never require this of me. At every level of my pack, from nuclear family to the ET epistemic community, we do unto each other as we would have each other do unto us.

To put it in Kipling’s poetic terms about the pack, we drink deeply, but never too deep.

To put it in Dungeons & Dragons terms, we are lawful good but not lawful stupid.

So hell yes, we’re going to charge money for access to and information about our investment research. Second Foundation Partners is a completely independent company. It’s me and Rusty doing a high-wire act with no net. Our research and puzzle-solving is not only an expression of our Identity … it’s also how we preserve our independence so we CAN write about more than markets and investing.

If you’d like to draw water from this research well, you’ll need an ET Professional subscription. It’s the only place we will be sharing our insights and plans for developing the Narrative Machine for investment applications.

Comments

Log in or sign up to join the conversation.