Upon re-reading my summary of the housing bubble and financial crisis, I suspect some skeptical readers might find my summary lacking because it may seem as if I am writing off what was clearly a boom in residential investment and home building.It may be worth a clarification.

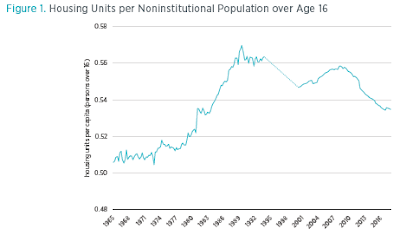

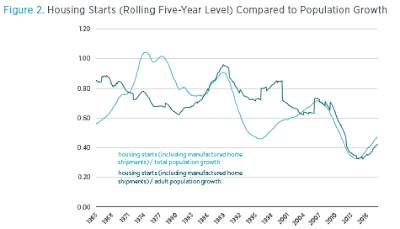

There certainly was an increase in building from the mid-1990s to the mid-2000s.But, in terms of either the number of homes per capita or the rate at which they were being built, nothing was outside of

.Residential investment seemed high, but part of what is accounted for as residential investment is brokers commissions, which don't really add to the housing stock.Brokers commissions were high, however, because the shortage of urban housing made existing homes too expensive.Subtracting commissions out of residential investment reveals a long term decline that was briefly interrupted with rates of residential investment

.

There wasn't really a national building boom.There was a moderate rise in building.The reason it seemed so disruptive is that the Closed Access cities can't allow a sustainable amount of building.

That means that any time Americans try to increase our real consumption of housing at the same pace that our incomes are rising, a disruptive migration event must occur, because if the consumption of housing expands and some cities cannot expand their local stock of housing to accommodate it, those cities must depopulate.That's what happened before the financial crisis.

Policymakers since then, whether they understand it or not, have been trying to avoid this disruption by either keeping incomes low (through tight monetary policy) or by reducing demand for housing (through tight lending standards).That has reduced the migration out of the Closed Access cities, but it has come at the expense of living standards for Americans everywhere.

Comments

Log in or sign up to join the conversation.