Valuations Matter.

As I mentioned briefly in Part 1 of the series, investors about to the enter the retirement distribution phase of their lives or seeking to extract money from a basket of variable assets like stocks and bonds to re-create a retirement paycheck, must be keenly aware of portfolio risk and prepare for a cycle of muted portfolio returns.

Newbies to the retirement experience and those who aspire to retire within the next 3-5 years must seriously consider comprehensive financial and distribution planning to ensure the retirement income paychecks they require are realistic, tax-effective and sustainable over a lifetime.

I passionately believe that people who retired last year and those looking to retire within the next 5 years will need to deal with a tremendous headwind to returns on variable assets. In other words, a traditional portfolio of bonds and stocks will fail to generate the returns and income required to maintain the annual 4% standard withdrawal rate touted by the masses of financial experts.

In addition, financial planning is going to become downright perilous for consumers. Planners and consultants employed by big-box financial retailers are not motivated to adjust downward their projected global stock and bond market returns. After all, it’s not in the best interest of their employers to downplay future returns to sell managed money products. There’s too much career risk for those who want to do the right thing; the responsibility for truth discovery is going to fall on the shoulders of clients of these firms.

Going forward, second opinions must be the standard for consumers of financial planning and asset management, especially those going through retirement preparation. Investors will need to employ a “two-plan strategy,” if their broker (most likely), has not prepared for lower future asset-class returns. Unfortunately, lives will change, but it’s not too late.

On a regular basis, our planners at RIA must re-adjust consumer expectations especially when they come to us for second opinions on retirement plans completed by their brokers. As fiduciaries, our goal is to be objective and help people plan for reality. Market fantasy is dangerous for those looking to re-create a paycheck in retirement.

For example, one of the financial planning programs we utilize has a projected asset class return of 5.03% for a balanced portfolio of stocks, bonds, and cash. Based on our analysis of valuations, we believe future returns for a similar portfolio will average closer to 2.5%. John Hussman, Ph. D one of the finest analysts of complete market cycles is less hopeful. In his market commentary from July 14, “They’re Running Toward the Fire,” he outlines:

“As of Friday July 12, our estimate of likely 12-year total returns for a conventional portfolio mix invested 60% in the S&P 500, 30% in Treasury bonds, and 10% in Treasury bills, has dropped to just 0.5%. A passive investment strategy is now closer to “all risk and no reward” than at any moment in history outside of the three weeks surrounding the 1929 market peak.”

Will there be years when 5.03% is attainable or exceeded? Sure. However, on a consistent basis, we don’t believe it’s going to happen until the current ultra-rich level of stock valuations have been worked off. Thus, a consistent ‘surprise gap’ in expected returns will require investors especially pre-retirees, to consider specific actions:

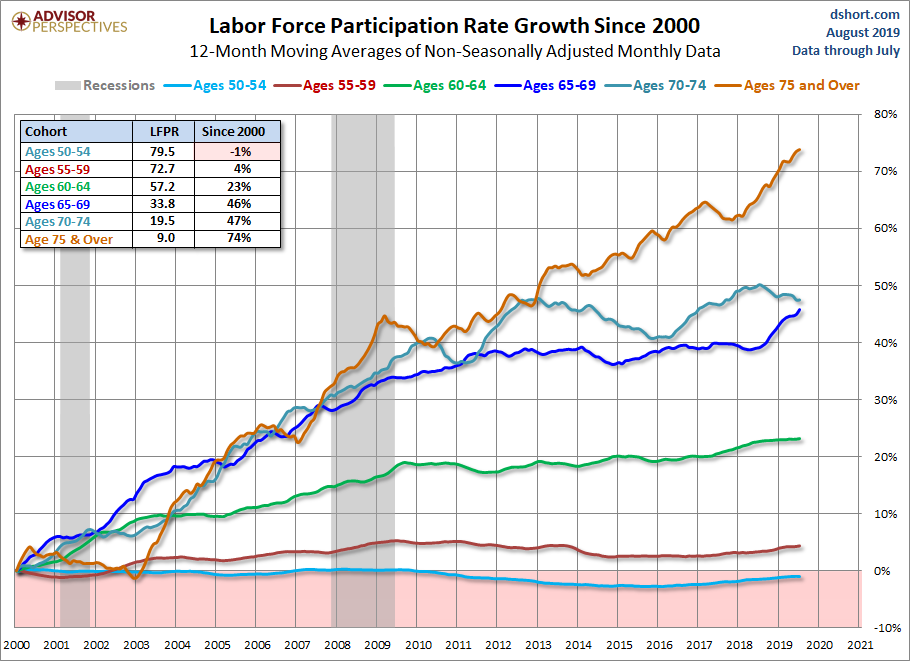

1). Work longer. Retirement at 65 is an outdated aspiration. Today, people are either working longer or returning to the workforce.

Notice the dramatic 74% increase in the Labor Force Participation Rate for 75 & older since the year 2000. For some older Americans, working longer allows them to remain social and engaged which crucial to health. However, like younger cohorts, seniors have utilized debt to maintain standards of living. They have taken on increased credit card debt and co-signed loans for children and grandchildren. In the latest U.S. Census Report, 44.4% of households led by people older than 65 are wallowing in debts.

Per NBER Working Paper No. 24226 titled “The Power of Working Longer,” by Bronshtein, Scott, Shoven & Slavov, the delay of retirement by 3-6 months has the same impact on the retirement standard of living as saving an additional 1% of labor earnings for 30 years. Yea, you read that correctly. We witness the results daily. Those who decide to work longer, even another year (which goes by quick), witness a marked increase in the probability of financial plan success even with our lower projected portfolio returns!

2). Remain unemotional when it comes to planning for potential guaranteed streams of income. Through a period of increased sequence of returns risk whereby withdrawals can have a deleterious impact on overall portfolio returns, a future retiree should maximize Social Security benefits (waiting until age 70 to file), re-consider an employer’s pension options over lump-sum rollovers to IRAs and investigate annuity options such as single premium immediate or fixed-indexed annuities with income riders. Guaranteed income alleviates the burden of a portfolio to bear the full burden of lifetime withdrawal requirements.

3). Rethink expectations. The results of a comprehensive plan can help people gain tremendous perspective of the financial viability of future goals in a world of lower returns; with compromise and a bit of soul-searching, retirement during a period of greater sequence of returns risk can still be rewarding. A reduction of spending on wants like big vacations, a revised definition of expectations and new methods that ensure a quality retirement on a budget should be topics on the table. A fiduciary planner who studies market cycles should be hired to communicate objectively and help you prepare for probable future reality, as unpleasant as it may be, not projected hopes of lofty investment returns.

4). Live smaller starting ten years before retirement. I have helped clients accomplish this task – it works. I have witnessed dramatic downsizing efforts as couples shed large two-story homes and settle into quaint one-story 1500 square feet abodes. I have watched pre-retirees purge most possessions, clean things out, donate aggressively, gift heirlooms to kids who want them, all to live simpler. Lower overhead, adherence to micro or strict household budget, aggressive savings rates north of 30%, along with a redefinition of retirement enrichment can reap formidable results. In other words, without the tailwind of robust investment returns, people are going to need to close the ‘surprise gap’ with their own sweat equity and ingenuity.

Whew. Now, for the valuation metrics that investors especially pre-retirees, should consider.

With the current Shiller P/E at 29x and other market valuation metrics at stretching points, those who are 5 years or less from retirement should act today to reduce portfolio risk.

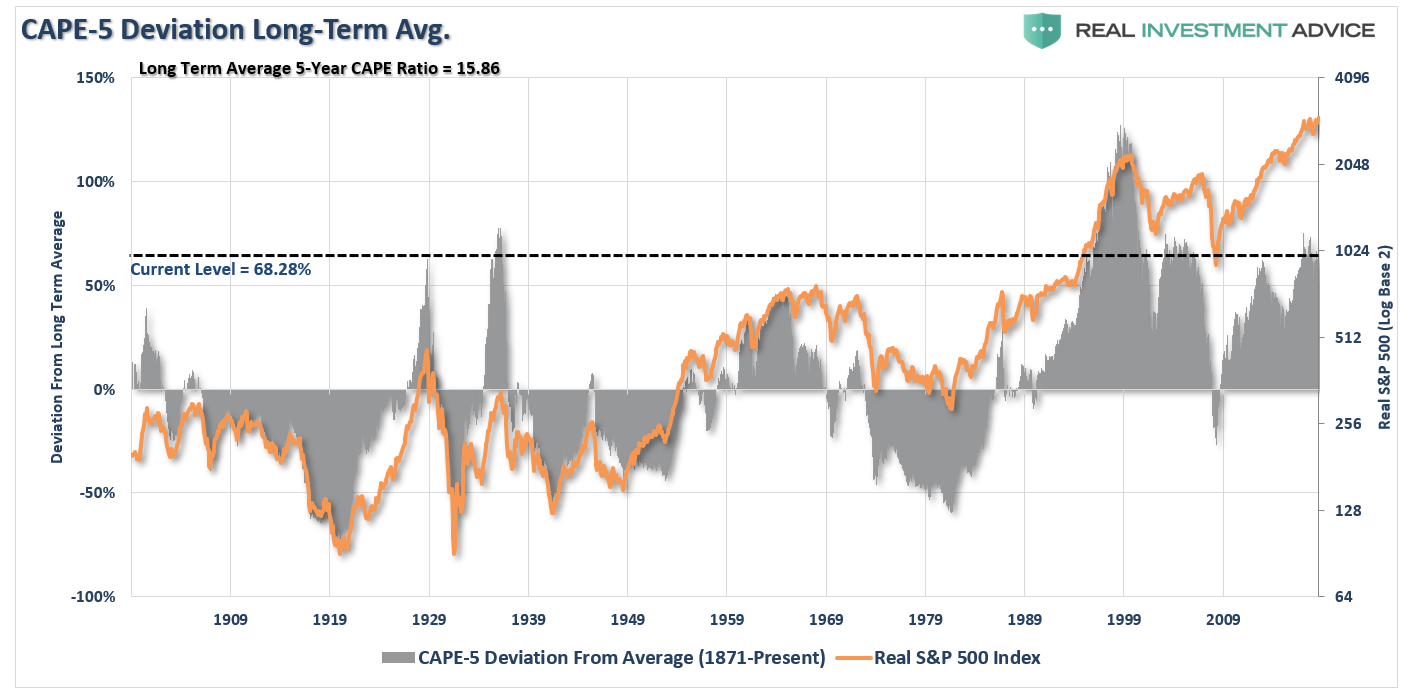

RIA’s CAPE-5, a more-sensitive adjunct compared to the Shiller P/E, correlates highly with movements in the S&P 500.

There is a positive correlation between the CAPE-5 and the real (inflation-adjusted) price of the S&P 500. Before 1950, the CAPE and the index closely tracked each other. Eventually, the CAPE began to lead price. The current deviation of 68.28% above the long-term five-year CAPE ratio has occurred only three times in recent history.

What if you retired last year and began a distribution plan?

I’m surprised to find that many investors still do not realize that markets had a poor showing in 2018. You may be shocked to find out that although S&P 500 returns are higher by 15.23% YTD through August 16th, over the last 12 months the major index has done nothing but tread water.

I have been a proponent of Ed Easterling’s market valuation work since 2010. At Crestmont Research they have created their equivalent to the P/E-10 (or Shiller P/E) ratio.

The Crestmont P/E is now at 33.1 which is 130% above its average.

To maintain perspective, the 33.1x P/E exceeds the Tech Bubble, August, and September of 1929.

Irrational exuberance, anyone?

There are financial advisors and pundits who scoff at valuation metrics. They are afflicted with terminal recency bias with little hope of recovery. I peruse their comments on social media; I listen to their words. The tone smacks of defiant “this time it’s different.” I remain eternally humble when it comes to markets. They are designed to obfuscate the masses. Markets are great levelers.

In all fairness to the doubters, unorthodox monetary stimulus from global central banks along with short-term interest rates being lower for longer, indeed push money into risk assets and manipulate markets. Finally, in a period of sustained negative interest rates overseas and accelerated lower rates domestically, the effectiveness of central bank intervention to move markets I believe, is finally starting to crack which could be the catalyst required to jump-start lower future investment returns. In other words, central banks are employing every tool in the magic box and yet economic growth is faltering and global markets are not as enamored with monetary efforts. It’s ‘pushing on a string’ at its shining hour.

Ruchir Sharma, author of the book “The Rise and Fall of Nations: Forces of Change in the Post-Crisis World,” recently penned an eye-opening opinion piece in The New York Times titled “What’s Wrong With the Global Economy? ” If you have the time, it’s worth a thorough read. Overall, he makes the case that demographics are the main driver of economic growth; let’s just say we should calculate a global “baby dearth rate.”

He writes:

“The benchmark for rapid growth should come down to 5 percent for emerging countries, to between and 3 and 4 percent for middle-income countries like China, and to between 1 and 2 percent for developed economies like the United States, Germany and Japan. And that should just be the start to how economists and investors redefine economic success.”

If the global central bank drug has lost efficacy – If younger generations begin to redefine their own economic success by living smaller and not looking to have children (I witness this in my own Gen Z daughter and friends), if earnings growth remains muted during a period of massive overvaluation as we’re in now, then the probabilities of lower investment returns are going to be a reality investors need to face.

So, what if I’m wrong?

I hope I am.

I hope consumers and clients who come to RIA for planning and investment guidance consistently beat the heck out of their personal investment return hurdle rates and easily meet financial milestones. I hope their biggest dilemma is how to spend more or leave a greater legacy to loved ones and charities.

At the least, even if you scoff at what I’ve written, it may compel you to monitor your annual portfolio distribution rates, be flexible to change them through periods of poor sustained returns, ask more questions of your brokers about how to maximize guaranteed income options including Social Security. Perhaps I’ve helped you get your financial head out of the dirt and propel you to prepare just in case. Maybe I’ve spurred motivation to create a contingency plan that places your household on solid financial footing regardless of how cycles play out.

What if I’m correct?

Time will tell. If correct, I’ve properly tempered expectations. We will not be surprised or need to scramble to have very difficult conversations with clients about uprooting their lives mid-retirement.

Either way – I win. You win, too.

And at night regardless, I can sleep like a baby.

Comments

Log in or sign up to join the conversation.