These Catalysts Could Easily Lead To A Market Crash In 2016

By Damon Verial

[In this article I don't predict]...a hard date or magnitude of the next market crash...[but] merely point out that there are several catalysts [as discussed below] that could easily lead to a large market crash in 2016.

The Cyclical Nature of the Market

One of my main complaints about buy and hold investors is that they fail to recognize the cyclical nature of the stock market, of industries, and of their individual holdings. Just as we know that International Business Machines (IBM) consistently underperforms during Q1 and Q2, we know things about the wider market as a whole. For example, every seven or eight years, the bull market comes to an end, giving way to a (usually) brief bear market.

Low Oil Prices Are NOT a Catalyst to a Market Crash

These days, "market crash" and "oil prices" often come up in the same conversation but low oil prices are not a catalyst to a market crash. This goes contrary to most investors' beliefs, but let me explain.

In the past, low oil prices implied lack of demand. A lack of demand then implies less traveling, less driving, and less production reliant on oil. In other words, low prices equated to low demand for the resource, which is essential to the U.S. economy. Today, however, low oil prices are driven by oversupply, not a lack of demand. So are oil prices important to predicting the market crash? I believe oil prices are not salient here, but a correlated factor, the strength of the dollar, is.

The Strength of the Dollar

A strong dollar is great for the individuals carrying it, assuming you're leaving the U.S.. For everyone else, a strong dollar hurts. Consider emerging economies who see their currencies weakening against the dollar. Yes, exports to the U.S. might increase, but domestic investments on a whole become less appealing.

Instead of investing in the domestic market, citizens in China, for instance, would benefit from taking their money to the U.S. to buy bonds and stocks. This is exactly what is happening in China, despite the government trying to contain the act. The result is more investment in the U.S. and a bolstering of the U.S. stock market.

Realize that this is completely unrelated to the fundamentals of the U.S. economy. The Chinese, for example, simply see the U.S. as the least worst place to put their money...

For the domestic U.S. market, a strong dollar still hurts. Consider the numerous multinational companies that now have to report weaker earnings due to Forex issues. Aflac, for instance, makes 70% of its revenues in Japan, where the U.S. dollar gets me 120 Yen; when I visited three years earlier, my dollar only got me 80. The wave of negative Q4 earnings reports have in part been affected by Forex rates that stem from a strong dollar.

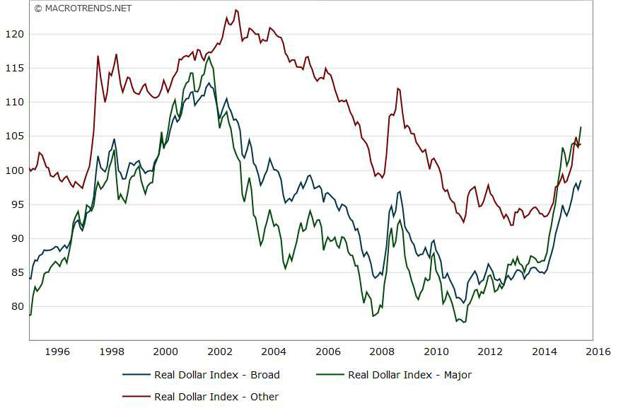

I doubt it is a coincidence that the U.S. Dollar Index has tended to spike prior to a market crash. Look at how the real dollar index (blue line) rose before 2000 and 2008; now look at it today:

Junk Bonds

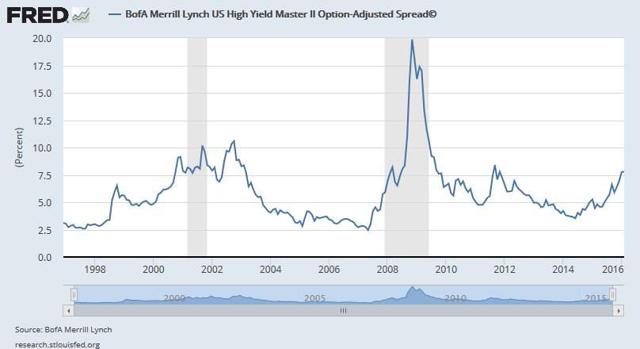

The high yield bond (or junk bond) spread is also informative in predicting bad things to come. In the following chart, breaking the 7.5% line is indicative of a problem. The 2000, 2008, and 2011 crashes were all preceded, or corresponded with, breaking that line:

Notice that we have just broken that line once again. The implication here, in fundamental terms, is that investors are no longer willing to risk loaning money to risky companies without excessive compensation. This equates to a lack of funding for said companies and the result is fewer and lower loans from investors, less spending from companies, and a more stagnant economy overall. In terms of sentiment, investors are no longer willing to take on the risk they were happy to take on during the nice bull market ride from 2011 to now. That is, fear is starting to set in.

Yield curves are known to be a leading indicator of the economy. The stock market can be considered a lagging indicator of the economy because of its heavy reliance on the reports of past performance of the companies involved. Put together, this means that the stock market lags behind the bonds market.

While bond investors have caught on - and are probably ahead of the game, as they are aware of both the bond and stock markets whereas most retail investors only pay attention to the stock market - most investors are still watching only the stock market. If you want to be ahead of the game, take it from the bond investors: Things do not look good at present.

The Market Is Overvalued

...Recently, I have been seeing many overvalued companies and very few undervalued companies. Statistically, I should see roughly 50% of each but this is not the present state of things...[as there are] many fundamental reasons that explain the overvaluation. Among them are:

- The Fed Ponzi scheme of printing money

- Foreign investors having nowhere else to turn but the U.S. market

- Company buybacks

- Bad news being good news

The Fed Ponzi scheme is a bit too political for me to get into, and I've already discussed the foreign investment issue, so let's quickly talk about the remaining two. Let's tackle bad news being good news first.

Bad News Is Good News

Yes, in 2015 and beyond, bad news has become good news - and vice-versa. The Fed raising interest rates hurt bank stocks while lifting the overall market yet banks had the most to gain from increasing interest rates, while the overall stock market had much to lose.

Welcome to 2016, where any governmental attempt to intervene in the stock market is met with good response. Any signs of artificial pumping of money into the stock market lifts stock prices. You only need to look at the market's reaction to the Bank of Japan's adoption of negative interest rates to see this.

Negative interest rates imply a weak economy. However, the U.S. market rallied after the Bank of Japan adopted negative interest rates. Essentially, negative interest rates equate to a stimulus - the government is forcing money to move around, eventually landing in the markets.

The basis of the regulation is not good for the economy but the consequences inflate stocks. Investors know this and go with the flow, taking bullish positions. Any bad news that can be seen in a good light is.

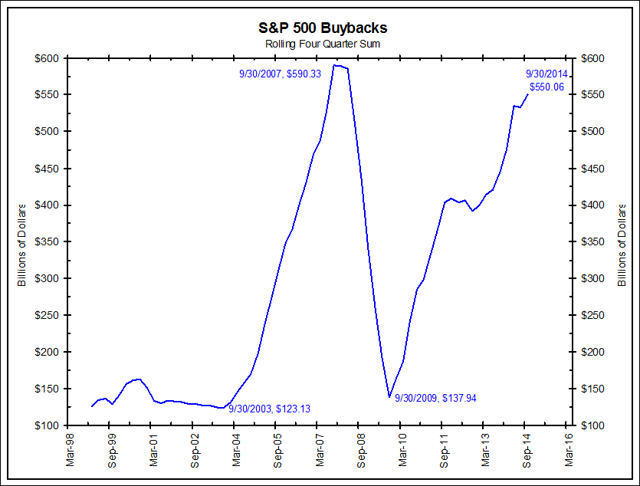

Company Buybacks

Much of the recent past has been characterized by companies not knowing what to do with their free cash flow. The answer comes in the form of buybacks. When companies buy back outstanding shares, they make each outstanding share worth more, thus bolstering the price of the stock. This has led to many inflated prices and, because buybacks are at a relative high, encroaching upon 2008-levels, this implies an artificial inflation of the stock market as a whole:

(Source: Fortune.com)

What Can Save Us?

The same thing that can keep the market afloat in the short term is the same thing that has been keeping the market afloat: More money input in spite of the fundamentals. While big companies lay off employees, the Fed can take taxpayer money and use it as a stimulus. Alternatively, they can re-engage in quantitative easing, shortening the U.S.'s path toward becoming a bigger version of Japan.

I wouldn't put it beyond the government to intervene in the markets, as, after all, it's worked thus far. However, without the fundamentals bolstering the market, we are walking a thin line. Once investors begin to see that the market lacks reason to be this high, they will start pulling their money out, creating a dominoes effect that hits other investors, hedge funds, and the algorithms that constitute half of the market action.

Ultimately, however, nothing can hold the market up for a longer period sans (without) a true fundamental change in the economy. Such changes do not occur quickly. The only remaining solution for the current market is a series of corrections - or all the corrections at once in the form of a market crash/bear market.

Conclusion

I am not a doomsayer. Rather, I have simply noticed through my studies of the market that the prices have become misaligned with the fundamentals. In addition, other factors, such as buybacks and junk bond yields, are pointing to a significant correction at the very least...

Disclosure: The original article was edited ([ ]) and abridged (...) by the editorial team at munKNEE.com to ensure a fast and easy read.