(Photo Credit: Don Shall)

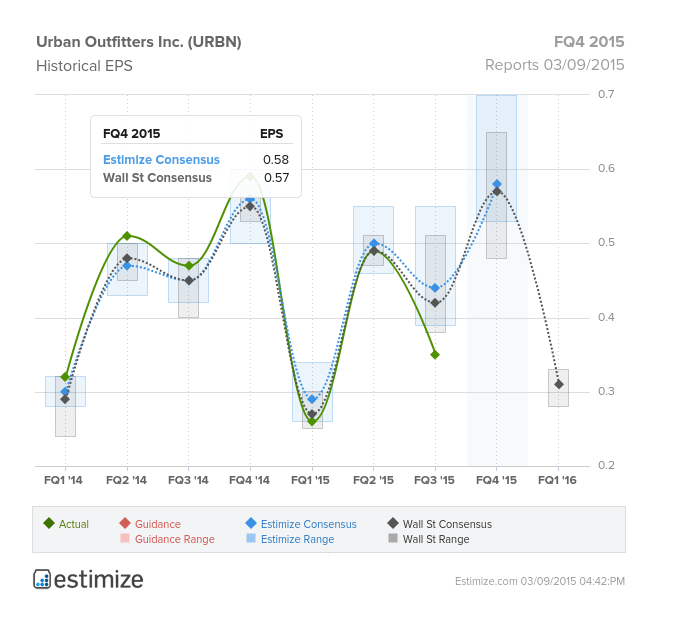

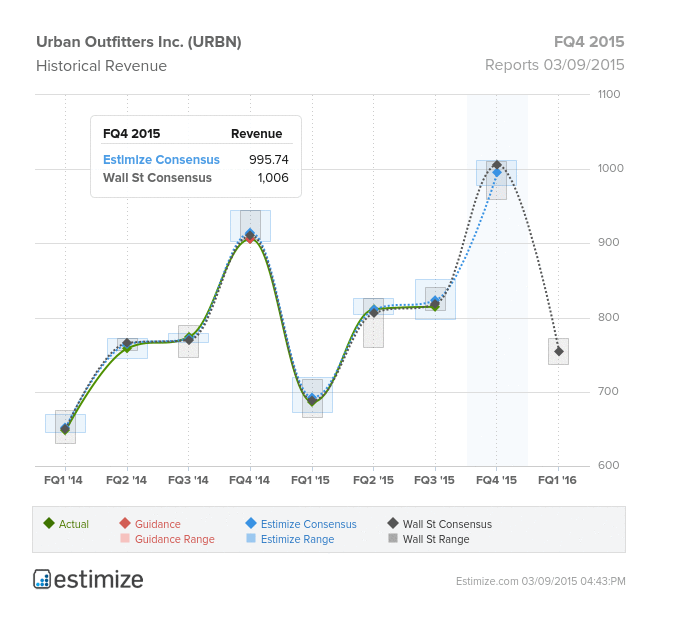

After today’s closing bell we get Q4 results from specialty retailer, Urban Outfitters. Currently the Estimize consensus is calling for earnings of $0.58, a penny higher than the Wall Street consensus of $0.57, indicating a 2% drop YoY. Revenues are anticipated to come in at $995M, also slightly lower than the Street’s estimate of $1.0B.

Urban Outfitters reported negative profit growth for the first three quarters of 2014, as their flagship brand continues to suffer, and robust sales from their Anthropologie and Free People brands aren’t quite enough to offset the losses. For most of the year, the company has made several missteps with their in-store product mix which can sometimes be disjointed, add to that poor decision making when it comes to incorporating sometimes offensive merchandise. The trend towards e-commerce also hasn’t helped. Foot traffic has consistently declined in the U.S., with buyers preferring the convenience and cost savings of online shopping. This hurts stores such as Urban Outfitters who depend on sales in their brick and mortar locations, and while they’ve ramped up their e-commerce efforts, online sales come with thinner profit margins.

Like many others in the apparel space, Urban Outfitters is also likely losing marketshare to fast-fashion retailers such as H&M and Zara which service the same customer demographic. In order to compete, they’ve had to offer deep discounts, the holiday season being no exception. We expect to see mention of heavy promotions in the latest quarter.

There are some signs that the retailer might be making a comeback, however. On February 9 the company reported Q4 comparable store sales of 6%, with an 18% increase from Free People, 6% at Anthropologie and 4% at Urban Outfitters which was previously down 7% in Q3. Several firms have also recently upgraded their price target for URBN, most notably Goldman Sachs on Feb 13.

Comments

Log in or sign up to join the conversation.