“In practice, tightening policy enough to slow growth meaningfully without tipping the economy into recession has been the exception rather than the norm. That said, the 1994-95 tightening cycle resulted in a significant slowdown, rather than a recession; the next recession after the 1994-95 tightening cycle did not start until 2001, following the 1999-2000 tightening cycle. (High-Frequency Economics, Web Page, Jan. 2019)

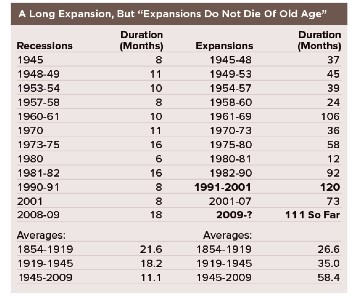

The economic growth expansion in the US, which is about 9 ½ years old, is approaching record book status. When the current expansion reaches June, it will become the longest in history.

Nonetheless, pessimists are right to worry about the viability of the US expansion and the outlook for the other advanced economies. Their concerns focus mainly on next year, rather than this year since the Federal Reserve Bank is attempting to engineer a soft economic landing at a time that fiscal policy will begin to tighten.

The Fed is in a quantitative tightening mode and has raised interest rates nine times since 2015. Up to the end of last year, US economic growth and employment has been unusually strong, even though the Fed had been raising interest rates and has been reducing its balance sheet by about $50 billion per month. Nonetheless, interest rates and inflation are still low, which provides some support for those, like this writer, who believe that a soft landing is possible.

Even though the Fed continues to monitor the economy for overheating, our experience has been that most American economic booms end when the central bank raised interest rates too far and tips the economy into a downturn.

While there is little risk of a recession this year, risks clearly escalate in 2020 when most of the advanced economies will be growing at a slower rate and their fiscal boosts will have faded away.

It should be noted that the last two American recessions were associated with excesses in real capital spending. The collapse of the dot-com and telecom spending boom led to the 2000-01 recession, while a housing bubble preceded the Great Recession. However, at present, it is hard to detect any significant excess capital spending in the US or the other industrial economies.

But as the Fed chairman Powell has observed, the last two downturns were also precipitated by financial excesses. The current concern on the financial side centers on corporate indebtedness. Because of a lengthy period of historically low-interest rates, American and European corporations borrowed massive amounts of money, possibly to excess. As interest rates increase and their economies slow down, the corporate debt burden will also increase.

Corporate financial risk has also increased since the US Fed embarked on its balance sheet reduction program, currently running at about $50 billion a month. The European Central Bank (the ECB) is also planning to engage in a milder form of quantitative tightening, which will involve winding down its bond purchases.

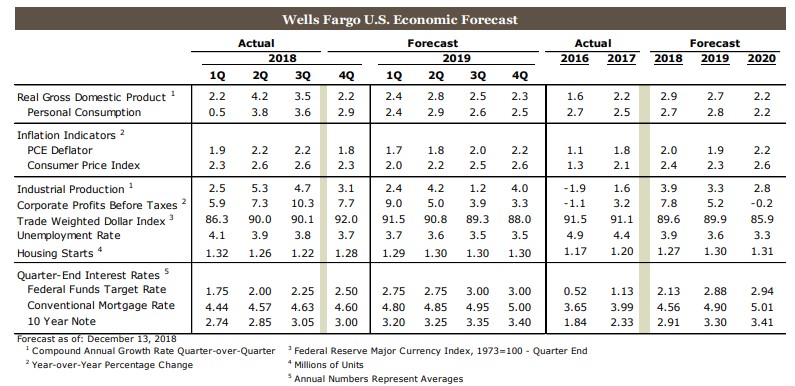

An example of a soft-landing US economic outlook is set out in the following projections prepared by Wells Fargo.

The tightening of financial conditions and the fading of the fiscal stimulus are the key drivers of the US and global growth deceleration expected in 2019 and 2020.

Is It Possible For The US Economy Too Have A Soft Landing?

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.