This is getting way too stupid. The Keynesian Chorus is going into a full blast trilling campaign, emitting a shrill cackle of warnings against a Fed rate hike. Yes, 80 months of pumping free money into the canyons of Wall Street is not enough.

Why?

Well, this is hard to type with a straight face, but according to the cackling gaggle of Keynesian Chicken Littles, the Fed has already tightened too much!

Paul Kasriel, the former chief economist at Northern Trust who now writes “The Econtrarian” blog, argues that “in recent months Fed monetary policy has become downright restrictive.”

Would that Kasriel could be dismissed as merely a Wall Street shill, but its seems that he’s taking his cues directly from John Maynard Keynes’ very vicar on earth. That would be Larry Summers, who yesterday blogged an identical bit of tommyrot:

I believe the case against a rate increase has become somewhat more compelling even than it looked two weeks ago…..First, markets have already done the work of tightening. The U.S. stock market is worth $700 billion less than it was 2 weeks ago and credit spreads have widened noticeably. Financial conditions as measured by Goldman Sachs or the Chicago Fed index have tightened in the last 2 weeks by the impact equivalent of more than a 25 BP tightening. So even if resisting inflation required a 25 BP tightening as of two weeks ago, this is no longer the case.

You can’t make this stuff up! And you don’t have to mince any words, either. This whole mantra that free money is actually tight money is the product of a tiny circle of academic scribblers and Wall Street hirelings who have invented what amounts to an alternate vocabulary of economic news peak.

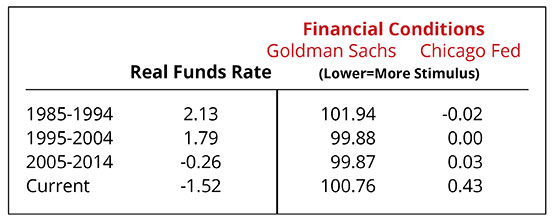

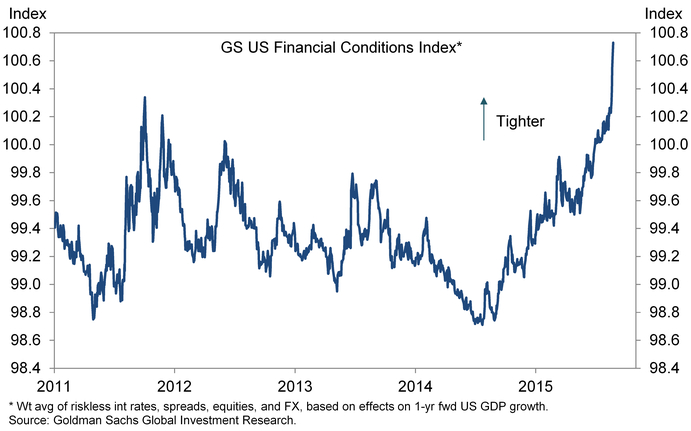

Exhibit number one is the Goldman Sachs Financial Conditions Index. As shown below it purportedly has surged sharply toward “tightening” during the last 15 months.

In fact, using this index Professor Summers twists economic logic into a corkscrew. By his lights, today’s deeply negative real interest rates at -1.52% are actually far tighter than 30 years ago when real interest rates were +2.13%!

I am not exaggerating. That’s exactly what the man said:

The figure below makes a crucial point. It shows that even though the federal funds rate is very low (negative one and a half percent after adjusting for inflation, financial conditions are helping the economy less than in previous years when interest rates were much higher.

Here’s the thing, however. Would you actually buy a used car from Goldman Sachs?

It turns out that this purportedly scientific measuring rod is just a goal-seeked data concoction put together by none other than the B-Dud. Back when Bill Dudley was Goldman’s chief economist, he needed a convenient metric to signal whether or not Greenspan was pleasuring the Wall Street gamblers with “moar” money at any given point in time.

So he came up with a four-factor indicator based on interest rates, credit spreads, equity market prices and the value of the US dollar.

That is to say, financial variables that are so powerfully influenced by Fed policy that they comprise the next closest thing to an auto loop. And a perverse one at that.

To wit, when the Fed is heavily pumping monetary juice into Wall Street and the gamblers are in a full throttle “risk on” stampede, what happens to the components of this miraculous index?

Why the dollar weakens, as it is sold short into the offshore and EM carry trades; credit spreads narrow since its risk-on time; equity prices rise because the casino is rocking; and interest rates are pegged at zero because the FOMC has essentially expropriated/nationalized the money market.

But when the resulting financial bubble finally reaches its apogee, as it did in the spring of 2000 and during the fall of 2008, the gamblers eventually succumb to a spat of “risk-off”, causing three of the four indicators to beat a panicked retreat.

Accordingly, credit spreads widen, as junk and other risky credits are dumped; the dollar soars as off-shore markets scramble to cover the immense dollar short; and equity markets fall as leveraged trading in the casino is unwound.

Yet, wouldn’t you know it. The inevitable collapse of the Fed’s bubble cycle causes the Goldman Sachs Financial Conditions Index to go vertical!

In a word, the Goldman gamblers have constructed a junk economics index that tells the Fed not to tighten because the arrival a modicum of sanity in the casino is evidence that it has already tightened.

Source: Goldman

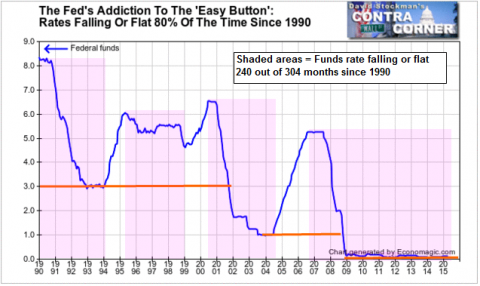

It is not surprising, therefore, that the Fed almost always has its hand on the Easy Button. Indeed, during the last 25 years, it has been cutting rates or holding them constant at (mostly) ultra low levels 80% of the time.

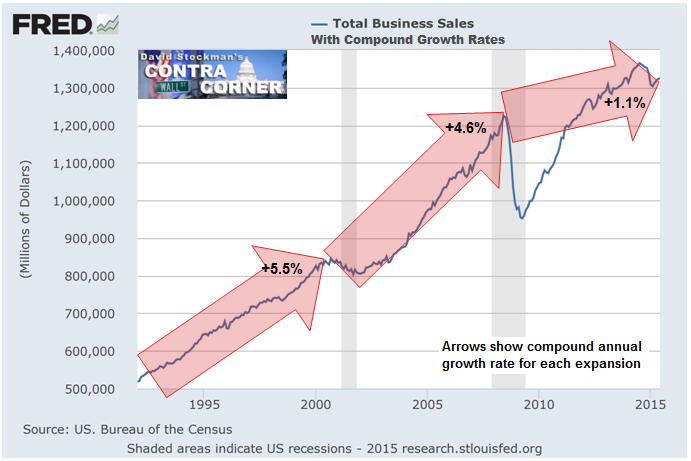

Yet the real economic facts do not lie. Even as the Fed has resorted to progressively more extreme money printing sprees with each bubble cycle, the actual growth of the business system has slowed. Since the mid-2008 peak, for example, business sales have expanded at only a 1.1% annualized rate—-a small fraction of what occurred during the two prior cycle.

Total Business Sales

Comments

Log in or sign up to join the conversation.